The vanishing case for student loan forgiveness

With no more need for stimulus, this doesn't make sense anymore

Student loan forgiveness is back in the news since the Biden administration decided to again extend the repayment holiday.

This is a topic where I think the facts have changed considerably since Slow Boring’s debut in mid-November of 2020, and as a result I have changed my mind. Back then, I thought loan forgiveness would be a good way to assist a depressed economy and that objections were being made on nonsensical grounds by fussy technocrats who weren’t paying attention to the actual situation. But today the situation is different. The economy is not depressed, and instead the Federal Reserve is pivoting to fight inflation. That means student loan forgiveness in 2022 is a purely distributive issue — one that will shift resources from the majority of Americans with no student loan debt to the minority of Americans who have it.

Both the debtors and the non-debtors are highly heterogeneous groups, but it’s pretty clear that the non-debtors are both more numerous and poorer on average.

So while there are certainly lots of individual cases where debt relief sounds like an appealing idea, under the current circumstances the case for broad debt relief has become extremely weak. There’s basically no other situation in which progressives would talk themselves into this kind of idea, which is currently being propped up with some very odd math about the racial wealth gap.

But I’d also say that the discourse around this seems to me to be largely driven by a correct sense that the higher education finance system in the United States is messed up and bad. The problem is that the form of debt relief that is being contemplated — one with no forward-looking reforms and in which even the most dysfunctional or abusive institutions still get paid in full — won’t fix anything about the system and could make it worse. Last but not least, I think the fascination with this idea represents a kind of unhealthy obsession with executive branch unilateralism. It’s important to understand and exploit the powers of the presidency, but the thing that sane people want here is not achievable through those means. What you need is a legislative coalition for reform, and probably a bipartisan one at that.

An idea whose time has passed

Once upon a time, I thought Joe Biden was likely to take office facing high unemployment, low inflation, and a GOP-controlled senate.

In other words, it would be an economy that badly needed fiscal stimulus but where fiscal stimulus would be hard to achieve. Under the circumstances, student loan forgiveness had a very attractive property — Biden could do it.

The reason is that back in the Obama administration, congress changed the student loan program from one where the federal government mainly guaranteed loans made by private banks to one where the federal government makes the loans itself. Since Treasury is the bank, the president can choose to simply not collect the loans. This theory has never really been litigated and it’s possible it could totally flop in court. But based on what people with actual law degrees have told me, it seems likely to prevail in part because it’s not clear who could sue to stop it or on what grounds or how a court victory for opponents would even work.

Skeptics raised two important objections to this plan:

It’s not a very effective stimulus, since the short-term spending impact of forgiving $1 of student debt is pretty low.

It’s a fairly regressive form of stimulus since student loan debtors are, on average, higher income than non-debtors.

Still, my view is that under the previous circumstances, these were not persuasive considerations. The key to me was that in the real world there wasn’t some other, better stimulus that Biden could do by not forgiving student debt. It’s not as if Biden had some big stack of money and was being asked to choose to use the stack on student loan forgiveness rather than some other thing. Instead, he had some specific statutory authority and the ask was that he use it rather than not use it. I was broadly in favor, though even at the time I didn’t think universal forgiveness (why did recent dental school graduates need debt relief?) made sense.

Then things changed. In December, Mitch McConnell brokered a deal to do roughly $900 billion in Covid relief that he hoped would help his candidates in the concurrent senate elections happening in Georgia. The plan didn’t work and those candidates lost anyway. Then Joe Biden surprised me by proposing a very large $1.8 trillion American Rescue Plan. Then moderate Democratic Party senators surprised me even more by saying yes to the proposal. By February, I said the case for debt relief was getting weaker. Then after that, moderate Republican senators surprised me a bit by saying yes to a bipartisan infrastructure bill that, like the Covid relief bills, is mostly financed with debt. And in the months since February, inflation has emerged as a big topic of discussion, with the Fed accelerating the end of Quantitative Easing and everyone wondering how many interest rate increases will happen in 2022 and 2023.

Debt relief in a world of tradeoffs

This new situation completely transforms the impact of student loan relief.

