Universal health insurance is a winning fight worth having

Affordable healthcare for all is the progressive message that works everywhere

Hey folks, this is Marc the Slow Boring Intern here with a piping hot take — a system where the government provided everyone with health insurance would be much better than the status quo, and in both political and policy terms, it strikes the right balance between ambition and viability to be worth fighting for.

Part of fighting for it means trying to recruit allies rather than expel heretics, and that in turn means displaying a little more precision than you sometimes see from the Medicare-for-All movement.

But the biggest part of it is convincing mainstream Democrats that if you want to avoid counterproductive political rabbit-holes, you have to present something exciting that’s worth fighting for. Broad, universal programs that help people in concrete, material ways are the popular face of progressive politics that has a fighting chance across America’s political geography. Health care has been Democrats’ signature issue forever. And while they shouldn’t be politically reckless about it, they can and should be more ambitious than Joe Biden’s campaign proposals.

The status quo is bad

The health insurance problem in America boils down to two issues:

There are 28.9 million uninsured people. Nobody should be uninsured.

A huge amount of the people who are insured are insured poorly and almost everyone who is insured is insured through their employer. Employers mostly shouldn’t handle health insurance, and health insurance should not be so insufficient for so many.

The first point is a real tragedy. It is hard to quantify exactly how many deaths directly stem from lack of health insurance, but I think the most basic point for why lack of insurance is such a harmful injustice is that it makes people afraid to go to the doctor. When people are afraid to go the doctor, they don’t go unless it’s an emergency.

Research shows this has dire consequences. People who are uninsured often skip important screenings like prostate exams or mammograms — if they do get cancer, it’s caught later, meaning it’s more likely to be advanced stage and lead to death. If uninsured people have chronic conditions like high blood pressure, they are less likely to have check-ups, which means they’ll have more emergency visits down the line. Preventative health care is important, and it saves lives. People should not fear the cost before they decide to go to the doctor.

When uninsured people do have emergencies — often because of the unaffordability of seeking preventative care — they are charged huge amounts for their emergency care. In most cases, they’re not going to be able to pay this amount. When patients can’t pay, they fall into medical debt, which affects 137 million Americans. Two-thirds of people who file for bankruptcy cite medical issues as a key contributor, and these stats are from before the pandemic.

Nobody should have to suffer this way, afraid to go to the doctor for routine reasons, and then straddled with debt after probably-preventable emergencies or curable-if-caught-earlier cancers. Obama brought the number of uninsured people down from around 44 million when he was first elected to around 27 million when he left office. Under Trump, the number has increased to around 29 million. Biden’s plan would likely bring insurance to between 15 and 20 million people, which is an alright first step, but it still leaves around 10 to 15 million uninsured, and that’s before factoring in those who lost jobs (and health insurance) during the pandemic and associated lockdowns.

Even the insured have big problems

There is a bit of a myth espoused by some centrist Democrats and conservatives that everybody on employer-tied health insurance “likes” their insurance. Biden said exactly this at a Democratic debate last November.

Now, at some level, insured people do like being insured. A poll done by the Kaiser Family Foundation and the LA Times found that 72% of those with employer-tied insurance said that the word “grateful” described their feelings about their insurance.

This is certainly logical — being insured is way better than being uninsured, and I too am grateful to have health insurance. But this gratefulness does not imply perfection, nor even something close. For tens of millions of people who are insured, their insurance is completely insufficient. 40% of Americans who have employer-sponsored coverage have had affordability problems with their health-related costs, whether that’s for prescription drugs, co-pays, or monthly premiums. The majority of those people with affordability problems have cut spending on necessities like food, clothes, or other household items. According to the same poll that measured high amounts of gratitude, over 3 million people cut back on food to pay medical bills while they were covered by their employer-tied health insurance.

Nonetheless, being underinsured is better than not being insured at all. And when people only have insurance because of their job, they fear leaving their job. This phenomenon is known as “job lock,” and it’s not good for the economy. One study showed that among workers with employer-sponsored health insurance, there is between a 15 and 25% reduction in turnover.

