The experts underrate full employment

Good things happen when people get jobs

In “The Media’s Lab Leak Fiasco,” I mentioned off-hand that casually scanning what you see people saying on econ Twitter would be a very poor guide to what the consensus is inside the economics profession. Alex Thompson did a story about Larry Summers’ criticisms of current macroeconomic policy that featured an (erroneously anonymous) quote from Jason Furman, another former top economic policy official under Obama, in which Furman opined that in his view, most macroeconomists agree with Summers but aren’t saying so.

The conversation about this on Twitter then went off the rails (as conversations do), with a lot of over-the-top stuff about cancellation and people getting mad.

My view is that in this case, while there are certain aspects of the American Rescue Plan that are non-optimal, the Biden/Powell synthesis on macroeconomic policy is fundamentally superior to the consensus view in the economics profession. To be a bit provocative, I would even call it the Trump/Biden/Powell synthesis, noting that when Donald Trump pursued a strategy of simultaneous fiscal and monetary loosening in 2017-19, he was widely criticized by mainstream figures.

The structure of modern Democratic Party politics is such that Biden likes to align himself with experts and expertise. And there are certainly extremely well-credentialed economists in the Biden administration, starting with Treasury Secretary Janet Yellen and CEA Chair Cecilia Rouse. But Rouse’s academic work is not about macroeconomic stabilization issues. By contrast, the two other CEA members — Jared Bernstein and Heather Boushey — are people who I have long known and admired for their dissident, outlier views on this topic. And while I think that they are great, Bernstein’s PhD is from the Columbia School of Social Work, and Boushey’s is from the heterodox department at the New School. Powell, similarly, is a lawyer rather than an economist.

I think it is fair to say — not as criticism but as praise — that the Fed and the administration are doing something outside the expert consensus because the consensus wrongly underrates full employment as an objective.