In a depressed economy, loan relief is a windfall for student debtors. But to the extent that they spend that windfall, it “crowds-in” investment, employment, and economic opportunity on the part of others. Your spending is someone else’s income, so while it’s a bit arbitrary and unfair to specifically shower the cash on student debtors, it does in the end benefit most people — including the people who most need help, the unemployed.

But then instead of doling out $1 trillion in student loan relief (roughly the cost of the Schumer/Warren plan to forgive up to $50,000 per debtor) congress handed out $2.7 trillion in direct checks to the non-rich, in supplemental UI payments to the jobless, and in aid to small businesses, state and local governments, and school systems.

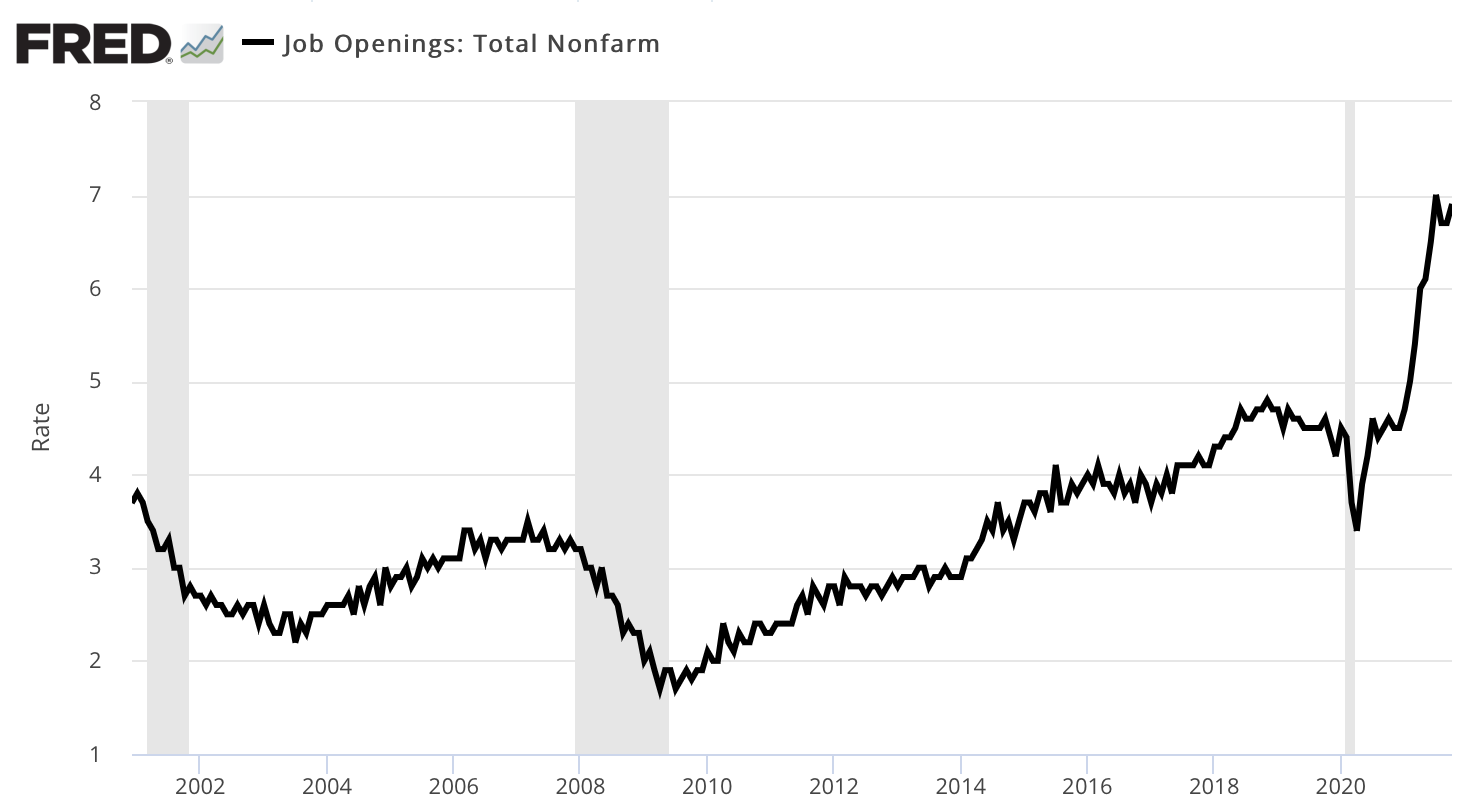

Those actions did not solve all the problems of the United States of America. But they did solve the specific problem of an under-stimulated economy. Today there are lots of job openings, and people say it’s the easiest time on record to find a job.

