The truth about the Biden economy

It's best not to exaggerate in either direction

Sorry for the later than usual email, folks. Thanks to an issue with Substack, the usual free preview didn’t make it to out this morning. So, you’re getting this as a bonus free article instead. Enjoy!

The American economy is in remarkably good shape, given the scale of the global economic disruptions during the Covid-19 pandemic and its aftermath.

That’s not just spin. If you compare the American economy to that of other rich countries, and you can see we are doing a lot better.

You can also compare the American economy in 2024 to the forecasts issued by the Congressional Budget Office in January of 2020. Real GDP — that’s with the inflation adjustment — is higher than they thought it would be. The biggest reason for that is that immigration has been higher than the CBO expected. But have those immigrants’ jobs come at the expense of Americans’ jobs? No. Before the pandemic, the CBO thought we would have a 4.4 percent unemployment rate this year and a 4.2 percent rate last year, and the actual numbers have been lower than that. They thought the prime-age labor force participation rate couldn’t break the 83 percent mark, but it has.

On the flip side, obviously inflation was greater than the CBO expected, and while inflation is now contained, that’s in part because interest rates are also higher than they thought they would be.

I think this is a good record, all things considered, because the pandemic did actually happen — production of certain things shut down for a while, patterns of consumption shifted around wildly, and all things considered you can’t address a problem like that at zero cost. And I’m glad that consumer sentiment popped a lot last week; it means the reality of the post-inflation economy is setting in. Last month, I scolded Debbie Downer Progressives who believe touting a glass half empty view of the economy will serve progressive causes, and I stand by that. But now that the mass public’s views are looking up, I do want to pull a slight hypocrisy and punch in the other direction.

When you do political messaging, you are trying to persuade swing voters, but in practice, your messages mostly persuade your own base. That’s just the way it works. So I think that as Democrats have talked up the Biden economy, they’ve talked their own elites into an excessively rosy picture of the situation.

That in turn is creating two distortions, one substantive and one political:

The substantive distortion is the overstated idea that Biden has forged some glorious new path in which we have shed the dogmas of neoliberal economics and will march forward into a brave new future of industrial policy.

The political distortion is the belief that if Biden loses, that loss will be totally unrelated to his objective domestic policy performance, and all of the lessons learned should be lessons about either the power of misinformation or else the perils of splitting your base over Israel.

The truth about the Biden economy is that it’s in remarkably good shape, given all that happened. But that’s not the same as saying that we are living through an unprecedented boom that the electorate is mysteriously failing to reward. Voters’ nostalgia for the economic conditions of the pre-pandemic era is perfectly reasonable.

The unreasonable part is believing that Donald Trump’s policies will bring it back.

The economy is fine

Something as complicated as “the economy” is hard to summarize, but if I had to pick one chart to summarize the recent economic evolution of the United States, I would take this one from Jason Furman that shows per person inflation-adjusted personal income.

The basic story here is that real personal income surged during the pandemic, because the government flushed out a ton of cash to households as stimulus, but people (on average) spent less money rather than more because they didn’t want to get sick. This created a weird situation where the government was able to enact massive stimulus without generating any inflation, because we were mostly pushing on a string — people simply refused to spend.

Then, as Covid faded, people started spending this money down.

You, as an individual, can spend more than you earn by drawing down savings you amassed during the pandemic. But global society cannot consume more than it produces, so when a bunch of people tried to simultaneously draw down savings, we got a big burst of inflation that pushed personal income into the negative. Inflation has settled down, and we’re now basically back on track. Note that even though we are still below forecast, this is not a case of Americans experiencing intense material deprivation. Consumption is way ahead of forecast, even when accounting for inflation.

If you imagine a hypothetical person who took office in 2018 and has been governing consistently since then (call this guy “Jerome Powell”), I think you’d say he did a pretty good, albeit imperfect, job of steering the ship of state through choppy waters. Certainly, I would say the managing of pandemic-related economic issues has been better than the management of the pandemic itself.

Did the powers that be spend too much on pandemic relief?

On one level, yes, that is the story of this chart. More money was spent than was strictly necessary. If you asked about this at the time, the architects of these relief policies made two points:

Correcting for a fiscal overshoot with higher interest rates is logistically easier than correcting for undershoot with more spending.

Because it’s impossible to target perfectly, you need to choose between giving some money to people who don’t really need it and leaving some people in desperate need without enough.

I would not defend literally every implementation detail of the CARES Act and the American Rescue Plan, but these are both reasonable points.

The flip side, though, is that if you act on these beliefs, the likely outcome is higher interest rates than one would ideally like to see. Which is what happened.