The question of symmetry

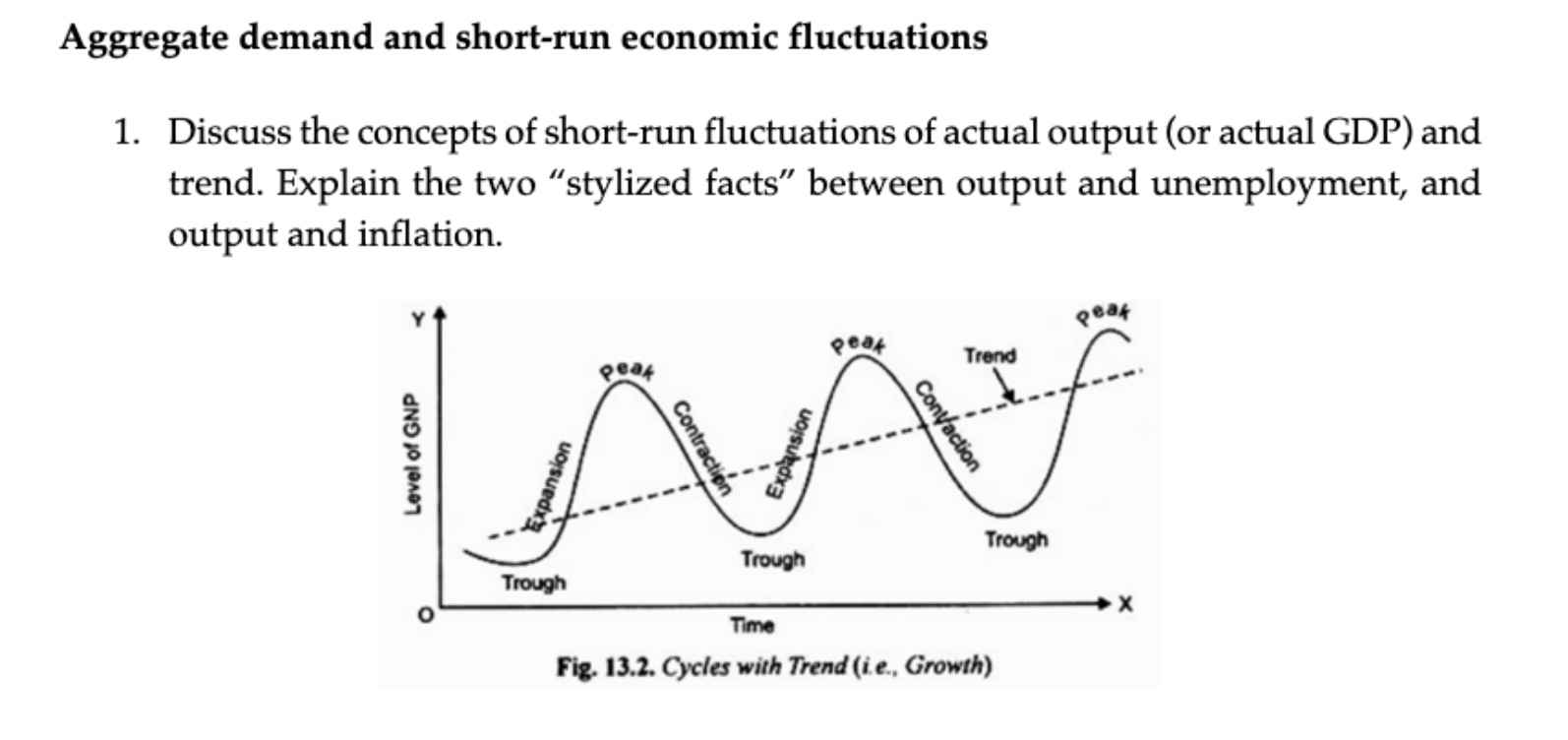

The dominant idea in macroeconomics that I think is at odds with both reality and normal people’s thinking is that there are symmetrical “fluctuations” in the state of the business cycle relative to a long-term growth trend.

This sample quiz question captures the dominant view in a nice, simple form:

Two things follow from this view that influence criticism of the Biden administration:

One is that the fluctuations aren’t important relative to the slope of the long-term growth trend. So expending political capital or fiscal capacity on short-term recession fighting rather than long-term growth-raising is a mistake.

The other is that fluctuations are symmetrical — it is just as bad to go over the line as under the line, and the goal of stabilization policy is to reduce the amplitude of the fluctuations because fluctuations are annoying.

Now to be clear, the alternate view is not unheard of in the academic literature. Nor is it distinctively left-wing. Indeed, among recent academics, its most prominent proponent is probably Milton Friedman, who described a “plucking model” where a recession is like tugging an elastic string and then it snaps back to full potential.

But again this is not a distinctively Friedman-ite idea. In Chapter 22 of “General Theory,” Keynes writes that “the right remedy for the trade cycle is not to be found in abolishing booms and thus keeping us permanently in a semi-slump; but in abolishing slumps and thus keeping us permanently in a quasi-boom.”

On the fluctuations model, what Keynes is saying there doesn’t make any sense; he is implicitly relying on something like the plucking model.