That doesn’t mean every non-working person in the country is lazy. But it means that either they are seeking a job in a very specific field that is still depressed by the virus, or else they face some non-demand impediment to working (disrupted child care, for example). Either way, a generic increase in demand won’t help, because demand is currently running very high.

And more to the point, the Fed is already taking gentle actions to slow demand. So anything you do to try to boost it with debt relief will end up being offset by a faster pace of interest rate increases. Stimulus is a kind of free lunch. But it’s not an unlimited free lunch buffet. Once you’ve done it, you’ve done it and you’re back in a world of tradeoffs.

During the long labor market funk of the Great Recession, I would always tell fussy economist types that they underrated the value of full employment and that one thing they would like about it is that when you have a full employment economy, all their fussy economist ideas are much more likely to be genuinely true. And now here we are in a world of tradeoffs and choices where helping student debtors would harm others via higher interest rates and less investment. And we’d be helping a relatively small and privileged minority of the electorate.

Debt relief benefits an affluent minority

So who are the student debtors? Well, it’s a minority of the population — as Matt Bruenig shows, among people in their late twenties and early thirties the median student loan balance is $0. For older households, owing student loan debt is even rarer.

There are some data issues about linking student loans to household income, but as Adam Looney’s work shows, all the different data sources broadly agree that the lowest-income 40 percent of the income distribution owes less than the richest 40 percent.

Whenever conservatives have a chance to accuse progressives of being regressive, they really go to town with it and in this case I think tend to overstate their case somewhat. There really are plenty of low-income people with high student loan balances, and precisely because they are low-income this debt can be a significant burden. I think it’s wrong to erase the fact that there are genuine hardship cases here and the desire to do something for them makes a lot of sense.

That being said, it is the case that broad student loan relief would be a transfer from the majority of Americans to a disproportionately affluent minority.

