How Jay Powell is bending time and upending the business world

Higher interest rates drive the Bitcoin crash, tech layoffs, and everything else

Want to hear me talk more about SBF, FTX, and EA? Check out the latest episode of Bad Takes in which Laura says my takes on this are bad.

Layoffs at Meta and Amazon, the ouster of Disney’s CEO, and the collapse of the crypto market are all stories with their own nuances and plot twists.

But there is a genuine and profound respect in which they are all manifestations of a single phenomenon.

Inflation was higher in 2021 and stayed high longer in 2022 than most forecasters predicted. And it’s important to remember that these were general errors. Joe Biden and his administration and their supporters made those mistakes. I made those mistakes. But so did Jerome Powell (a Republican), the Fed staff (a very nonpartisan group of professionals), and most private sector forecasters at the big investment banks. And crucially, the collective forecast of bond investors got it wrong. I like to think the reason that I, personally, erred in my forecast isn’t partisanship but that I doubted my ability to outguess the financial markets. I mention this not to make excuses but to remind everyone that we shouldn’t retrocast what we know today — professionals with real money at stake were making decisions based on the idea that inflation would be much milder than it turned out to be.

That means this year’s rapid increases in the Federal Funds rate aren’t what people were expecting. And even though the rate still isn’t especially high, the speed of increase is unprecedented, and even if they step the pace down, it’ll still be a steep trajectory.

And this matters to the technology industry in particular because the rapid and not-properly-anticipated rise in interest rates has the curious property of bending time itself in a way that impacts different industries differently.

Time preference matters

Most of us suffer in some way from short-sightedness in our decision-making. It would make us happier in the long run to lose weight, but right now we want to eat a cookie. Or it would make us happier in the long run to go on a four-month personal austerity budget and pay down credit card debt, but right now we want to go buy Taylor Swift tickets. The conflict between now and later is part of life.

And as a parent, a big part of taking care of kids is dealing with the fact that they have extremely short time horizons.

Even smart kids are just terrible planners and have no idea how to manage inter-temporal tradeoffs. The whole community of people involved in children’s lives is basically just trying to get them to do things that will pay off down the road (learn to read, eat some vegetables) and avoid doing things that seem fun but might be regretted later. As people age and mature, they generally get better at this. But not everyone gets as much help from parents and community members early in life, not everyone matures into equal levels of wisdom about intertemporal tradeoffs, and a lot of the difference in people’s life outcomes is influenced by that kind of thing.

But over and above questions of rational decision-making, it oftentimes makes sense to discount future gains.

