What's going on with inflation?

A soft landing, if you can keep it

Inflation! It’s been the dominant economic story of the last two years, and there have been some mixed signals in recent months about where things will go from here and what the appropriate course of action for policymakers is. So today I’d like to break down where things stand now, the arguments for both dovish and hawkish policy, and where things might go from here.

To (very) briefly summarize the last two years of economic news, Congress passed several major stimulus bills in 2020 and 2021 due to fears of a pandemic-induced depression and of repeating the mistakes made after the 2009 financial crisis. Separately, the Federal Reserve decided that they had been underrating the full employment part of the dual mandate while overreacting to the risk of inflation and decided to adopt the “flexible average inflation targeting” (or FAIT) framework in their 2020 review.

Prices began rising in early 2021 and have continued to do so since. Dovish observers argued that this inflation was transitory, caused by supply chain disruptions created by Covid-19 and later Russia’s invasion of Ukraine, and not solvable with tighter monetary policy. Hawks countered that inflation was caused by excessive fiscal stimulus and must be curtailed by quickly tightening monetary policy, even at the risk of a recession, in order to avoid inflation expectations from becoming unanchored and spiraling out of control.

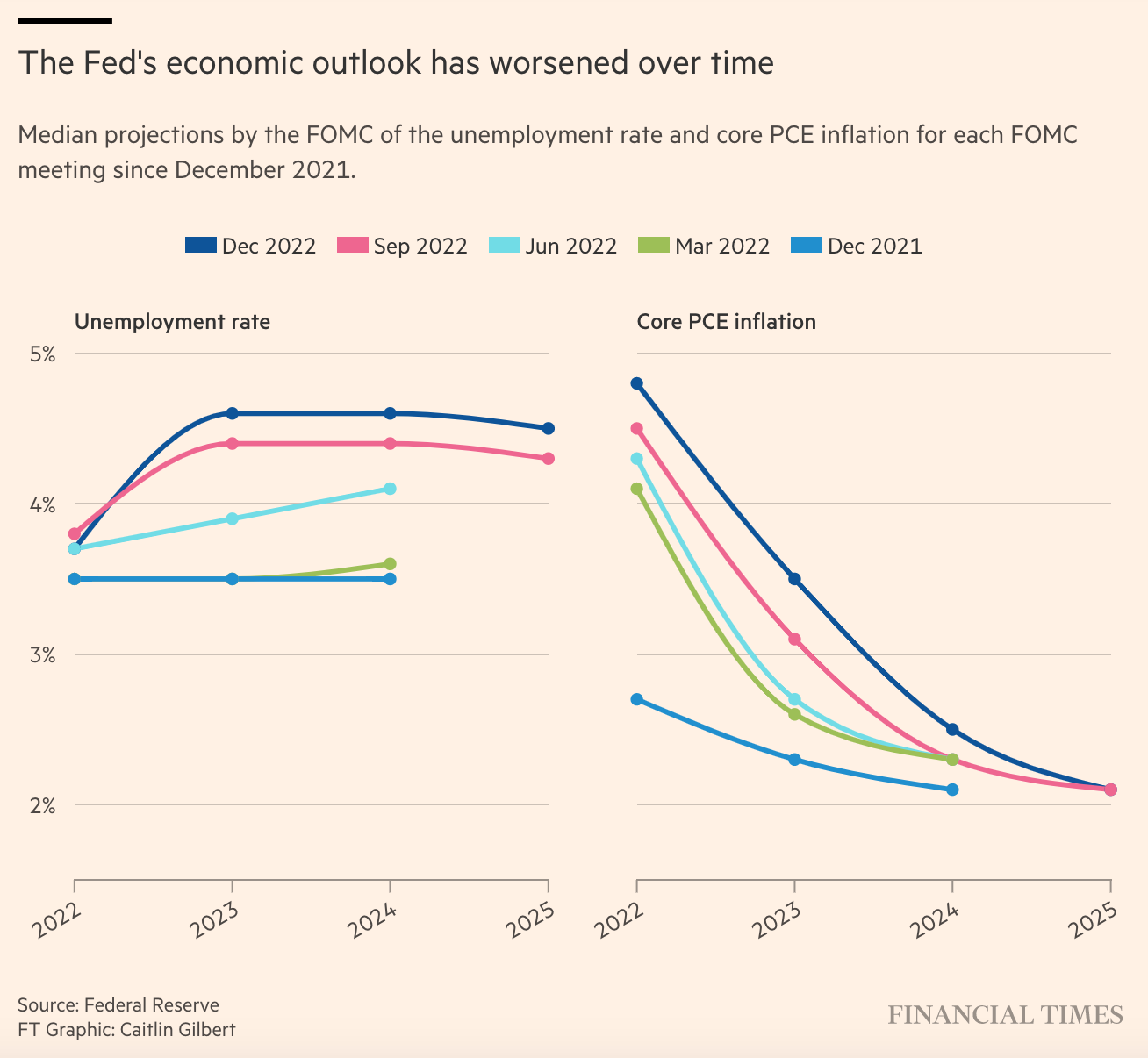

Despite the Fed’s incredibly rapid series of rate hikes in 2022, the labor market remains white-hot. The unemployment rate in December was a historically low 3.5%, the prime-age employment-population ratio sat at 79.7%, and the ratio of unemployed people to job openings was 0.57 in November, the most recent month for which data is available.

Following several cool inflation reports, the December print came in with headline CPI dropping from 7.1% to 6.5% in year-on-year terms and core inflation (which is what the Fed primarily focuses on) falling from 6% to 5.7%.

So what comes next?

The case for dovishness

There are two basic arguments for dovishness: (1) inflation itself is cooling and (2) supply problems are beginning to work themselves out.

The last three CPI prints have come in cooler than expected, but there’s reason to believe that official inflation measures are actually overestimating the speed of price increases.

Housing is the largest single line item in most households’ budgets and it carries the most weight in official inflation indexes, with the “shelter” category making up 32.8% of the Consumer Price Index. Housing costs for homeowners make up the majority of the “shelter” category and are calculated using something called “owners’ equivalent rent.” Tim Lee and Aden Barton have a great explainer on the nuts and bolts of OER, but for our purposes what matters is that OER and CPI: Rent of Primary Residence move in the same direction.

