The truth about profits and inflation

Rising margins are why inflation is bad, not why it's happening

The American economy had a huge demand deficit in 2009 that was only partially filled in subsequent years. As a result of this inadequate demand, inflation and interest rates were persistently low, as was the share of working-age people who had jobs.

This vexing lack of employment had a lot of consequences. Non-working young men living with their parents tended to spend a lot of time playing video games. Employers grew quite reluctant to hire anyone who would need on-the-job training. Lots of people accepted low-paid gig work rather than a proper job. Many others with degrees “undermatched,” and took food service positions. Construction activity plummeted, and the people (mostly men) who used to swing hammers had to find jobs (mostly lower-paying) in other fields.

Because the consequences of this demand shortfall were so widespread, lots of little stories that got the direction of causation backwards started to sprout up.

Maybe video games and porn had become so good that people didn’t want to work anymore? Maybe there was a “skills gap,” and workers didn’t have the skills they needed to get jobs? Maybe we’d built too many houses before the crash, and now nobody would ever want to live in a house again? All of these micro-theories had a kind of limited validity. It’s true that for any given worker, if that specific worker had better skills and more intrinsic desire to work, he would be more likely to get a job. But even collectively, these microeconomic points couldn’t explain the phenomenon of overall low unemployment. Among young, inexperienced workers there are always people — half the people exactly, in fact — who are below-average in skills and motivation, and in a healthy economy, these people get jobs, too. In an unhealthy one, they don’t.

Some of the stories that people told were wrong, but plenty of them were right. It can be interesting and valid to explore micro-dynamics that help explain which people get jobs when jobs are scarce and who is particularly likely to suffer. But as a broad explanation of why jobs were scarce, these micro-stories fail. You need to bring macroeconomics into the picture: the government did not do an adequate job of stabilizing aggregate demand, which kept unemployment high.

More recently, the United States has been at full employment, with a decent amount of inflationary pressure added by high budget deficits and by the expectation that deficits will continue to be high. This has spawned articles exploring the micro-dynamics of how, exactly, companies go about raising prices. A lot of this is interesting. If you’ve ever been involved with a business in any way, you know that people don’t just sit around and say “aggregate demand is up, time to hike prices.” A lot of calculation and effort go into being clever about it. But a lot of the work that’s been done in this field, like this recent package of American Prospect articles on “How Pricing Really Works,” is mistaking a micro-scale exploration of pricing dynamics for a macro-scale explanation of why inflation happened.