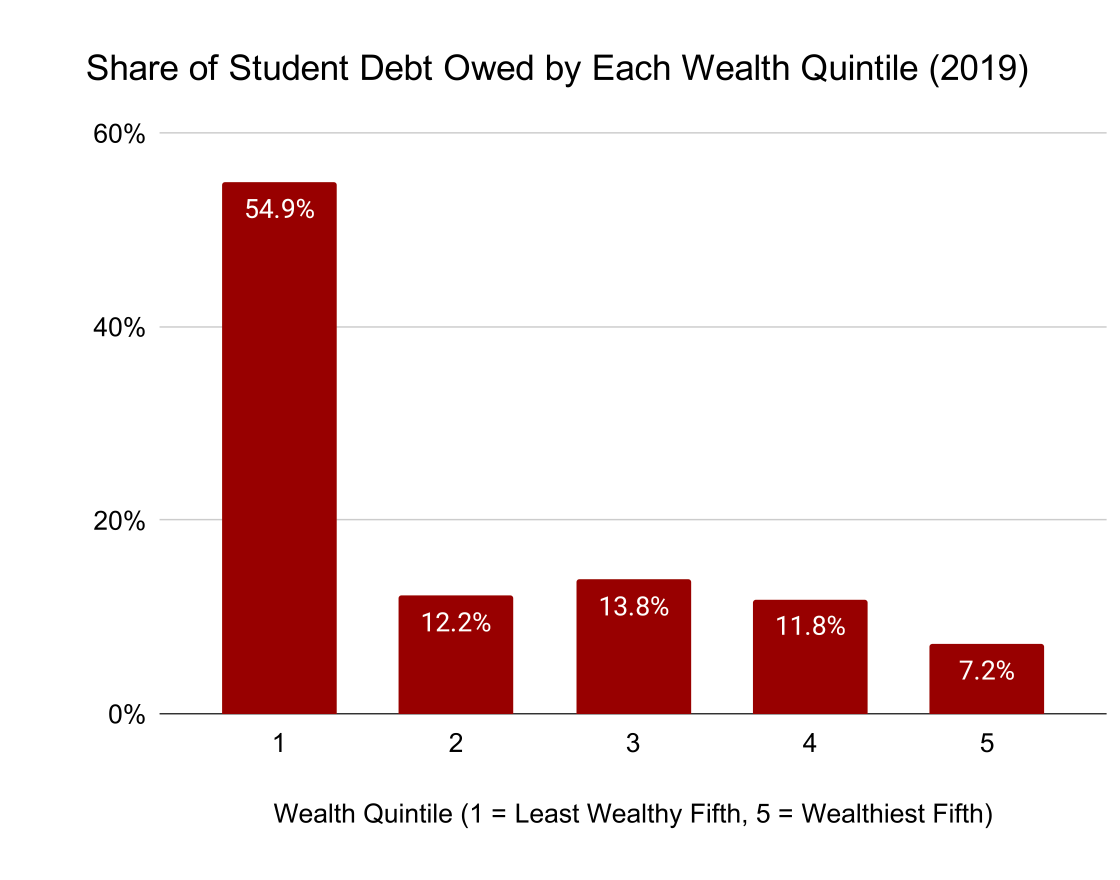

The contrary view you sometimes hear is that debt relief is progressive if you rank families according to wealth rather than income. Here’s another Bruenig chart:

This argument is sometimes amplified with appeal to the idea that universal loan forgiveness will narrow the racial wealth gap, an argument that I don’t think would make this idea any more appealing to the mass public but which is a powerful tool in intra-progressive fights.

I think this mostly illustrates the point I made last March that “wealth” is a weird and often misleading idea. Or to be specific, while it’s a very important and powerful idea for understanding the economic situation of wealthy people, it’s not very important for understanding dynamics facing the non-wealthy.

Consider the following four people:

29 year-old graduate of Stanford Law School working as an associate at a major law firm and renting an apartment downtown somewhere.

A single mother of two working in the Starbucks that’s on the ground floor of his building — during the pandemic her expenses dropped and she got some stimulus relief checks so she was able to actually use the corporate 401(k) match for once.

A homeless guy who when the store isn’t crowded just kind of sits quietly at a corner table for hours sometimes.

The recent Stanford grad’s dad, a divorced and retired cop who rents a place in Florida and lives off of his pension.

The way wealth data works is that a 401(k) is wealth but a defined benefit pension is not. So the barista is the richest person in this story, followed by the retired cop, followed by the homeless guy, and poorest of all is the lawyer — he has negative wealth unlike the homeless guy, who is at zero. In this world, 100 percent of the student loan debt is held by the poorest quartile of the population.

But I don’t think this is really informative. Higher education is not “wealth” because you can’t sell it, but it’s still valuable. The main reason that people take out student loans is that, on average, the financial upside of going to school outweighs the financial downside of the debt. Unfortunately, that average masks significant variation. And there is a very strong case that the loan-centric vision of higher education finance is bad. But debt forgiveness per se doesn’t do anything to fix the problems.

A bailout not a jubilee

In his influential book Debt, David Graeber dwells at times on the concept of a “debt jubilee” in which a government would essentially declare debt contracts unenforceable and forgiven.

The standard free market (or “neoliberal” if you like) critique of this is that if you fail to enforce old debt contracts you’ll make it harder for people to obtain loans in the future. There is probably some margin on which this is true. At the same time, American bankruptcy law is generally friendlier to debtors than European bankruptcy law. And far from making credit unavailable in the United States, our relatively lenient practices seem to encourage more risk-taking and entrepreneurship.

Meanwhile, during the Great Recession I certainly had the thought that a mortgage debt jubilee of some kind would not only boost the economy (we needed stimulus back then) but also that if banks got a little more skittish about handing out home equity loans and such in the future, that might not be such a bad thing.