You can understand why workers may be more reluctant to switch jobs, since 54% of Americans on employer-sponsored health insurance say that someone covered by their plan has a chronic condition. That chronic condition probably needs routine check-ups that usually discover no emergent problems. Nobody wants to pay tons of money for that check-up, but that’s how much it costs. Why would they leave their job — even if it sucks or it doesn’t fit their strengths — when it offers them massive discounts for those expensive check-ups (or emergency visits) they or their family member need?

The “job lock” decreases labor flexibility, which is key to helping people find jobs they’re good at in places they’ll thrive in. This means happier people, and if that isn’t enough for you, rest assured that happy people are also really productive and good for the economy.

Tying health insurance to your job also means that if you lose your job because your company is downsizing or going through a pandemic, the fall is much deeper. Not only will you lose your income, but you’ll temporarily lose access to affordable healthcare. This is wrong. One’s health insurance (and therefore ability to pay for healthcare) should be held constant regardless of exactly whether and where they are employed.

Bidencare is a Band-aid

Joe Biden’s health plan addresses some of these problems. He plans to enact a public plan he calls a “public option,” which would be sold on the Obamacare marketplaces to help low-income Americans get health insurance. This would reach poor Americans in states that refused to expand Medicaid after the ACA passed. It would also potentially reduce costs for existing marketplace customers and in turn help some of the uninsured who can’t afford existing plans.

But Biden goes out of his way to preserve the employer-tied system. The use of the word “option” makes it seem like people could choose it over their employer-tied health insurance. But unlike in some other plans proposed by center-left Democrats (like Buttigieg’s or CAP’s), this is unlikely. Biden’s plan doesn’t allow employers to use the public option for their employees and it doesn’t allow employees to use their employers’ premiums to pay for it. Employers could simply drop insurance altogether and pay workers more, but if they do that, they’ll lose valuable tax breaks for job-linked health care such that the pay raise won’t be equivalent to the money the company saved.

We shouldn’t dismiss the value of bringing health insurance to 15-20 million people. But Biden’s plan still leaves millions uninsured, and does nothing to address the underinsurance, healthcare instability, and job-lock implicit in the mainstream private insurance market.

The political case for going bigger

Presented straightforwardly, single-payer health insurance is popular. Here’s a list that a libertarian think tank put together of the five most recent nationwide polls they’ve tracked on single-payer healthcare:

These 5 polls aren’t outliers. The same think tank has a list of the 24 single-payer polls they’ve tracked since March 2019, and the averages are about 51% in favor, 38% opposed, and 10% who don’t know. That means single-payer would be favored by the majority of the electorate, even if everybody who didn’t know enough about it made up their mind in opposition.

More generally, public health insurance programs are popular. There is broad support for Medicare (77%) and Medicaid (75%) and little support for cutting spending on either, which Republicans have repeatedly tried to do in the last 4 years. In 2017, when Trump was floating the idea of cutting Medicaid, just 12% of Americans agreed with him. That same year, Pew found that just 15% of Republicans and 5% of Democrats supported cutting Medicare spending, which Trump has also proposed doing.

