The triumph of capital

It’s been a great generation to have started out rich.

A handful of left-wing economists have made tortured efforts in recent years to redefine asset value appreciation as a form of income.

That’s because over the past 10 years, Mark Zuckerberg, among other billionaires, has amassed a staggering amount of wealth relative to the taxes he’s paid. But defining income to include this sort of appreciation means that you can say Zuckerberg pays a low tax rate.

The problem, to be slightly boring, is that this is not income.

If you compare the United States to the famously high-tax Nordic countries, the major difference is not in the top statutory income tax rates. The top American combined state and local tax rate is generally a little higher than it is in Norway and a little lower than in Denmark and Sweden. New York and California, where a large share of our billionaires live, have unusually high top income tax rates, so the richest people are paying Nordic-level marginal rates.

The big difference is that the Nordic top rates kick in at between 110 percent (Sweden) and 180 percent (Norway) of average income versus 880 percent of average income in the United States. Obviously if we lowered the threshold for the top income tax bracket down to the Norwegian level, that would generate a ton of extra revenue — including extra revenue from billionaires — and that could pay for all kinds of things.

But nobody in the United States wants to ask the middle class to pay more, so we keep seeing efforts to kind of redefine the billionaire situation to make it seem like they’re paying unusually low tax rates when they actually aren’t.

I find this whole situation pretty annoying.

But I also think conservative critics are putting their heads in the sand in terms of what’s really happening in the American economy to drive all this. Simply put, we’ve been living through a period in which the returns to being rich have grown astronomically faster than the returns to being a hard-working, gainfully employed normal person.

