Tax increases are the best cure for inflation

It's pretty weird that we use interest rate hikes to reduce aggregate demand

The collapse of Silicon Valley Bank is in part a story of mismanagement and poor regulatory supervision, but it’s also in an important sense a consequence of the decision by the Federal Reserve and other major central banks to fight inflation by raising interest rates. Which in turn should put on the table the long-ignored question of why exactly interest rate hikes have become the world’s preferred anti-inflationary measure.

A big part of the answer is simply that raising interest rates is a thing that central banks have the legal authority to do, and there’s widespread belief that it makes sense to delegate macroeconomic stabilization to central bankers. But if you step back from that aspect of institutional design, there’s a strong argument that taxes are a superior inflation-fighting tool, one that would slow inflation in a more direct and more predictable manner. If the main problem with fiscal policy as an anti-inflationary measure is that the main inflation-fighting institution isn’t allowed to use it, then maybe optimal policy would involve adding a fiscal dimension to the Fed’s authorities.

After all there is something deeply perverse about raising interest rates to slow the economy only to flip around and do bailouts to prevent interest rates from slowing the economy too much.

The interest rate channel

Fundamentally, inflation is a question of too much money chasing too little goods and services, resulting in increases in prices. The ideal inflationary fix is to increase economic productivity (increasing the amount of “stuff” the economy produces per unit of input). Matt has written a lot on this website about ways to do that, whether through zoning changes that allow more housing to be built, permitting reform that increases energy supply, rescinding Trump’s tariffs, or other supply side reforms.

But these are really not the kind of changes that can realistically be delegated to a central bank. Permitting rules and zoning laws impact inflation, but they have many other kinds of impacts over which voters will rightly insist on maintaining more direct control. Legislators need to try to find politically viable strategies over the long-run for increasing the country’s economic capacity. But in the short run, it falls to central banks to manage inflation by regulating the amount of spending in the economy.