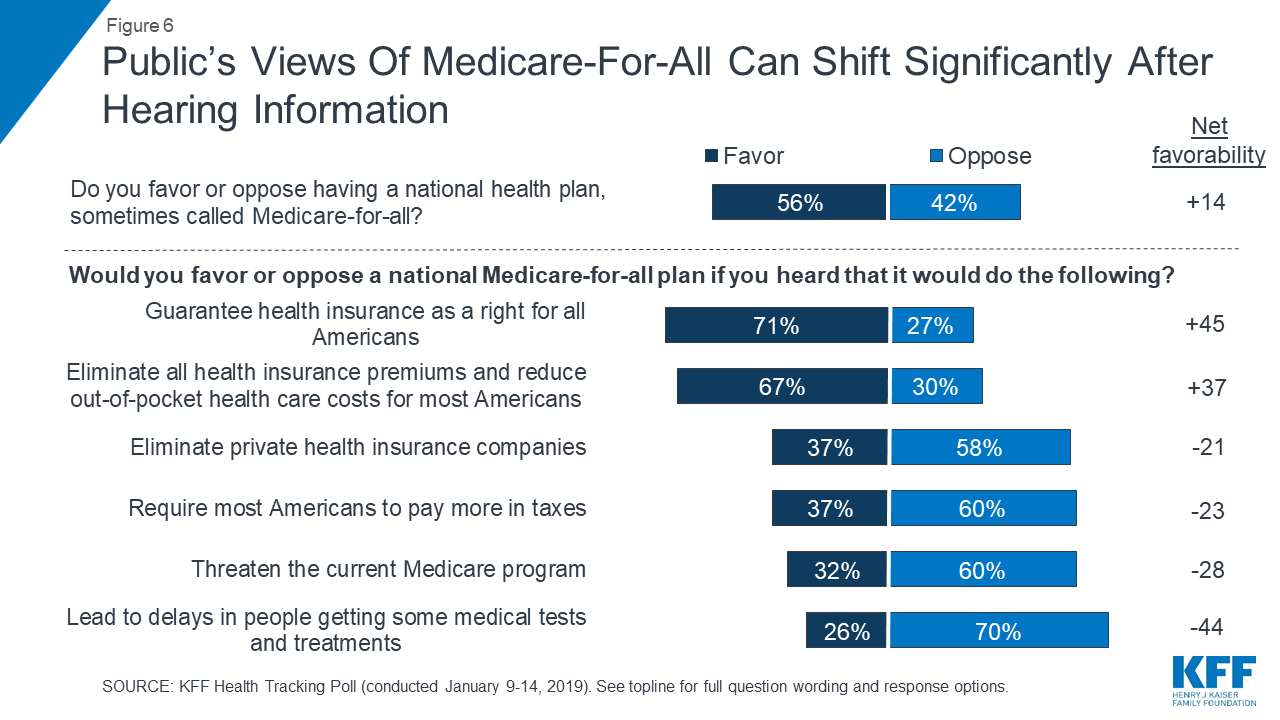

Now it’s true that support for Medicare-for-All varies a lot depending on what aspects of it you highlight.

But this is typical of many policy issues, and a few of the items on this list are actually even more misleading than just asking about single-payer without getting into the specifics. You could poll any government program and watch as its popularity falls if you tell the respondents that their taxes will go up or that it threatens other things they like.

Even moderate Democrats generally acknowledge that health care as a subject is a topic that plays to Democrats’ advantage, and unlike on many other issues, “government health insurance for all” is a topic where we have real life examples of politicians like Tammy Baldwin and Katie Porter running and winning tough races while embracing it as a goal.

Compared to arguments about white-privilege-based diversity trainings in the federal government or a promise to decriminalize HIV-positive people failing to inform sex partners about their HIV status, or even just to ban assault rifles, an argument about expanding public healthcare programs plays across a much broader swathe of political terrain.

80% of Americans say they dislike “political correctness,” but 77% of Americans, including 70% of Republicans, like Medicare. Bold plans that effectively deliver material improvement to vast swaths of Americans — rather than just the 5% of them that can get a public option on the Obamacare exchange — might seem riskier than super-narrow ones, but they also draw attention away from politically toxic cultural battles and towards the tangible things that Democrats can do for people.

A message like “we can make it so you don’t have to worry about how you’re going to pay for a doctor’s appointment” has real political upside, but only an ambitious plan can make this actually true for most people.

A more ambitious plan is also harder to co-opt. Democrats desperately wanted to focus the 2020 Senate election races on the narrow question of the ACA’s pre-existing conditions protections. But it wasn’t hard for Republican Senators to just decide they also wanted pre-existing conditions protections, which is exactly what swing-state incumbents like Joni Ernst and Susan Collins did before easily holding onto their Senate seats. A push for a government guarantee of insurance can’t be ducked by the opposition or dismissed by the media as boring.

Ambitious plans that materially improve most Americans’ lives — not just the 5% getting the public option through ACA marketplaces — make people pay attention in a way that can’t easily be diverted.