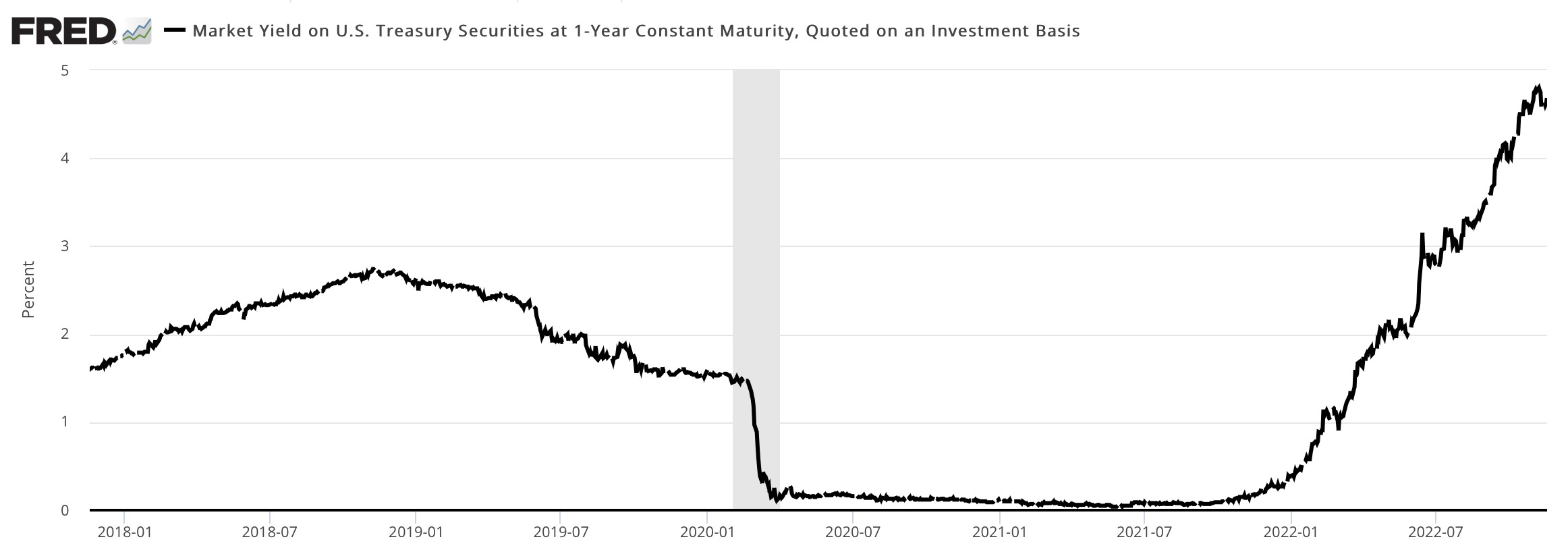

If I offered you a choice between $100 today and $100 a year from now, you’d take $100 today. What’s more, even if I sweetened the offer to $100 today versus $101 in a year, it would make sense to take the $100. Why? Well in part because you could earn more than that with zero risk by buying a Treasury bond. But if you had the chance to get $120 in a year versus $100 today, then you should take the $120. Note, though, that where you draw the line between “irrational short-sightedness” and “correct assessment of opportunity cost” is not a fixed thing handed down by God. It’s a variable handed down by a mix of market conditions and Jerome Powell.

As you can see here, the amount of risk-free interest you can earn on a one-year time horizon has been soaring this year. So it’s entirely rational for people to become more short-termist with their financial decisions.

Derek Thompson did a piece recently on “why everything in tech seems to be collapsing all at once” that flags the macroeconomic explanation before dismissing it as “fairly technical,” and launching into “another story that’s a little bit harder to prove. It goes something like this: The tech industry is experiencing a midlife crisis.”

Thompson’s explanation absolutely makes for a better story than the fairly technical one about interest rates and time preference. And I suspect he’s onto something with his midlife theory. But even though it’s not as viral, I really do want to insist that the technical explanation here is important to understanding why so much seems to be collapsing.

Jay Powell is making everyone more conservative

The one-year risk-free rate is fun to think about but doesn’t necessarily have huge implications for business.

But the 10-year rate is also rising, after having been in a period of structural decline for literally 40 years.

The story behind that long-term decline is itself interesting, but the point is that all of today’s middle-aged and young people are used to a world of falling interest rates.

With kids, developing a more long-term orientation normally means tamping down risk levels. But in investing, it’s actually the opposite. Because while you only have one life to live and it’s generally prudent to avoid wrecking it, in investing you can diversify in pursuit of big payoffs. So if when Google IPOed in 2004 and you thought to yourself “I don’t really understand how this company is going to make money, but the product is really good and I think more and more people will use it in the future,” you’d be in really good shape today. And by the same token, if you invested in an undisciplined way in Friendster and MySpace and Orkut and Facebook, you’d be in good shape today, even though three out of the four products failed.

When interest rates are low and “money now” has very little value compared to “money in the future,” it makes sense to take a lot of speculative long shots in hopes of getting a big score.

There’s a perpetual dynamic on Twitter where VCs — who are enthusiasts by nature — get enthusiastic about stuff, and then journalists — who are haters by nature — point out that the stuff sounds dumb. Looking back on the past 15 years, the journalists feel vindicated because a huge share of the stuff VCs get excited about turns out to be dumb. But the VCs also feel vindicated because they’re really rich, and skeptical journalists conveniently forget that they called seven out of the past two stock market crashes and said Facebook could never make money. At the end of the day, venture capital is just a slightly odd line of endeavor where flopping a lot is fine as long as you score some hits. I think most of us find this to be an unnatural way of thinking because, when you’re out there hunting and gathering, it’s very important to not be impaled by a bear or to accidentally feed your kid a poison berry. Good investors are able to internalize the much more abstract nature of finance and embrace prudent levels of embarrassing failure.

But what I think the VC mindset tended to miss was the extent to which the entire “take big swings and hope for the best” mindset was itself significantly downstream of macroeconomic conditions rather than being some kind of objectively correct life philosophy.

Big tech companies have been taking big swings

The application of this Fed-induced vibe shift to crypto is, I think, pretty clear.

Let’s say you think crypto is pointless for anything other than Ponzi schemes, scams, and maybe some money laundering. How sure are you about that? Sixty percent? Sure. Eighty percent? Sure. Ninety percent? Now I’m hesitating a little. Ninety-five percent? Ninety-nine percent? Yikes. I mean, a lot of very smart, very technically adept people swear that this is useful. What I think is probably happening is that even though these people are smart and technically adept, they don’t understand economics. But 99 percent is a really high level of confidence. I’m just a normal person who has money in a low-fee index fund. But if you’re thinking about investment allocation across the whole breadth of possible vehicles — stocks, bonds, real estate, timber, iron ore, whatever — then it seems like “0 percent” is maybe the wrong amount of your portfolio to be in crypto. But then interest rates go up, time-preference shifts, and suddenly the right amount of money to have in a totally speculative long-term gamble goes way down.1

But it also influences how companies handle their internal investment portfolios.