But the rent of primary residence is a measure of average rents — the Bureau of Labor Statistics asks a bunch of people how much they pay in rent and then averages the results with some adjustments to ensure a nationally representative sample. A more accurate measure of current housing prices is spot rents,1 or how much it would cost to sign a new lease on an apartment today. As old leases expire, average rents will move around, but mechanically they always lag behind spot rents because they include a bunch of old leases with terms that may not be in sync with the current market.

As covered in Slow Boring, spot rents were higher than average rents earlier in the year, which meant that official measures were likely underestimating “real” inflation. But that’s now reversed, and the sheer weight housing carries in the indexes means that the overall inflation is likely to cool as average rents catch up to spot rents.

There are positive signs elsewhere on the supply side. The prices of gas and used cars — flagged as key contributors to inflation earlier in the year — are down 35% and 15.6% respectively from their peaks earlier this year.

The Inflation Reduction Act and bipartisan infrastructure bill provide funding to reshore supply chains, with semiconductor plants already being planned or built in Columbus, Ohio and Phoenix, Arizona. The full impact of these bills will only materialize over the long run, but they’re moves in the right direction. In the short term, the end of China’s Zero-Covid policy will remove a major bottleneck on global supply chains, and there are promising signs that European manufacturing is adapting to doing more with less in the face of Putin’s de facto natural gas embargo.

Because rate hikes make loans more expensive, they reduce business investment, including investments in expanding supply. Since doves believe that various supply shortages are causing a large chunk of inflation, further rate hikes might actually be counterproductive and crimp supply when we need it to expand (this is why the Fed doesn’t raise rates when a boat gets stuck in the Suez). And there are some signs in the housing market that this is happening — starts have fallen in 2022 but completions remain on trend.

That’s part of why doves are arguing that the Fed should ease off on the brakes; the other reason is that they believe the benefits of maintaining full employment are worth slowing the pace of tightening. Here’s Elizabeth Warren arguing that further rate hikes will damage the labor market and risk a recession.