Changing Minds

To gain credibility, universal health care advocates should probably drop some misleading rhetoric that now leads people to tune them out. The first type of mistake people make is saying that progressives’ Medicare-for-All bill is simply what every single other developed country has. The plan outlined in the bill covers dental, vision, hearing, reproductive care (including abortions) and mental health care while promising no premiums, deductibles, or copays, and a cap of $200 of out-of-pocket spending on non-preventive prescription drugs for people whose incomes exceeds twice the poverty line.

Many European countries have universal systems that aren’t single-payer. And the Nordic social democracies, which do have a single-payer system, generally do not have a system like this with basically no cost-sharing. Norwegians pay between $19 and $42 per primary care visit and between $30 and $46 for specialist visits, though every adult has a deductible of around $500 above which the government will cover the rest. Denmark has copays too, with a cap of $538, and they don’t pay for adult dental care. Neither does Sweden for people over 23. In Finland, copayments are 20% of all health expenditure, averaging around $850 a year per person. Iceland’s out-of-pocket costs are over $800 per person.

Are all these countries doing way better than America, where out-of-pocket spending is over $1200 a year? Of course. But are their plans substantively different from Medicare-for-All? Yes, hugely — Finland and Iceland’s out-of-pocket expenses are closer to $1200 than they are to $200!

100 percent taxpayer-financed coverage of every conceivable health service is a fine aspirational goal, but it remains an aspiration even in Sweden and Denmark because everywhere you go, there is a tradeoff between services and taxes. There’s also issues of moral hazard and skyrocketing healthcare costs when people find out the government is always on the hook, and I haven’t even gotten into these.

By flattening all plans into “everything related to healthcare is free pretty much always” and “other,” we lose the ability to make distinctions between plans that put us on a path towards government health insurance for all and things that don’t.

For example, Pete Buttigieg’s health insurance plan was also a public option, but it allowed businesses to get the public option for their employees, unlike Biden’s. This difference would’ve allowed tens of millions more people to transition from employer-tied health insurance to government-funded health insurance, while Biden’s plan would by and large preserve employer-tied health insurance. Buttigieg’s plan would have been a much more meaningful step toward the government-health-insurance-for-all vision and if our goal is to recruit allies and move closer to it (as opposed to ideological purity), then we should be willing to recognize that.

Setting a goal

Government health insurance for everyone is not going to happen in the short-term. Something like 50ish percent of House Democrats support the hyper-ambitious Medicare-for-All bill; the President-elect does not support it; and it has limited backing in the Senate. So in keeping with the Slow Boring ethos that politics cannot merely be idealistic dreaming, what should we do knowing that government health insurance for all cannot be accomplished at the moment?

We should set it as our goal.

Once the goal is set, we can move forward with whatever change is possible at the moment. We can support ideas that move us closer to government health insurance for all that might be a lighter lift in Congress. Medicare for Kids, for example, or a public option that is actually an option for everyone, or even just lowering the Medicare age by 5 years. We can expand Medicaid, and challenge state Republicans in states where they have refused to, and dare to make these expansions a central part of the campaign, given Medicaid’s overwhelming popularity. And we should push Democrats to at least adopt the same goal and propose — and then support — steps in that direction. We should enlist primary challengers to focus on this issue (and on challenging its opponents), rather than a huge grab-bag of policy fads and culture wars. We can notice and point out differences between plans along the lines of which ones move us closer to our goal.

Democrats need to get behind widely-accessible plans bold enough to excite enthusiasts, generate media attention, and ameliorate huge amounts of suffering, while also being willing to play the incrementalist games that our political system —with its geographical weighting — demands. Universal government health insurance fits this bill.

Big ups to Marc the intern. I'd bet it's intimidating to write the first article for a website NOT written by it's founder and one of the best-known policy writers in the United States, about an issue as complicated and aggressive as universal healthcare. Good work, the article turned out great. It matches the style and tone of Slow Boring and has depth to it.

Nice to see Intern Marc flexing his writing skills! Great stuff.