Part of the problem at Disney is that Disney+ loses a ton of money, even though it is, on its face, a good product. But part of the problem Disney is having in streaming is that they are competing not only against their traditional media rivals (HBO Max and Paramount Plus), but also the streaming startup Netflix, and then Apple and Amazon are also pouring all this money into streaming video. But why did Apple and Amazon decide they should be movie studios? You can reconstruct their specific thinking, but on some level it comes down to “well this seems like something we could do and it might pay off.”

And indeed both Amazon Prime Video and Apple TV+ are services that exist and have customers and win some awards and put on some good shows.

It’s possible that someday they’ll be enormously successful businesses, too. After all, it certainly wasn’t obvious when Amazon Web Services launched that it would become more financially successful than Amazon’s main (and more famous) retail business, and even though there was a lot of excitement around the original iPhone, I don’t think everyone looked at that and said, “well this is obviously going to be the most successful consumer product of all time.”

You get big successes by trying stuff. At the time, lots of people thought it was crazy of Google and Facebook to pay as much as they did for YouTube and Instagram, even though in retrospect they not only got great prices but we also maybe wish the Justice Department hadn’t allowed those mergers. But it’s not like every acquisition or new product was a huge hit. Google is infamous for launching and then killing products. Facebook tried to make a phone, Apple keeps trying and failing to make social networks — it’s just necessarily a graveyard full of failures alongside the successes.

And as long as you’re constantly trying out new things, layoffs are unattractive, even if you think some of the specific things some of your people are doing seem superfluous — there’s always something new on the horizon that’s going to need new people. But then the worm turns.

Now people want money

With interest rates higher, you have a structural shift in business thinking toward “I’d like some money now.” Something really boring like mortgage lending now has a decent return, so you don’t need Bitcoin. And if your company is profitable, shareholders would like to see some dividends. If it’s not profitable, they would like to see some profits.

The specific way this process of “lay a bunch of people off and hope that makes the company profitable” is playing out at Twitter is dramatic and weird and being handled in a bizarre way by Elon Musk since he decided to become the main character of the news cycle. But the exact same thing is playing out at a bunch of other mid-tier tech companies because the fundamental dynamics don’t have anything to do with Musk or his politics; they’re about Powell bending time to make present money more valuable relative to future money than it used to be.

Higher interest rates mean rational actors’ discount rates are rising, so everyone is acting more impatiently.

An interesting question is what we should make of that change. It’s easy to pick specific cases and decide that as a rightist, you’re glad to see layoffs at Twitter, or as a progressive, you’re glad to see crypto crashing. But in a conventional sense, it’s bad to have a vibe shift across the business community that makes everyone more impatient and more oriented toward the short term. We’d be better off fighting inflation in ways that are consistent with a more measured approach from the Fed because that helps maintain an investment-friendly economic climate.

At the same time, I do think a lot of us have the sense that the past 15 years have featured too much emphasis on throwing technical talent into super-duper-speculative ventures rather than something boring like “let’s make the self-checkout machines better” or “let’s earn modest sums of money by making it easier to schedule a plumber on the internet.” There are lots of places where more application of software and hardware engineering could do good, but where you’d be trying to hit singles rather than swinging for the fences. Big swings can be great, but I do think there’s something to the idea that such low rates for so long encourage so many big swings that you’re left essentially ignoring big swathes of the economy just because there isn’t a plausible story about creating a winner-take-all market with a strong moat. Lots of the stuff people buy and rely on doesn’t have those characteristics but would still benefit from attention and investment — attention that will hopefully be coming in the new paradigm.

This, to be clear, is not to defend anything that happened at FTX, which seems to have been a simpler fraud just moving along in the slipstream of rising crypto prices.

I think the observation that 'time preference is very important' is correct. A low interest rate environment allowed all kinds of speculative ventures to take off, knowing they had years to borrow money cheaply and make money in the long term. That's changing now, and consequently any business that was doing that is suffering. The Metaverse thing Facebook has was a dubious proposition in a low rate environment and looks downright kamikaze now.

And it's great to see crypto suffer. Nobody has identified a use case for it except crooks. The only reason people bought it was to gamble that someone would buy it off you in the hope they could sell it to someone else for a higher price. That's a bad bet at anytime, but looks ridiculous at a time when you can get decent yield at low risk. Bitcoin mining is an environmental disaster.

It seems weird to have an entire article about tech woes and not mention at all the straightforward business decline being suffered by the big players in tech.

Part of the story here is that during the pandemic, ecommerce was up, online advertising was up, streaming services were up, and so forth. The companies bet that they could hang onto most of those gains in a post-pandemic world, and they were wrong. Now they have revenue problems.

That's not to say that time preference isn't also part of the story -- it's certainly part of the story that tech is telling itself -- but there's some pretty straightforward business decline too.