Economist Claudia Sahm says that while the American Rescue Plan did create some inflation, that was a price worth paying for full employment. “I’m not doing a victory dance, but I’m over the moon about the labor market — I would pick 3.5% unemployment and 10% inflation over a worse labor market,” she told me over the phone. “Inflation is coming down, the labor market is still kick-ass, and the only way for the Fed to get demand down is to weaken the labor market and the labor market ain't coming down.”

The Fed is projecting that unemployment will rise almost one percentage point over 2023, which Alex Williams of Employ America says constitutes the Fed “trying to engineer a recession,” pointing out that “the unemployment rate has only increased by 1% within a year twelve times since World War II. Every time, (1) we saw a recession, (2) the unemployment rate continued to increase far beyond the initial 1%.”

Aggregate demand is still above-trend

The argument for continued hawkishness is that aggregate demand is still really high.

One way to look at this is to consider the NGDP gap: the difference between actual nominal GDP and the forecasted level of nominal GDP for a given quarter. It’s essentially a measure of how hot the economy is running — and right now, it’s pretty hot.

Another way of looking at it is personal savings or aggregate labor income, and both are well above the pre-pandemic trend.

The point here is that stimulus bills, specifically the American Rescue Plan, overshot the demand shortfall caused by Covid-19.

“Prices are going up and yet people continue to consume because they have more money to spend,” David Beckworth of the Mercatus Center told me, “but the fact that they could find more money to spend means that policy was too loose.”

Here’s what Larry Summers, one of the leading hawkish voices in the inflation debate, said in February 2021, before ARP passed Congress:

In contrast, recent Congressional Budget Office estimates suggest that with the already enacted $900 billion package — but without any new stimulus — the gap between actual and potential output will decline from about $50 billion a month at the beginning of the year to $20 billion a month at its end. The proposed stimulus will total in the neighborhood of $150 billion a month, even before consideration of any follow-on measures. That is at least three times the size of the output shortfall.

In other words, whereas the Obama stimulus was about half as large as the output shortfall, the proposed Biden stimulus is three times as large as the projected shortfall. Relative to the size of the gap being addressed, it is six times as large.

That’s the core case for remaining hawkish: inflation is fundamentally a macroeconomic phenomenon, and so as long as aggregate demand remains high, prices will keep rising. If the price of used cars drops and people still have an extra pile of savings, they’ll spend that money on air fryers instead until that pile gets spent down.

It’s also worth noting that the Fed and the financial markets have consistently underestimated the sticking power of inflation over the last two years. Three cooler prints are welcome news, but the job’s by no means finished. Inflation is still well above the Fed’s 2% target, and easing up now could undo the progress made so far — and in the worst case, lead to inflation expectations becoming unanchored.

Predicting the future is hard

Unfortunately, I don’t know exactly what’s going to happen, and if I did know with certainty how the inflation situation would play out, I’d use that information to make some lucrative trades instead of emailing it to you.

But the Fed has gotten much more pessimistic over the past year. They now believe it will take longer to get back to 2% inflation with a greater cost to employment, returning to rate cuts only by 2024. In their December forward guidance, they said they did not expect to cut rates at all in 2023. Some of this tough talk is probably about expectation setting. If markets react to slowing rate hikes by acting as if the Fed is done tightening, it undoes the effect of the previous, larger hikes. But some of these more bearish projections no doubt reflect members of the FOMC updating their views to match new data.

The pessimistic take is that hot demand will continue to outstrip supply and keep inflation high until demand is brought back down to earth. Larry Summers thinks that getting inflation under control will require a recession in 2023, with unemployment rising to around 6% and the federal funds rate peaking at over 5% (it’s currently sitting in the 4.25 to 4.5% range). That’s the hard landing scenario.

But there’s a case for a soft landing.

As I am reminded when I log into my Fidelity account, the past year of rate hikes has not been kind to the stock market. This drop in asset values is likely to reduce consumers’ propensity to spend down their excess savings (research has found that consumer spending rises by 2.8 cents for every $1 increase in stock wealth). Meanwhile, home prices have gone down while mortgage costs have gone up as a mechanical effect of rate hikes. The upshot is that it’s now much more attractive to spend extra savings on a down payment for a house, which drains checking accounts by creating a lower-leverage economy (i.e., less mortgage debt) rather than a binge on consumer goods.