The stock market’s wild ride

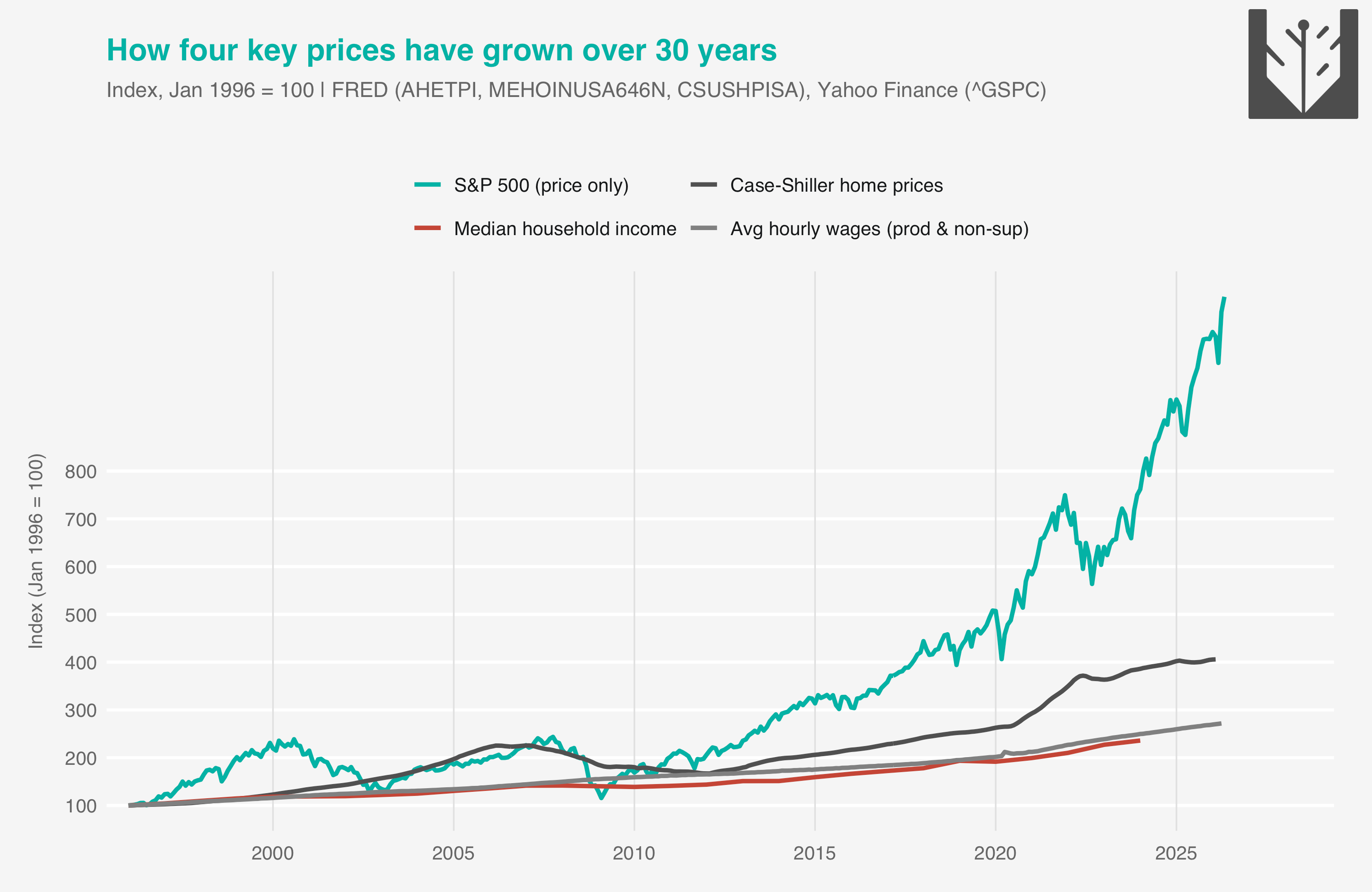

Check out the chart below tracking four major economic indicators over the past 30 years. You’ll see that from 1996 until around 2012, the stock market was much more volatile than median household income or average hourly wages for nonsupervisory workers, but these indicators actually ended up in about the same place. The Case-Shiller house price index diverged from the stock-market trajectory for a few years, but ended up in the same place.

But the years since 2012 have looked very different.

To be clear, even my chart is a bit too generous to working for a living. Stocks, in addition to appreciating in price over time, pay dividends. And a house isn’t just a financial asset; if you own one you can live in it rather than paying rent to someone else. Or alternatively, you can rent it out and make money. But still, there’s a world of difference between that 1996–2012 trajectory and what we’ve seen in more recent years where housing prices have risen faster than incomes and stock prices have soared astronomically.

Imagine someone who inherited $1 million in an S&P 500 index fund at the start of 2012 and never sold the shares or reinvested the dividends.

He’d have about $6 million in his portfolio today and would have scored about $40,000 per year in dividend income. You could imagine two people with decently paid white-collar jobs, one who’s upwardly mobile from an immigrant family and another who inherited the million bucks from his grandparents. If the heir was prudent with his windfall, he and the non-heir have experienced increasingly divergent economic fates over the past 14 years.

Before conservatives pop in to yell at me, let me flag that I am well aware there is a reasonable policy argument that it’s good and appropriate for tax policy to encourage this kind of prudence.

If you taxed the heir’s inheritance, that would have encouraged his grandparents to increase their consumption and pass on a smaller nest egg. If you taxed his unrealized capital gains, that would encourage him to sell more shares and increase his consumption. A classic tax-policy idea is that this is bad and we should encourage high rates of saving to grow the capital stock and ultimately increase wages.

I’m just saying that if you want to understand the vibes in American society, you need to look at that chart, because it’s kind of crazy.

