Why hasn’t oil gotten even more expensive?

TACO equilibrium is keeping a lid on the futures market.

I keep trying to puzzle through the question of why the price of oil hasn’t risen even more as a result of the closure of the Strait of Hormuz.

When this war started, I didn’t know much about the details of the oil industry, but I did know about the short-term price elasticity of gasoline consumption — specifically, I know that it is low.

In other words, if gas prices spike, consumers don’t tend to cut back very much in the short-term.

Conversely, in the literature, long-run elasticity is actually pretty high. Credible commitments to durably higher gas prices (usually via gas taxes) mean that people buy cars that use less fuel. And the estimates in this body of literature are now almost certainly serious underestimations since E.V.s and plug-in hybrids have become so much better and more available; there would probably be even more available (particularly more electric trucks) if carmakers anticipated the kind of durably high prices that would make them more lucrative.

Technologically speaking, almost everyone could dramatically reduce their fuel consumption in the long-run by buying different vehicles.

But short-term elasticity is low: Your family owns the cars that it owns, and you live where you live. A minority of the population has a reasonable “shift to transit” option that would save them money, while others can carpool if they get desperate. But the mainstream response to short-term increases in the price of gas is to just pay the higher prices and be annoyed.

But in the face of a supply disruption, consumption has to fall somewhere.

More than 20 percent of the world’s oil normally moves through the Strait, and that oil is not going anywhere right now. To compensate, the price needs to rise high enough for people to cut consumption by 20 percent.

The price at which that would happen is really high — more like $150 a barrel, versus the current price of roughly $100. I’ve seen talk about how the American economy is much more resilient to oil shocks than it was in the past. This is true. It is harder than it used to be for higher energy prices to push the economy into recession. But in a sense that just underscores that prices need to accelerate a lot to reduce consumption — precisely because we are more resilient than we were in the 1970s, it is harder to push consumption down.

It turns out that the real oil industry is a lot more complicated than the oil futures market and that introduces a lot of nuance into this conversation. But we are also fundamentally in a TACO1 equilibrium: Traders reason that if prices did spike to a much higher price, that would be too politically painful for Trump, so he would back down and find a way to force Israel to as well. Therefore, any time oil gets bid up too much, the smart money starts selling. That means the price doesn’t spike and Trump doesn’t back down.

And yet, still the oil is not flowing, so someone needs to consume less oil — it just turns out that most of the action isn’t happening in the mainstream futures markets.

A crude explanation

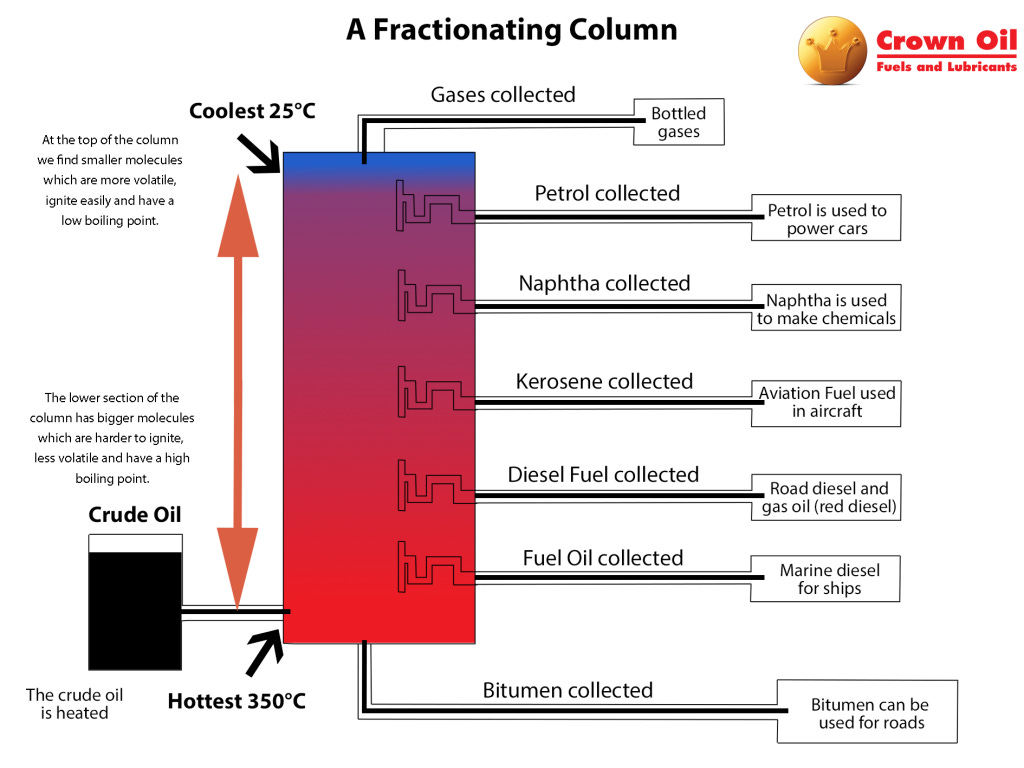

With apologies to chemists and industry specialists for oversimplifying, I think it’s important to understand that “oil” and “petroleum” are not really the names of specific things.