And there is some empirical evidence that monetary policy operates with lags, though the size of the lags depends on whether policy works primarily through expectations or hydraulic channels and may change over time. So the past year of hikes may only now be kicking in.

Beckworth said he would be “surprised if they continue to raise rates past spring; they may have to start cutting rates by summertime.” He warned that the Fed might end up making the same mistake it made in 2021 in the opposite direction, overcorrecting and providing forward guidance that locks policy into a potentially non-optimal path.

“A soft landing is possible if we ease off on the brake a little bit. Inflation can still come down if the Fed is more gradual, not so hawkish,” he told me, noting that “bond markets think this is going to happen already.”

Changing the target

I highly doubt that a college freshman (even one as intelligent, charming, and humble as myself) has a better sense of what’s going on in the macroeconomy than the experts at the Fed or professional bond traders. I’m inclined to trust their judgment on the 50-point hike after November’s inflation numbers, and given the December figures, I think 25 basis points seems about right for the next meeting.

But let’s say it’s the middle of 2023, inflation is sitting at 3% and unemployment is at 4 or 4.5%. Is it worth raising unemployment by another point to get inflation down to 2%? Larry Summers says yes, writing that “a shift now even to a 3 percent target, let alone a higher one, would set the stage for a stagflationary decade.” Olivier Blanchard seems more favorably inclined towards raising the target, but notes that doing so now might have risky impacts on expectations. Beckworth told me that there was a good case for a 3% target, but failing to get back down to 2% might look like the Fed folding to political pressure, setting a bad precedent and undermining long-term expectations of inflation stability.

That all makes sense to me. I think that raising the inflation target to 3% might be a good idea2 because it provides more room for monetary stimulus by getting us further from the zero lower bound (you can't cut interest rates below zero)3. Long-term factors such as population aging haven’t gone away, and that’s going to push interest rates and aggregate demand down in rich-world economies — which in turn merits dovish monetary policy such as raising the inflation target. But in order to pull off a major shift like that, central banks need to maintain their credibility, making it all the more important to finish the inflation-taming job this time around.

But in the long run, we’re all dead. For now, it seems like a soft landing is within reach. Things might change in the next few months, but right now inflation is falling and unemployment is low. Let’s hope those trends continue (RIP Phillips Curve).

If you’re interested in the details of different spot rent indexes, Joey Politano has a great post explaining a new one — NTRR — from researchers at the BLS and Cleveland Fed.

Fun fact, all the central banks use the 2% target because New Zealand happened to have picked it first in a somewhat arbitrary manner.

Yes, technically you can use tools such as negative rates or quantitive easing, but these aren’t as effective as rate cuts and ceteris paribus central bankers would prefer not to have to resort to them.

Milan - you write a real good take. This is as good as anything I've read on the current state of inflation. And I've read a fair amount. Congratulations and keep up the great work. For what it's worth my take is that there should be a soft landing, unless the Fed becomes needlessly sadistic. Among other things, there's this piece by Connor Sen in Bloomberg from 10 days ago:

https://www.bloomberg.com/opinion/articles/2023-01-09/rental-housing-is-suddenly-headed-toward-a-hard-landing

Anecdotally, the apartment building where my wife and I live while we're looking for a new house is now offering $1,000 bonuses for new renters. When we rented in July, there were only 4 vacancies out of 340 units. Quite the reversal. No one asked but I think by July-Sept core PCE will be in the threes YOY and the fed will be looking at rate decreases by year end. Anyway, your piece was a real pleasure to read. Best regards.

I’m more a dove than a hawk, but Claudia Sahm’s complete apathy toward the inflation rate shows the type of contempt for voters that leads to bad things down the line. We can try to convince people they should care about different things, but we can’t really choose what voters care about, and inflation is very unpopular (I’d argue the same point on entitlements to conservatives who have issues with them - it’s a democracy and voters like social security, deal with it).