But it’s important to remember that we’re not talking about the government cancelling debt that’s owed by evil banks or poorly performing colleges. We’re talking about the government forgiving loans that were made by the government. I would have a very different attitude about this, in particular, if the way that student loans worked is that the school fronts you the tuition and then expects you to pay it back over time. In that universe, a loan forgiveness program would be a way of punishing schools that saddled their students with too much debt. I think you’d still want targeted forgiveness (there’s no reason dental schools should be punished for successfully training dentists), but you’d be broadly in the universe of trying to reward sympathetic cases while punishing bad actors.

Check out the latest reporting by Melissa Korn and Andrew Fuller on NYU’s debt-tastic master’s degree programs. They write that NYU “is the worst or among the worst schools for leaving families and graduate students drowning in debt. Many of its graduate-school alumni earn low salaries, despite their expensive degrees."

NYU’s defense to this charge is essentially to argue that NYU only looks unusually bad because other schools don’t make as much data available and actually they are all bad:

NYU spokesman John Beckman said those numbers don’t reflect progress the school has made since its current president took the helm in 2016 and emphasized affordability initiatives.

The Education Department doesn’t publish data on programs with a small number of graduates. Mr. Beckman said that because NYU has so many large programs, more of its figures are made public and the data put the school “in a disproportionately disadvantageous light.” He also said NYU receives so much Plus money in part because its total enrollment is among the largest in the country, at around 52,000 students.

Inspired by a previous round of this reporting, I wrote last summer about how “There Are Too Many Scams in Higher Education.”

On average, American higher education is worth the high price. But there are lots of specific situations — mostly involving for-profit schools, graduate degrees, or schools with very low completion rates — where that’s not the case. An improving labor market and reporting from places like the Wall Street Journal is putting pressure on these programs to clean up their act. That’s a very positive development. But debt forgiveness at public expense would operate less like a jubilee than like a bailout of bad programs, which would be able to wink at future students and suggest they shouldn’t worry too much about costs.

We need real reform

The big problem with subsidizing higher education via low-interest loans is that it eliminates all kinds of quality control.

If Columbia University asked the government to finance a master’s degree program in data journalism that cost $160,000 they’d be told “no, that’s stupid.” And by the same token if you asked people to fork over $160,000 up front to do a master’s degree program in data journalism, nobody would pay for it. This whole niche of higher education just wouldn’t work, and whatever it is Columbia teaches you in the data journalism master’s program would just have to be learned on the job over the course of 2-3 years working in an entry level journalism job.

By contrast, if you were training doctors and nurses and dentists, you’d have a very strong case for public subsidy — it would be easy to make the argument that there is a broad social benefit to increasing the share of the population with these skills. Some people might say we shouldn’t subsidize doctors’ education because they earn high salaries. Others might say we should subsidize doctors’ education but in exchange reduce their compensation. Still others might say we should subsidize the education of even more doctors and let competition drive down the price.

For some fields — lawyers, say — a debt model really might make sense. But I think the best version of that would be that the law school itself would extend credit to the students it admits and the loans would be dischargeable in bankruptcy. That puts the onus for quality control on the school itself. Then the government could have a relatively straightforward program where people who agree to do certain kinds of public sector work for a certain span of time have their loans paid off.

Now obviously there’s going to be plenty of room for disagreement over exactly which programs are worthy of public subsidy and why and that’s fine — that’s why we have a political process. But if you go back to the original Morrill Act establishing public universities in the United States, it talks about creating schools “where the leading object shall be, without excluding other scientific and classical studies and including military tactics, to teach such branches of learning as are related to agriculture and the mechanic arts, in such manner as the legislatures of the States may respectively prescribe, in order to promote the liberal and practical education of the industrial classes in the several pursuits and professions in life.”

This is extremely vague and implementation is just kicked to state legislatures. But it is clearly asking the legislatures to make some kind of judgment about the educational needs of society — to decide which kinds of programs are valuable and which are not.