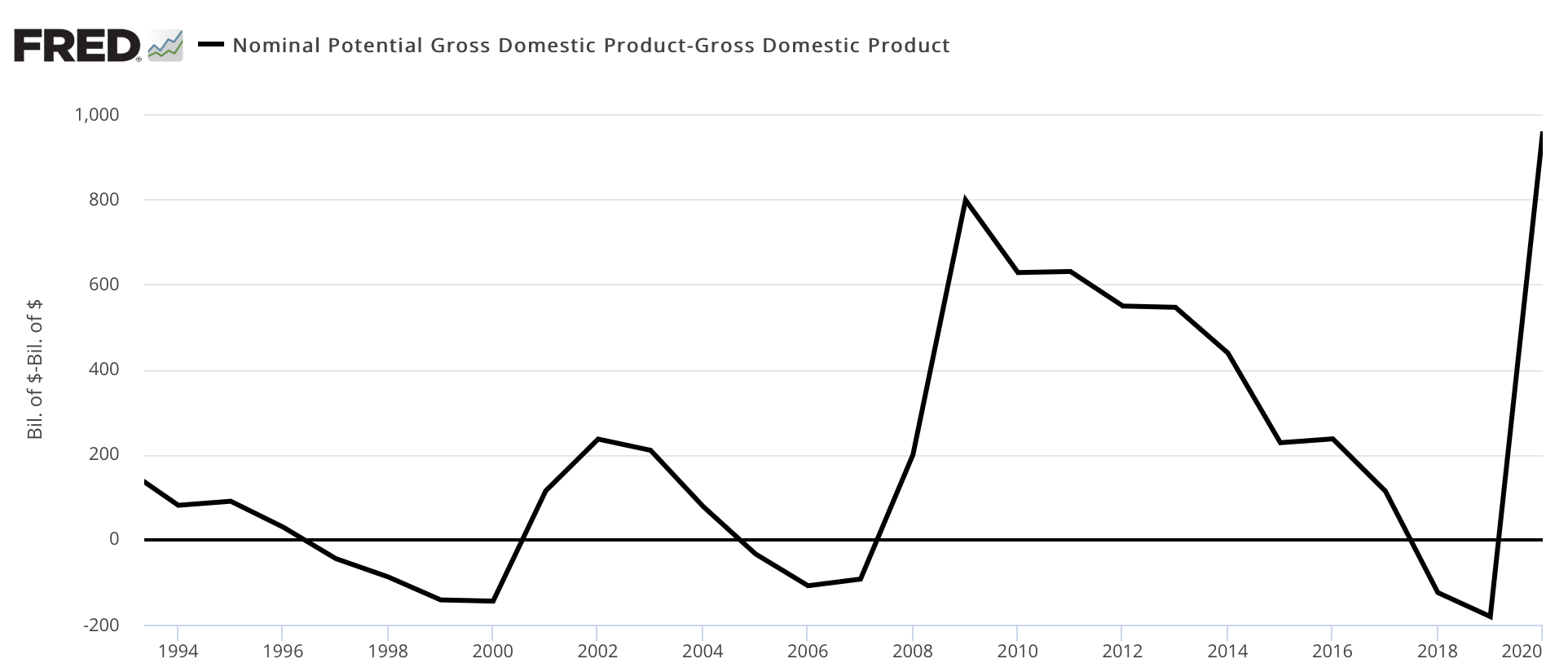

Another way of looking at this is to look at the Congressional Budget Office’s work on potential vs. actual economic output. Here I made a chart of potential output minus actual output — giving you the history of the output gap according to the CBO. Note that on this view, 1997, 1998, 1999, 2000, 2005, 2006, 2007, 2018, and 2019 are all examples of years in which the economy was running too hot.

On the fluctuations account, policymakers should theoretically be equally eager to avoid the state of the economy in 2016 as they are to avoid the situation of 2019, as they both reflect roughly $200 billion deviations from long-term sustainable output. And the boom year of 1999 was similar in the scale of the deviation from the jobless recovery year of 2004.

A plucking account not only disputes that symmetry; it suggests that the potential of the economy has been misestimated. That the boom years of 1999 and 2019 represent the “true” potential of the economy to produce things, and that every year between them represented a certain amount of falling short. Imagine the red line on the graph below as the ‘true’ potential GDP.

I think this Red Line view of the economy is correct. I think it corresponds with the mass opinion that 1999 and 2019 were really good years and that 2006-07 were just okay, and that even though 2016 was a big improvement from what Obama inherited, the economy was still really weak. And I also do have on my side two Famous Dead Economists — one identified with the political left and the other with the political right. Plus the Fed Chair agrees with me and so does the current president and his predecessor. So I absolutely do not want to talk you out of this view.

But I do think it’s important for you to understand that it is a non-consensus view among economists. In part because once you understand that, you’ll see that it’s more vulnerable to disruption than it may seem.

Many economists declared victory too soon

When Obama first took office, the United States was clearly in the midst of a severe and worsening recession. Action was taken to combat the recession, and the situation improved. Then, as the recovery gathered steam, it became a bit harder to say exactly what was going on. By the fall of 2015, the unemployment rate was around 5%, which is a pretty good number by the standards of the past 50 years of economic history.

For comparison’s sake, note that the unemployment rate never dropped below 5% during Ronald Reagan’s time in office.

That said, the prime-age employment rate was telling a different story. By that metric, the economy never re-obtained its 1999 peak during the Bush presidency, and by 2016, we were still short of the Bush-era peak.

This wound up generating a fair amount of debate. Here’s a senior economist at the International Monetary Fund writing in the spring of 2015 “Is the U.S. approaching full employment? It's close.” A March 2015 story in the Wall Street Journal reported that Fed officials believed the U.S. economy had achieved full employment. A January 2016 NPR story said, “bingo, we're basically there at full employment.”

By this point, Obama’s economic team had run the numbers and concluded that only a small fraction in the decline of the labor force participation rate was due to cyclical factors — i.e., that we were close to full employment and the rest of the fall was about something else.

Around this time an economist name Erik Hurst wrote a widely discussed paper arguing that the mystery residual was that video games had improved, so men didn’t want to work anymore.

But to be clear, Obama’s economists didn’t have this view because they are secret right-wingers. They were offering a progressive diagnosis of structural barriers to labor force participation, arguing that the economy needed criminal justice reform, investments in child care, and a big push on infrastructure to move forward. There were also conservative structuralists who were obsessed with the need to repeal the Affordable Care Act or revise Disability Insurance benefits. Thanks to the very meager policy legacy of the Trump administration, we now know all that was wrong and you could substantially boost employment with neither progressive nor conservative reforms.