Democrats created an expanded Child Tax Credit in the ARP primarily because they hoped this would lay the groundwork for a permanent CTC expansion that reduced child poverty. This was a good goal and it almost worked. But, of course, it didn’t. If Democrats had known in advance that it wouldn’t work, they wouldn’t have done it, and both the interest rate and inflation situations would be better today. That said, the underlying issue of child poverty continues to be very important. I really recommend this recent Niskanen Center report on options for rebooting the CTC expansion, as well as Rep. Jared Golden’s thoughts on this.

The choice of a baseline

Note, though, that if I wanted to make Joe Biden look bad, I could make this chart showing that real personal disposable income has collapsed since the beginning of the Biden administration.

This is, in my opinion, a stupid way of looking at it. But it is true that people got a huge surge of stimulus payments right at the beginning of Biden’s term, and personal income has been lower than that ever since.

I mention this not because that’s the best way to look at things, but to illustrate that the choice of baseline makes a big difference.

When people try to make the case for Bidenomics, they tend to do what Brendan Duke does in his chart, showing the rising wealth in the bottom half of the income distribution — comparing the present day to the situation before the pandemic.

The reason to do it that way is so that the 2020-2021 swings in prices and stimulus payments cancel each other out. Methodologically, I think it’s completely defensible. And, again, since Jay Powell has been in office this whole time, it’s also a perfectly reasonable way to assess his tenure. But in terms of partisan politics, there’s a big difference between 2020 and 2021 — we switched presidents. If you measure from the pre-pandemic baseline rather than from the pre-Biden baseline, you get a much happier story.

The main thing I would say about this is that it’s dangerous for Democrats to get themselves confused about what their charts are saying.