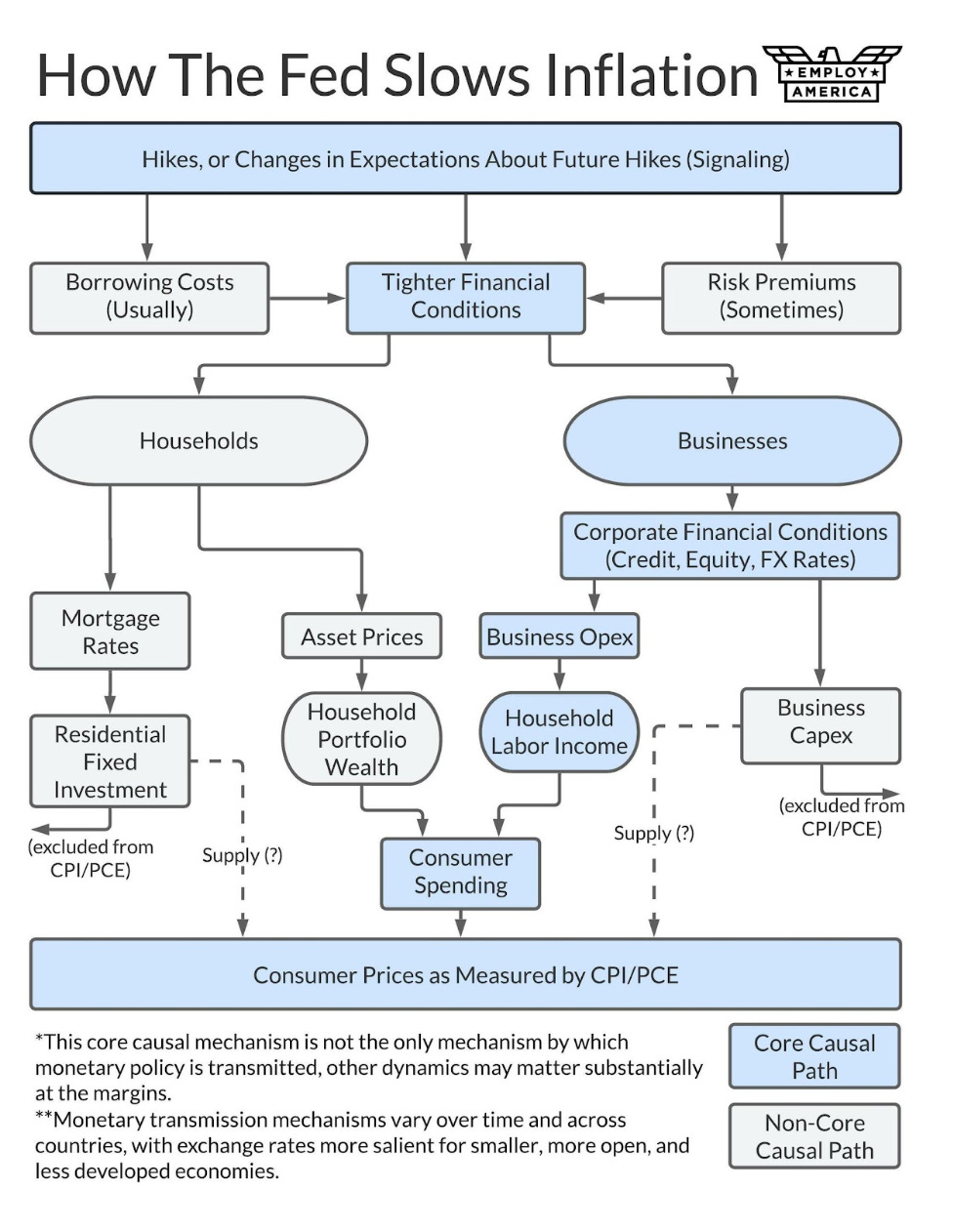

The primary way the Federal Reserve does this is raising or lowering the interest paid on banks' reserve balances at the Fed, which passes through to other interest rates in the financial system and the broader economy. The idea is that when the Federal Funds Rate changes, other interest rates throughout the economy change in the same direction.

Higher interest rates make it more expensive to borrow in order to invest in new equipment, in building a new home, or in plugging a gap caused by a temporary downturn in sales. The reduced borrowing that comes from higher interest rates directly reduces spending, but it also has indirect impacts. When some people get laid off or have their hours cut because of the drop in business investment, they cut back on their spending, which reduces aggregate demand.1

These cutbacks on spending are the primary ultimate mechanism that interest rate increases reduce inflation — this Employ America flow chart maps the various mechanisms.

A very imprecise mechanism

While raising interest rates can be effective in curbing inflation, it has some major drawbacks. The first is that it takes time for the effect of rate hikes to ripple out and affect aggregate demand — hence Milton Friedman’s quote that monetary policy operates with “long and variable” lags.

There’s some evidence that better communications technology has reduced the length of these lags in recent years (down to 6-9 months according to a recent meta-analysis) but it’s intrinsically hard to predict because of the cascade-like transmission mechanism. This time lag makes steering the economy challenging for the Fed. It’s not just that it takes time for the interest rates to have their full effect, but new things keep happening in the world — central bankers need to decide today what they think the economy will look like in a year.

Second, it’s odd to fight inflation with a tool that so directly hammers investment in businesses and housing. Investment is how economic productivity increases. It's what grows the supply side of the economy and ultimately allows for higher living standards.

Third, as we’ve all just seen, rapid changes in interest rates have side effects on the financial system. Banks borrow short and lend long: bank deposits are effectively short-term, low-interest loans to the bank. Banks then keep some of the money on hand and lend the rest out at a higher interest rate — usually with longer terms. The spread between the rate they pay their depositors and the rate they earn from those they've lent to is the profit. SVB took a bunch of money from tech firms and venture capitalists and lent it to the federal government by buying a bunch of Treasury bonds. This was essentially SVB making a big bet on interest rates remaining low.2 SVB was unusually exposed to hikes because, by having its depositors come primarily from the venture capital and tech industry, which are particularly sensitive to rate increases, its business model was essentially a double-down bet on rates staying low. But the fact that it collapsed has undermined confidence in banks like Signature Bank and First Republic (the technical term for this kind of thing is “contagion”).