Trump’s stimulus experiment

Donald Trump comes into office, fails at ACA repeal, then enacts a giant deficit-financed tax cut while also cutting deals to raise both military and non-military spending.

Larry Summers denounces the tax bill in October of 2017, arguing that “the economy is very close to or at full employment.” Trump also starts bullying the Fed to keep interest rates low (I said Trump was right at the time), which attracts a bunch of criticism, but eventually the Fed comes around to Trump’s line of thinking.

And what happens next is the prime age employment rate keeps growing until eventually things fall off the cliff with the pandemic:

Now because of the pandemic, there is just enough ambiguity here for the people who were wrong in 2015 and 2016 and 2017 and 2018 to instead maintain that they were correct. Every serious analyst that I can find said something like Summers’ “very close to full employment” that leaves them enough wiggle-room to be unrefuted.

And of course, there are our friends at the CBO who maintain that the 2018-19 economy was operating “above potential” and that the downside consequences of that just didn’t materialize yet. That to me is the backdrop of the debate. Biden is aiming to restore the economy that existed in the winter of 2019-20, and the idea that he should try that is simply more heterodox than a lot of people realize.

Biden is more heterodox than he lets on

The contemporary Democratic Party is in the grips of an ideology of expertism, which is distinct from (though related to) the actual idea of listening to experts. And one way that manifests itself is that while Trump would proudly tell you that he’s brushing off the ivory tower losers who don’t understand the pain of unemployment, Biden keeps citing fake academic consensus in favor of his policies.

Probably the most egregious case of this was Biden speaking at an Anderson Cooper town hall when he said “this is … the first time in my career that there is a consensus among economists left, right, and center that is over- — and including the IMF and in Europe — that the overwhelming consensus is: In order to grow the economy a year or two, three, and four down the line, we can't spend too much.”

This is just not true.

There was both a lot of disagreement about the desirability of spending and then also disagreement (the Summers point) within the “spend more” camp about the merits of the kind of spending that was in ARP as opposed to saving the money for infrastructure.

Then at a May 27 event at Cuyahoga Community College, Biden says:

When it comes to the economy we're building, rising wages aren't a bug; they're a feature. We want to get -- we want to get something economists call “full employment.” Instead of workers competing with each other for jobs that are scarce, we want employees to compete with each other to attract work. We want the -- the companies to compete to attract workers.

That kind of competition in the market doesn't just give workers more ability to earn a higher wage, it gives them the power to demand to be treated with dignity and respect in the workplace. And it helps ensure that America -- when you walk into work, you don't have to check your right to be treated with respect at the door.

This is like music to my ears. This is the gospel I picked up when a review copy of “The Benefits of Full Employment” arrived at the slush pile at The American Prospect in 2004. The authors of that book, Dean Baker and Jared Bernstein, were pretty distant from the mainstream of the economics profession. But Bernstein became a Biden advisor back in 2009 and is close to the president today. Around this time Baker was also co-authoring pieces on full employment with his then-colleague Heather Boushey, who today has joined Bernstein in the White House. The Open Philanthropy Project gave money first to Ady Barkan’s Fed Up campaign and later to Sam Bell’s Employ America, both of which pushed versions of this message.

And I am proud to have personally played a role in popularizing some of these ideas.

But precisely because I am so familiar with this work, I can promise you that it does not reflect a broad academic consensus. Rather, heterodox ideas have gained political strength either because policymaking has gone off the rails (the orthodox interpretation) or because the orthodoxy is wrong.

It’s important to note that these are related. Orthodox skepticism that full employment raises real wages by improving worker bargaining power helps explain orthodox eagerness to throw in the towel prematurely on boosting employment. If you don’t believe there are any particularly large benefits to full employment, then you’ll be inclined to seize on any data supporting the idea that it’s already arrived.

A biased worldview

The people on the other side of this are all very smart, and they have PhDs and can do more math than I can.

But I really think this is a case where occupational and class bias has seeped into the analysis. Economists do not, personally, have jobs where their ability to bargain for higher wages and better working conditions is closely tied to the state of the overall economy. It’s less-educated people in working-class jobs who have a lot to gain from full employment. If you’re cooking food or cutting hair or cleaning floors, there’s no such thing as a competing offer that you can use to get a pay increase unless you’re living through a period of an overall very strong labor market. Even just what the academics would call the “search frictions” involved in trying to ascertain whether or not you could get a competing position for slightly higher pay could be overwhelming.

A hot labor market is different.