The standard macroeconomic account

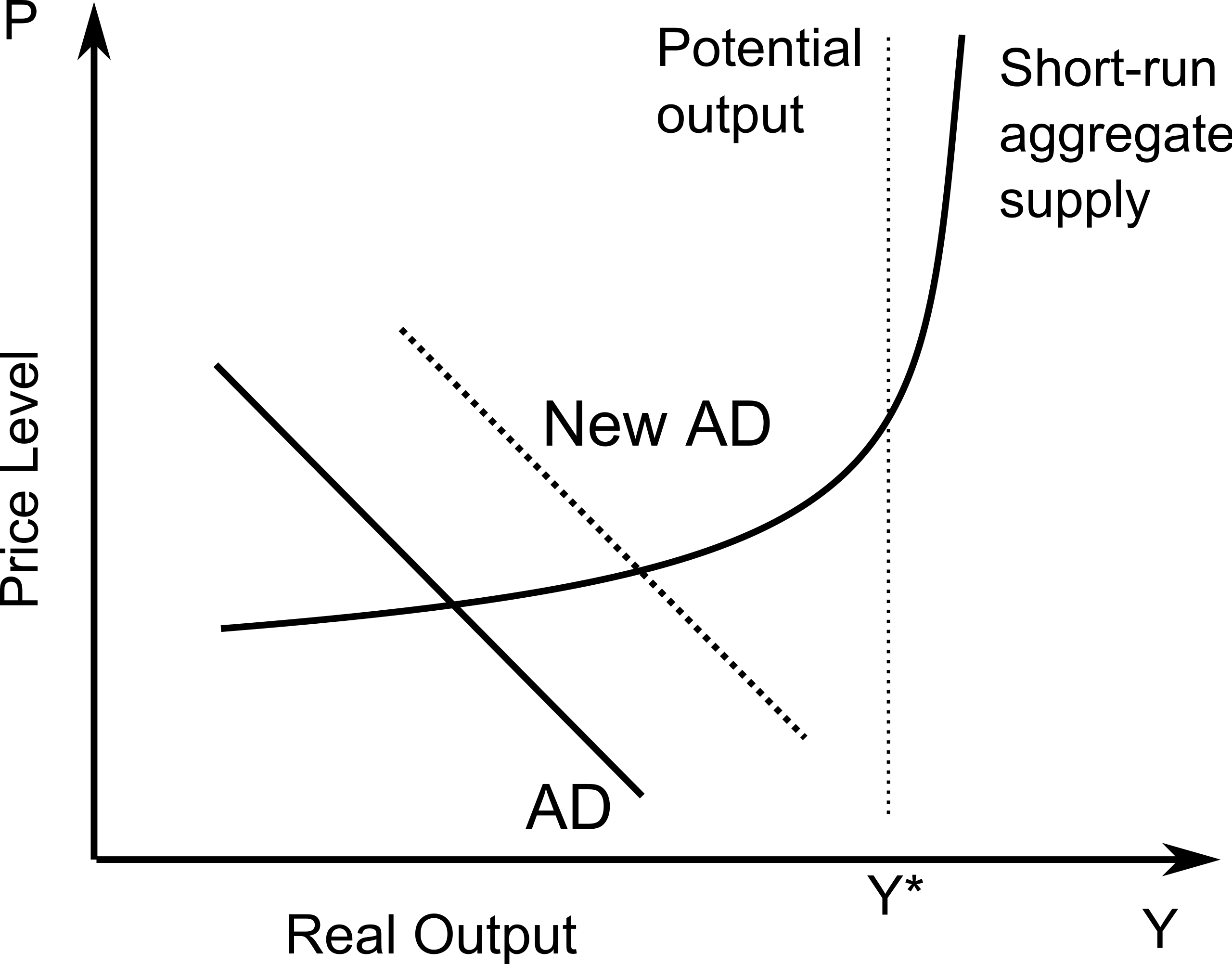

Here is a really simplistic Keynesian model of aggregate demand and aggregate supply, borrowed from Wikipedia.

It depicts an economy that is in a fairly depressed state — a recession — driven by inadequate aggregate demand. But then wise policymakers act to increase aggregate demand (by cutting interest rates or doing deficit spending) and AD shifts from the solid line to the dotted line.

That stimulus has two impacts. On the one hand, prices rise in response to the increase in demand, because some kinds of goods and services are in scarce supply even in a recession. But mostly what happens is that “real output” increases.

Thanks to the rise in demand, unemployed workers are put back to work. Factories run additional shifts. Vacant storefronts get occupied. Existing retailers maintain longer hours. Extra trucks roll off assembly lines and more deliveries get made. That’s why stimulating a depressed economy is good. Life is full of tradeoffs, but when you have tons of unemployed people, the opportunity for nearly-free lunch exists. So if a boost to demand leads to more real output, why not keep boosting demand higher and higher? Over time, you start running out of unemployed workers and idle factories and vacant storefronts. Or if you do have vacant property, it’s because remote work has dealt a structural blow to companies’ desire for office space, rather than because the economy is depressed per se. You start moving to steeper and steeper parts of the curve, where a larger and larger share of the marginal new dose of demand goes into higher prices rather than higher output. Eventually, the supply curve is vertical — or nearly vertical — and you’re just doing inflation.

This doesn’t make for a good magazine article.

Keep reading with a 7-day free trial

Subscribe to Slow Boring to keep reading this post and get 7 days of free access to the full post archives.