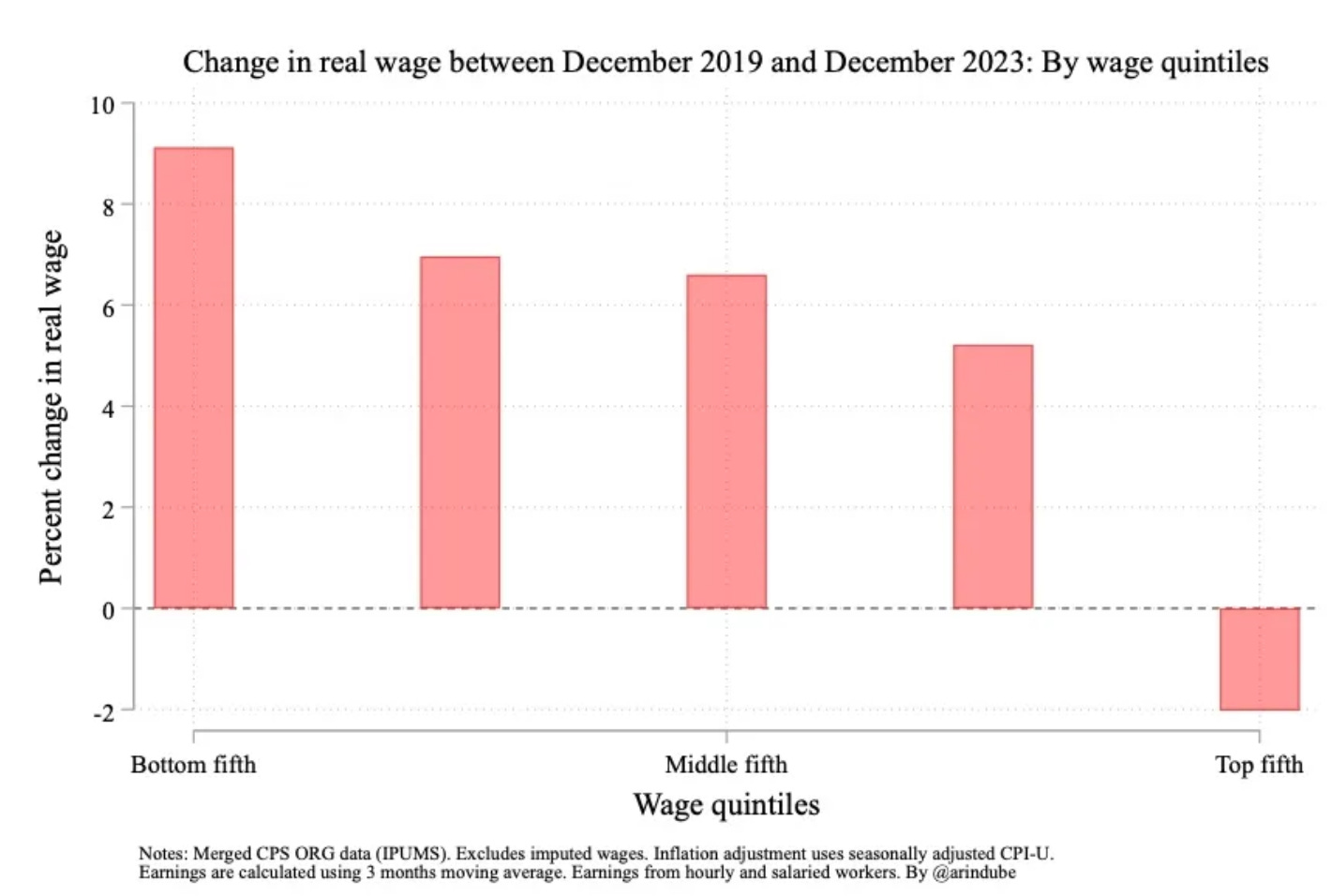

Arin Dube, the University of Massachusetts economist, is a really straight shooter who’s very interested in labor market dynamics and income inequality. So when he makes this point about aggressive fiscal stimulus leading to both wage growth and reduced inequality, he’s correctly measuring from a baseline of December 2019. And there’s nothing wrong with people interested in partisan politics using this chart to counter the Debbie Downers.

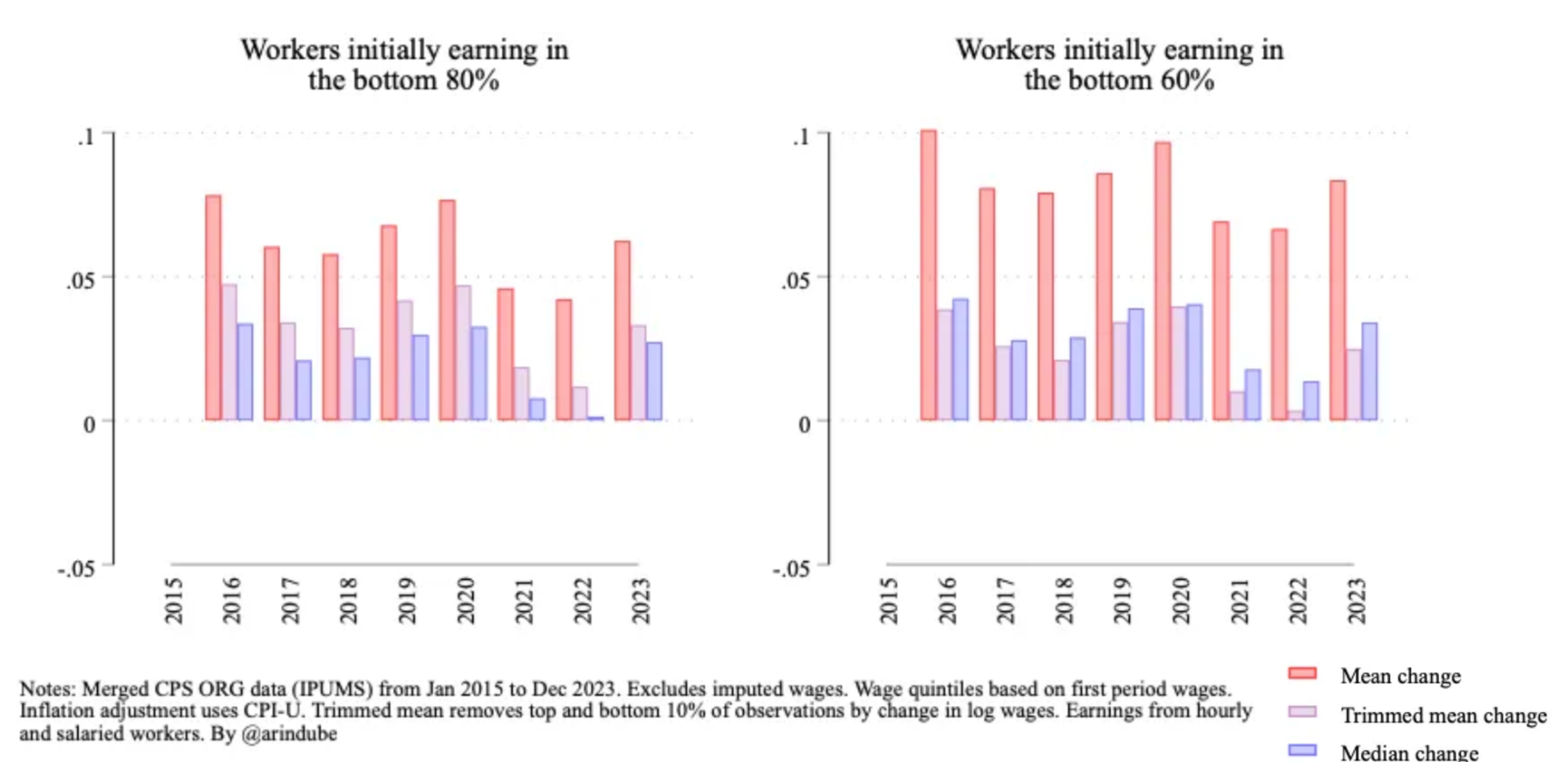

But if you’re looking at this chart and puzzled about why workers aren’t rewarding Joe Biden for broadly shared prosperity as much as you think they should, you need to keep in mind that Biden was inaugurated in 2021. Here’s a different chart from the same paper that has a more detailed temporal breakdown of what’s been happening. These charts clarify a few things:

Properly measured wage growth under Biden has been positive.