What comes out of an oil well is a mixture of different liquids and gases, and the specific mixture varies from place to place. These different mixtures are similar enough that it’s convenient to refer to them all as “crude oil,” and we say that there is a kind of facility called an “oil refinery” that takes crude oil and turns it into specific petroleum products.

The British company Crown Oil has a nice graphic.

But in reality, different barrels of crude are pretty different in their content. And refineries differ in the type of crude they’re set up to refine and what products they’re set up to make.

As far as I know, nobody actually uses crude oil as an end consumer; it’s purely an input into refineries. The refining process itself consists at least in part of separating out the different specific chemicals that constitute the crude, which works because different molecules have different boiling points. The stuff that boils coolest — things like butane gas and gasoline for cars — is considered “light” and the products on the other end are “heavy.” Crude oil itself is classified as light, heavy, or medium depending on its specific chemical content.

Long story short, gasoline, which is most salient to normal consumers, is a light product. The American crude oil that is least-impacted by these supply disruptions is mostly light crude that feeds refineries that specialize in making light products, and the most heavily traded markets are for light blends located in the Atlantic basin.

But the supply that’s been knocked out by the war in Iran is a lot heavier on average, and mostly feeds refineries in Asia that specialize in heavier products, which means the oil that’s getting bid up in the first instance is not the most widely cited oil price.

In the long-run, all the different crude blends should achieve equilibrium. But in the short-term, we’re seeing big divergences.

Hipster oil prices have risen a lot

Looking beyond the widely traded Brent and West Texas Intermediate crude oil blends, you can see much larger price movements in other markets.

The most notable of these is Russian crude. Prior to Trump’s war, the price of Russian crude oil was deeply depressed due to Western sanctions, and Chinese and Indian refineries were buying it at bargain prices. But Trump lifted sanctions, which has led the market price of Urals crude to converge with the Brent/W.T.I. global standard. Lifting sanctions basically doubled the price of Russian crude, a huge windfall for Putin that has pushed the global average price of crude oil up by more than you can see from eyeballing the main indexes.

Bloomberg reported on Friday that obscure hipster blends like Labuan (from Malaysia), Minas (Indonesia), and Bach Ho (Vietnam) are trading for $10 more than the widely covered Brent. This is even impacting certain blends such as Johan Sverdrup (in the North Sea) and Mars (in the United States).

Watch the products

The deeper story is that actual demand destruction is taking place in the market for distilled petroleum products.

India is rationing commercial users’ cooking gas to try to preserve it for households, but there’s clear evidence of shortages, with people switching to dirtier fuels like wood and dung.

One European airline has already canceled flights due to expensive jet fuel and more are preparing to follow suit. The petrochemical industry is facing shortages of naphtha (a base material for petrochemical products), and the maritime shipping industry is facing shortages of fuel for ships. This is largely because Asian refineries can’t get the crude they need, so they’re producing less.

With products in short supply, refiners are scoring windfall profits on diminished output. In the longer-run, elevated prices for distilled products should lead to refineries bidding higher and higher for crude oil and, because there are lots of partial substitutabilities between different blends, the whole market should eventually move like it’s being pulled by a string.

In theory, the point of a futures market is that prices today reflect events that are weeks or months in the future.

But the TACO principle says that Trump can shrug off a crisis in South Asian households’ ability to get cooking fuel but will back down if domestic gasoline soars to new record highs here at home. So the market is still betting on that not happening.

One thing many commentators have noted is that the mere fact that the United States is a net exporter of petroleum does not insulate us from the price impacts of this supply disruption.

That is true. But it is also worth saying that it genuinely is cushioning the blow. The monetary value of our exports is rising, which bolsters the value of the dollar and gets us access to cheaper foreign goods.

In countries that import their oil (i.e., most countries) this means not only higher energy prices but general currency depreciation and higher prices for everything.

The fact that a large majority of the economic suffering unleashed by this war is borne by non-Americans illustrates the limits of TACO as a principle. Whatever the economic pain point that would lead Trump to back down, the lead-up to it has inflicted a larger degree of suffering per person on a much larger set of mostly much poorer foreigners, especially in Asia.

“Trump Always Chickens Out” is a concept first developed on Wall Street to explain stock price movements in the wake of tariff threats. The basic idea is that only suckers would panic sell in response to an announcement of something disastrous, since Trump predictably responds to stock market crashes by working out a “deal” that withdraws the disastrous proposal.

The question I have is that even if Trump wants to TACO, how much leverage do the Iranians have to extract humiliating concessions or even inflict political pain on Trump for the sake of it? What we're seeing here is that it doesn't take an old fashioned flotilla blockade to close Hormuz, just enough of a threat where shipping companies won't risk sailing through it because of a chance (even a low one, say 2% chance) that their tanker is hit badly. Insurance companies are not going to underwrite any policy until they sense the risk of transit is near zero.

Part of me wants to buy oil futures because I think the market is too stuck on the tariff TACO experience where Trump really did have unilateral control (and trading partners did not have much leverage), but here even though Iran is pretty spanked in a conventional military sense they can still go Hyper Houthi and lob Shaheds and other munitions for what's probably indefinitely and the US is left playing a very expensive game of whack a mole which still probably won't provide enough stability to return the strait to status quo ante.

The other short term adaptation that's available now to some people that wasn't in the past is remote work. Obviously this takes cooperation of the employer, but in a real crunch I suspect it would marginally increase elasticity compared to the seventies crises.