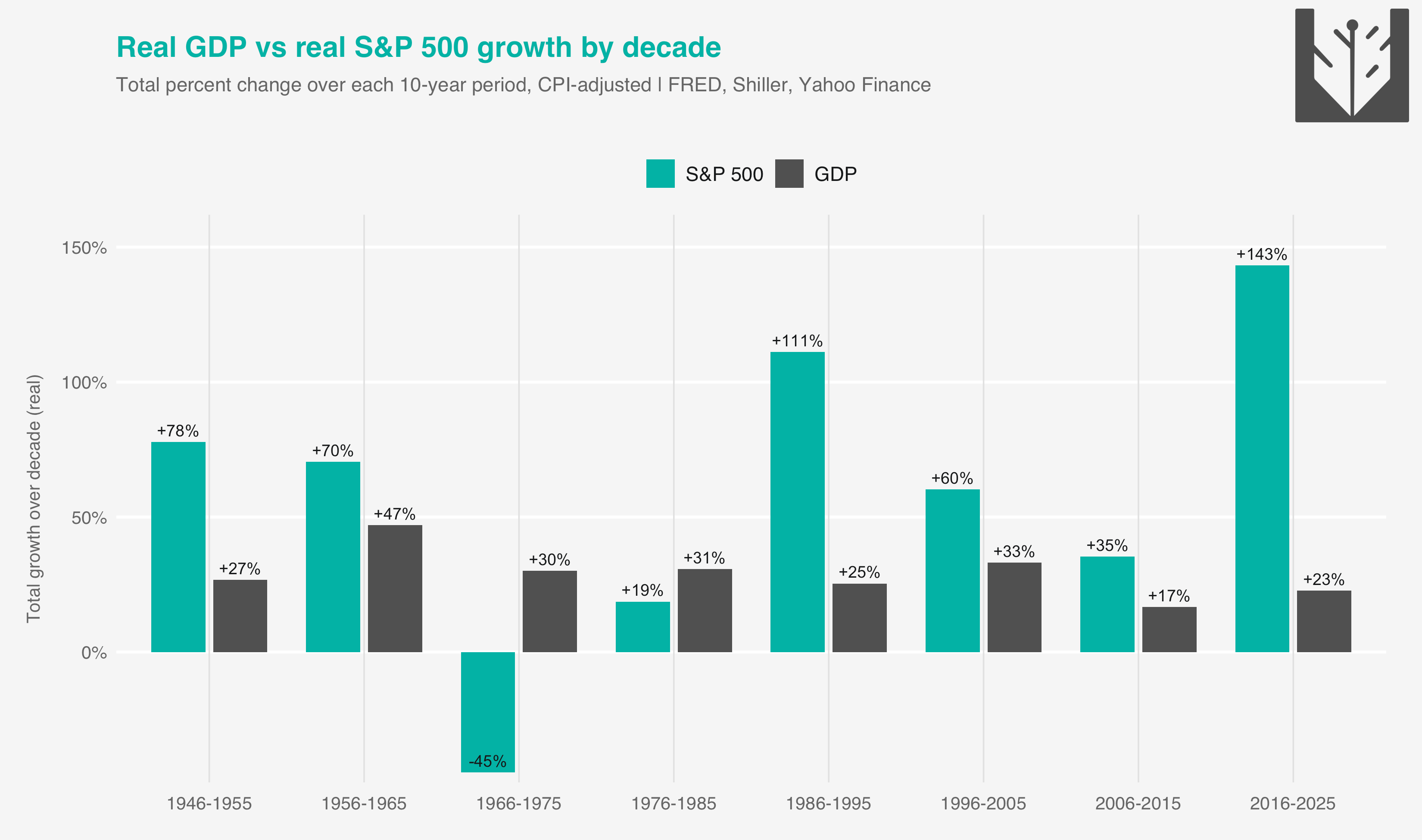

And you should also note that this is not a historical inevitability. There are long stretches of time when the stock market grew more slowly than the economy. But from 1986–2015 it grew faster. And then for the past 10 years the gap became dramatically larger than at any earlier time in history.

If you are one of the six people who actually read Thomas Piketty’s “Capital in the Twenty-First Century,” then you’ll know that the primary concern he raises in the book is specifically about this heir question. He’s worried that a tendency of the value of financial assets to grow relative to the size of the overall economy will lead to a new aristocracy of inherited stock-market wealth. This is in fact not what happened, because a whole new cohort of even richer people arose.

The rich get richer and others get even richer

If you look at the very richest people in America — Elon Musk, Larry Page, Sergey Brin, Jeff Bezos, Larry Ellison, Michael Dell, Mark Zuckerberg, Jensen Huang, Steve Ballmer, and Jim Walton — nine of them are basically self-made, with a Walton heir in 10th place. So we’re not really living in the world that Piketty warned about with an aristocracy of inherited wealth.

But we’re also not not living in that world.

Back in the 2011 Forbes 400 list, Jim Walton had $21.1 billion and he’s now closer to $144 billion according to the Bloomberg Billionaires Index. That’s a very large increase in net worth. And he’s not the only Walton heir out there: Rob Walton is listed at $141 billion, Alice Walton at $140 billion, and Lukas Walton (a grandson of the Walmart founder) comes in at $49.7 billion. Christy Walton has $23 billion. Notably, the Bloomberg list says that Lukas’s net worth has grown by about $2.6 billion this year.

If you started a company in January and it was worth $750 million today, I think most people would say you were incredibly successful. But that pales in comparison to Lukas Walton’s business success doing basically nothing.

Which is just to say that the billionaire entrenchment dynamic Piketty was worried about has, in fact, happened. The error he made was not realizing how open the field would be for a relatively small number of successful founders and financiers to amass newly minted fortunes that are even larger.

This was a pretty big analytic error on his part — and awfully French in its way to just kind of assume there wouldn’t be huge new fortunes. Still, I wouldn’t underestimate heirs! I don’t think anyone needs to wander the streets feeling sorry for Brian Chesky or Marc Benioff or Reid Hoffman or Reed Hastings or the Collison brothers. But it is true that all these successful and prominent founders have significantly lower net worths than various Walton and Mars family heirs.

Two things can be true

I have some takes on what this all might mean and what the implications for policy and society might be.

But mainly I think the basic descriptive facts are underrated:

The U.S. economy remains very open, and talented individuals can, with a mix of hard work and some luck, achieve incredible success.

For a normal person who is not going to found a high-growth start-up, the best route to affluence in recent years is to have started with a modicum of affluence and then just watched your portfolio compound.

To return to the tedium of tax policy, there is a lot of good theory that says that a rising capital stock is ultimately good for everyone, and you basically want to encourage these trends. A rising stock market is good. Founding new successful companies is good. Rich people having high savings rates is good. It’s all going great.

But it does mean you’re looking at a widening wedge between people with significant asset portfolios and those without.

And while the newly minted entrepreneurial billionaires do undercut the specter of an aristocracy of inherited wealth, they don’t fundamentally change the dynamic in which, among the population of normie non-founders, the logic of compound growth in asset prices is racing ahead of working for a living.

Something I'm curious what you think about, that seems like it would have been included here is the strategy of borrowing against your assets to keep your tax bill down and not having to pay for it as a realized capital gain. I'm not a tax wonk but every time I hear about this approach It feels like a big unfairness in the tax code that punishes high income w2 folks and allows the top earners to really avoid full taxation of their assets.

I don't think it is coincidence that this growth in asset prices aligns with massive government deficits. As best I can tell, when the government pushes a dollar into the system, it circulates amongst people who NEED to spend until eventually it reaches people wealthy enough to save that dollar. At which point they usually add it to the giant pile of money sitting in the capital markets.

For all the old talk of "trickle down" economics, as best I can tell the mechanism is much more "trickle up" with a few cents of profit getting skimmed off every transaction and sequestered in financial assets.