The SVB situation had some unique aspects, but it illustrates the general phenomenon. Disinflation works in the short term through worsening financial conditions, and it’s hard to decouple financial conditions from financial stability risks. Higher interest rates are supposed to put some pressure on the banking system — but some particular bank is going to be much more exposed than average, and the failure of even one bank can create a big national problem.

Last but not least, interest rates have different impacts on different categories of workers. Rate-sensitive industries, like construction, bear the brunt of layoffs. This poses fairness problems. It’s also probably bad for the long-term efficiency of the economy — the construction sector tends to be structurally short of workers during booms because people are hesitant to take jobs in fields with a high level of instability.

The fiscal option

But raising interest rates isn’t the only way to take money out of the economy. We also have fiscal policy — the government can use tax increases to suck money out of the economy, reduce spending, and stabilize prices.

Of course, it seems unlikely that Congress could or would fine-tune tax policy several times a year in order to do macroeconomic management. But in principle, the Fed could be granted the power to raise and lower some taxes as an inflation-targeting measure.

The tax that would probably make the most sense would be a consumption tax — similar to the retail sales taxes charged at most stores in most states. European countries usually have a Value Added Tax (VAT) which is levied on the value added at each stage of production for goods and services. It’s similar in concept to a retail sales tax, but it’s administered differently and it’s designed to hit all consumption not just stuff you’d buy at stores. The more you consume, the more VAT you pay. So if the VAT goes up, households are directly incentivized to reduce their consumption, without any complicated bankshots.

You could imagine a set of institutional arrangements where the Fed (or any nation’s central bank) is authorized to raise or lower the VAT at its regular meetings to control aggregate demand.

Inflation is high? Raise the VAT to suck money out of the economy. Demand is too low? Cut the VAT so consumption increases and unemployed workers get hired. Instead of relying on a complex, ripple-out transmission mechanism such as interest rates, the Fed would be able to quickly and directly reduce aggregate demand, without the downside of reducing investment in expanding supply, and without concentrating the pain of fighting inflation on a few industries.

Meanwhile, back in reality

Sadly, not everyone reads economics blogs and in the real world, it might be difficult for the Fed to explain why it’s responding to the problem of high prices by raising the price of everything.

The opaque and indirect nature of the interest rate mechanism makes it a flawed tool, but it’s arguably integral to the Fed’s political sustainability. Monetary policy sounds (and is) complicated and technical in a way that raising taxes isn’t. This is part of what insulates the Fed from public backlash when it makes mistakes — such as cases where it raised rates unnecessarily before the economy had reached full employment.

It’s possible that people might anticipate a VAT hike and rush to buy things before it happens — the opposite of what the Fed would want (though of course, this anticipatory effect also applies to rate increases, though perhaps to a lesser extent due to their lower salience). Greater variability in tax revenue might also spook politicians, and have negative effects on the federal budgeting process.

In any case, delegating tax authority to the Fed would almost certainly be deemed unconstitutional as well. The constitution states, “Congress shall have Power To lay and collect Taxes, Duties, Imposts and Excises.” People disagree to an extent about the degree to which the constitution allows Congress to delegate the powers it’s been granted to executive agencies, but this would be a dramatic new form of delegation in the face of a conservative judicial majority that’s taken a very skeptical view of delegated powers.

So while some other countries with different constitutional laws might want to consider the idea of tax policy by central bank, for American purposes, it’s really just a thought experiment to demonstrate the value of fiscal policy as an inflation-fighting tool.

Here in America, Congress writes tax policy and the upshot is that congressional action on taxes matters a lot.

Biden kinda sorta did anti-inflationary taxation

The signature legislative achievement of the Biden administration thus far has been the Inflation Reduction Act (IRA). The premise behind the name of the bill was that it would reduce inflation, both by reducing aggregate demand, via higher taxes on the wealthy, and increasing aggregate supply through greater energy abundance. On both dimensions, this is exactly the right kind of inflation-fighting approach (and it’s part of why the IRA was an excellent piece of legislation).