Biden’s first two years in office were really rough compared to both Trump’s term and Obama’s second term.

Wage growth in 2023 has been solid, but not necessarily more solid than it was in 2018 or 2019.

To be clear, I don’t take any of this to mean that Trumpstolgia is rational. The idea that Trump was good for the economy and Biden is bad involves a pretty fundamental cognitive error — you need to say that job losses of 2020 were an inevitable consequence of the pandemic that Trump should be held blameless for, but the inflation of 2021-2022 was all Joe Biden’s fault. That isn’t true, and it also isn’t true that Trump’s forward-looking policy ideas will improve any of the problems with the contemporary economy. For those reasons, I strongly support Democratic efforts to message people into a more optimistic read of the economic situation, and I’m glad consumer confidence is making a comeback. But I don’t want Democrats to message themselves into believing that they’re dealing with the greatest political puzzle of our time.

Biden is achieving his specific goals

Democrats have also made a lot of charts based on data showing a huge increase in spending on the manufacture of construction facilities. This is a real thing that is happening. But is it true that there is a “manufacturing boom” under Biden that voters haven’t noticed?

Not really. What’s happening is that overall business investment is exactly on track for pre-pandemic forecasts. This spending on manufacturing construction has been largely oriented around semiconductors, which have been a major policy focus of the Biden administration. We are also seeing investment related to the construction of batteries and electric cars. Carbon dioxide emissions are falling. If you listened to Republican Party criticisms of Democrats’ priorities, you would have expected all this work to crush business investment and destroy the economy. That hasn’t happened: Democrats are getting stuff done on their priorities, and overall investment is exactly on track for pre-pandemic forecasts — Democrats have shifted investment into their priority areas.

That’s a solid story for Biden, to the extent you view the strategic argument about semiconductors and the environmental argument about climate change as correct on the merits. It showed that these goals can be achieved at much less cost than Biden’s critics warned.

But it’s not a thrilling new economic paradigm that’s delivered unprecedented levels of prosperity. Biden’s economic policies have restored the solid labor market conditions we had before the pandemic, but with higher interest rates. The case in favor of those policies hinges on convincing people that Biden is right to care about steering investment into these priority areas.

And the case against Trump hinges on convincing people that he doesn’t have a solution on interest rates.

Trump doesn’t have a solution on interest rates

My bottom line about all of this is that if a person says to me “sure, the labor market is strong in 2024 but it was also strong in 2019 and we had lower interest rates back then so I want my Trump Economy back,” that’s fine.

But there’s a difference between looking back fondly on some elements of the past and actually having a plan to bring them back. I miss the days when I could stay out drinking until 2AM, then wake up and put in a solid day at work. But I have learned from bitter experience that even though hanging out with friends is still fun, forty-something Matt just can’t act like twenty-something Matt and expect twenty-something Matt outcomes.

By the same token, when Donald Trump took office in 2017, he did so at a time when the labor market had been growing steadily for years, a time when both inflation and interest rates had been low for years. What liberals had been saying for all those years was that the economy would benefit from fiscal stimulus. Trump took office and raised domestic spending, cut taxes, and raised military spending. And it worked out fine — job growth continued, low inflation continued, and while interest rates went up a little, that was a change from “freakishly low” to “still low.” And good for him. If I’d been president, I would have used that fiscal space to accomplish somewhat different things, but a big fiscal stimulus was the right idea for the conditions of 2017.

Right now, though, the whole premise of Trumpstalgia is that we want those low interest rates back. And nothing on the Trump policy agenda — not giant tax cuts, not defending single-family zoning, not deporting the agricultural workforce, not a 10 percent tax on all imports — is going to accomplish that, unless he has a secret plan to enact big short-term cuts in programs to support America’s seniors.

Because the issue here really is the pandemic.

That was a big negative shock to the economy. We navigated it pretty successfully and emerged with the strongest economy in the world. But there was a cost to all that, and the cost is a higher debt load and higher interest rates. Biden also successfully pursued some big investments in semiconductor manufacturing and green technology, while defying Republican forecasts that doing this would lead to some kind of economic cataclysm. But we’re not living through kind of staggering outburst of prosperity with huge benefits beyond the geopolitical and environmental impacts.