That’s exactly what the loan-based system doesn’t achieve. Instead, if you’re within the blessed circle of accredited institutions you can just spin up whatever programs you want and start recruiting students who pay through regulated debt. Even where we’ve made cursory efforts to crack down on shady for-profit operators, it turns out that nonprofit institutions can make cynical cash grabs too — often contracting out the actual operation of low-value online classes to the former purveyors of for-profit schools. The system stinks and it needs change.

The awkward inevitability of bipartisanship

And here’s where I land at the opposite end of executive branch unilateralism.

When it comes to stabilizing the macroeconomy, the president’s got to do what he can knowing that the opposition party’s interests are objectively advanced by the economy going bad. But the president can’t reform the whole basis of higher education finance in the United States through executive action. It really takes legislation. And realistically, it’s going to take bipartisan legislation. Not because bipartisanship is always better and not because of filibuster math, but because the coalition is awkward.

The Obama administration tried to curtail some of the worst abuses in higher education by promulgated regulations that would have made schools ineligible for student loans if they delivered consistently terrible salaries to their graduates.

But for reasons internal to the dynamics of the Democratic Party, this swiftly ended up being limited to just for-profit institutions. The higher education establishment rightly argued that a very disproportionate share of the worst actors were for-profits, and then leapt to the conclusion that traditional schools should be completely exempted. Then after regulating on that basis, it became a partisan controversy with Republicans as the defenders of private enterprise. When Trump became president, instead of leveling up by applying Obama-era rules to nonprofits as well, they simply rescinded the rules. Now Biden’s Department of Education is doing a new rule making process.

Actually fixing things requires us to get out of this ping pong and have progressives who are worried about student debt collaborate with Republicans who are skeptical of American higher education. They’re going to need to come up with a system that involves more direct subsidy and less financialization (as progressives want) but that in exchange involves more scrutiny of which programs exist — probably leading to more emphasis on training engineers and less on subjects with lots of leftist ideology and minimal quantitative work.

And of course the path to bipartisan legislation is inherently difficult and fraught, both in terms of ideological compromises, coalition infighting, and the general difficulty of getting anything done. That said, I think the people who’ve convinced themselves that there is some other path to fixing what ails higher education finance are just really wrong. The whole case on the merits for broad stroke student loan forgiveness hinges on messing up other aspects of macroeconomic policy. Now that we are appropriately stimulated, it doesn’t make sense. And of course one-off forgiveness is not reform at all. And one-off forgiveness with the implication that it will just happen again in the future is the opposite of reform. This is a big issue that requires a real solution with legislation, including the reality that shifting to direct public subsidy will necessarily mean more democratic oversight of the higher education system in ways that sometimes discomfit professors.

While I agree on the economics and the dire need for deeper reform, my biggest concern is actually the optics. 'The Dems are giving out a lot of free money, and it's only for people who went to college' seems tailor-made to build resentment. It's not just that it's regressive, it's that it's regressive in a way that's incredibly obvious to a normal person.

As someone who has 4 degrees (not bragging, just giving bonafides), made poor choices and good choices along the path, has advised and taught for over 29 years , and is very much part of the higher ed insider establishment, here is the simple advice I gave to my son who is looking at colleges:

1. If you’re in the top 10-15 percent of your undergrad college’s gpa when you graduate, the difference between public and private in terms of job or grad school opportunities is zip.

2. Colleges have made it much easier these days to get a double major in 4 years, so choose a major you love and a major that gets you a job. If those are the same major, even better.

3. If a department can’t tell you on its webpages within 2 clicks what jobs its majors get and if its first example in its placement page is “our majors go to grad school” that’s a warning sign.

4. You really only know what your parents do and don’t understand your career opportunities at 18 so over the next 4 years, intern, intern, intern. Don’t know in what? The BLS Occupational Outlook Handbook is a great way to learn what an occupation actually does.

5. This is the only time in your life that society will let you “find yourself” so take a variety of courses, read newspapers, read books, join clubs and, yes, take jobs and learn there as well. Everything you do in the next 4 years is basic training… you just don’t know what it’s for yet.

6. Never underestimate the blessedness of sitting alone under an oak tree reading a book.