But in practice, the taxes the Biden administration chose to raise weren’t particularly powerful levers to pull, purely from an inflation-fighting perspective.

Raising taxes on the wealthiest Americans pushes inflation in the right direction, but it has a relatively small effect. This is because the wealthiest Americans have a lower marginal propensity to consume their income: when taxes go up on billionaires, they reduce their consumption, but not by that much.

To really reduce inflation via tax policy requires either dramatically higher taxes on the rich, or broader-based tax increases, on the middle and upper middle class. The former is, unfortunately, not on the table, because the House of Representatives is controlled by the Republican party. The latter is almost certainly also not on the table due to bipartisan opposition — but as a matter of public policy, it would make a lot more sense as a way to fight inflation than raising interest rates.

Matt has written several times in the last few months on how a “grand bargain” in pursuit of deficit reduction, while a terrible idea in 2010, is now actually appropriate to our macroeconomic situation. This is what would be optimal right now: a compromise proposal, where Congress raises taxes on a broader swath of higher-income Americans than the IRA did, in order to reduce the deficit and control inflation. Ideally, this would involve raising taxes that have the fewest distortionary effects — taxes that cause the least deadweight loss, so to speak.

While a one time increase in taxes would be a good match for our present moment, it’s not a long term solution to macroeconomic management: what’s appropriate now might not be appropriate next year. And again, it’s obviously hard to imagine Congress voting to fine-tune fiscal policy every month, based on the latest inflation report.

But you could imagine a two-sided version of the “automatic stabilizers” proposals, which have been pushed by senators such as Michael Bennet as a way to respond to recessions. These proposals have primarily focused on automatically increasing spending on programs like SNAP, or unemployment insurance, when the unemployment rate rises. Economists like Claudia Sahm have also argued for direct payments to individuals (“helicopter money”) during recessions, in order to stimulate the economy.

But these automatic stabilizer proposals haven’t tended to address the flip side, when demand is too high. Congress could and should propose that tax rates, especially on consumption, automatically adjust, in whichever direction is needed, in response to economic conditions, as measured by the employment rate and the inflation rate. This would provide the anti-inflationary counterpart to Bennet and Sahm’s proposals.

Ideally, in order to address concerns about regressivity, these taxes would be targeted at the upper half of the income distribution — either via higher rates on luxury goods, or via an explicitly progressive consumption tax.

This all seems very unlikely to happen. But as a matter of good public policy, it should.

Higher interest rates also tend to depress the value of financial assets, making rich people less rich and therefore less inclined to buy stuff.

The reason this constituted a big bet by SVB on rates staying low is because, as Matt Levine has explained, what “rate hikes” means in practice is that the Treasury issues new bonds with higher yields. This mechanically depresses the price you’ll get for your older, lower-yield bonds if your depositors come calling and you have to sell them tomorrow — in short, rising rates lower the threshold for a bank run to actually occur.

| A guest post by

|

So then maybe DEFINITELY don't do "inflation relief payments" like some state governments did? Can we all agree those were one of the worst policy ideas ever?

This article misses an important point about why interest rates are used to control inflation rather than taxes. This point is the whole reason why interest rates are used to control inflation in the first place, and the author seems to be unaware of it.

When inflation is expected to be high, *real interest rates are too low*. The real interest rate is equal to the nominal rate minus expected inflation. The reason to raise *nominal* rates is in order to bring real rates back to the correct level. Put differently, inflation results in distorted incentives to consume and invest today relative to tomorrow. That's why intertemporal prices (i.e., interest rates) are used to control inflation.

By contrast, the VAT proposal doesn't directly address intertemporal prices, and it could even have perverse effects. Suppose that people expect inflation this year to be high. Then people anticipate that *next year*, the central bank will raise the VAT. This makes consumption next year more expensive relative to consumption this year, which effectively lowers the real interest rate and boosts demand now.