The minimum wage in Pennsylvania is $7.25 an hour. But when I was there last weekend, I saw a bunch of places with signs in the window advertising retail and food service jobs for pay starting at $11 an hour. The sheer ubiquity of those signs matters. It means that anyone just living a normal life will become aware that those signs are up in a lot of places. You don’t need to search for a job to know that better-paying ones are available. And when you ask your boss for a raise because you could walk into Sheetz or Five Guys and earn more, your boss has also seen those signs without researching it.

And I think that not only does this give experienced workers the opportunity to secure real wage increases, it also has a bunch of other knock-on effects.

I don’t think it’s a coincidence, for example, that crappy for-profit colleges blossomed during the long labor market slump. Making it easier for people to get jobs and raises is good on its own terms. But forcing the education sector to raise its game and do more to deliver real results has longer-term benefits. Full employment means that skill at recruiting and training raw workers becomes a valued attribute in managers, which in turn improves the quality of the workforce down the line. Full employment means that stubbornness and aversion to change are punished more severely, so companies that don’t succeed in adopting productivity-boosting innovations will be put out of business and replaced by those who can.

Beyond that, as Bernstein wrote as far back as 1999, there is a reason Martin Luther King put full employment at the center of the civil rights agenda. For all the attention paid to diversity and inclusion in white-collar workplaces, the vast majority of workers have working-class jobs where Black candidates appear to be subject to meaningful amounts of discrimination. Full employment lifts up people on the margins of the labor market, punishes discrimination, and even reduces “rational” or “statistical” discrimination (I’m scare quoting here because I don’t love that language) by genuinely changing the calculus about how much sense it makes to be choosy.

A big fucking deal

To use one of Biden's favorite (secret) phrases, full employment is a big fucking deal.

But it’s not seen that way by the mainstream economists. The mainstream view emphasizes fluctuations rather than plucking, thus systematically undercounting the economic losses due to non-full employment. The mainstream view is also unreasonably wedded to marginal product theories of wage determination and underemphasizes the labor market monopsony issues that make it very challenging to secure raises absent full employment.

And especially in terms of intramural fights among Democrats, I think the mainstream view underrates the role of full employment in ameliorating long-term problems like educational quality or structural racism.

Centrist Democrats fall too much in love with various “reform” schemes for improving education, and more left-wing Democrats are so skeptical of capitalism that they almost don’t want to believe that a market economy can be made to work really well for everyone. Summers, in particular, seems to grossly overstate the economic value of marginal additional spending on America’s very mismanaged transportation infrastructure system.

I wish I could promise you with 100% confidence that there is absolutely no way, no how that the Biden/Powell approach will horribly backfire and generate out of control inflation. But there are no certainties in life. There’s a saying that if you’ve never missed a flight, you are spending too much time in airports. In response, I say that I enjoy spending time in airports, so I don’t mind. By the same token, if you are making policy choices that are guaranteed to avoid overheating, then you are going to spend too much time away from full employment. The conventional wisdom in economics feels the same way about that as I feel about airports.

But if I get to the airport early, I fill up my water bottle, plug in my laptop, put on my headphones, and do some work — it’s genuinely fine.

I think labor market slack is not fine, and that we ought to fight like hell to get back to 2019 economic conditions as soon as possible. Biden and Powell agree, and I’m glad they are in charge. And while I think there are various valid quibbles one could make with the structure and design of the ARP, it’s important to understand that a lot of criticism these days is coming from people who fundamentally don’t agree with that diagnosis and think it’d be fine to plunk along for years and years before we get back to a high-pressure economy.

It may not be prominent in the academic literature but I suspect one of the underrated aspects of full employment is the wellbeing benefits of being able to tell your boss to go f***k themselves if they’re being unreasonable.

If you're right Matt, and I believe you are, the small business lobby is going to be angry for a pretty long time. Right now, they are grasping at straws because of the bonus UI that runs out in a few weeks, but what do they blame after that?

The reality is that many if not most small business owners operate businesses that, most of the time, require almost no innovation, clever pricing strategy, or in many cases, even risk. Some are risky because the unit economics are on the margin (see: restaurants). But the common thread you get at here is that many small businesses have never had to *recruit* workers at all, and now they find themselves in a game they are entirely unprepared for, and they're mad.

Imagine going your entire business life under the idea that the best way to motivate your people is to "let the beatings continue until morale improves", then suddenly be in a full employment world where that particular management technique starts to fail spectacularly.

Maybe we should start new job training programs for these poor guys so they can learn how to make it in this new world of small business that requires effective implementation of a talent strategy?