The pandemic is still upending the economy in surprising ways

Remote work created a housing boom which has depressed labor force participation

Lane Brown wrote an article for Curbed asking a good question: how can rents be up in a city like New York if the population still hasn’t fully recovered to its pre-pandemic level?

Unfortunately, the answer the piece suggests is that it’s a conspiracy whereby landlords are somehow colluding to keep units off the market in order to drive up rents. There’s no evidence for this, it’s extremely hard to see how landlords could possibly pull it off, and it’s somewhat hard to square with the fact that the same basic trend is visible everywhere.

And it’s too bad, because in macro-political terms, I do think it’s good for leftists to appreciate that one way for property owners to enrich themselves is to collude to restrict the supply of housing. They can’t really do this in the way that Brown suggests, but they of course can directly access the political system to impose zoning and other land use restrictions that curb supply. This doesn’t particularly explain New York City price trends over the past two years. But looking at the past 20 or 50 years, it’s absolutely true that property owners colluding to block supply is central to the story. They just do it by blocking new construction, not by warehousing existing units.

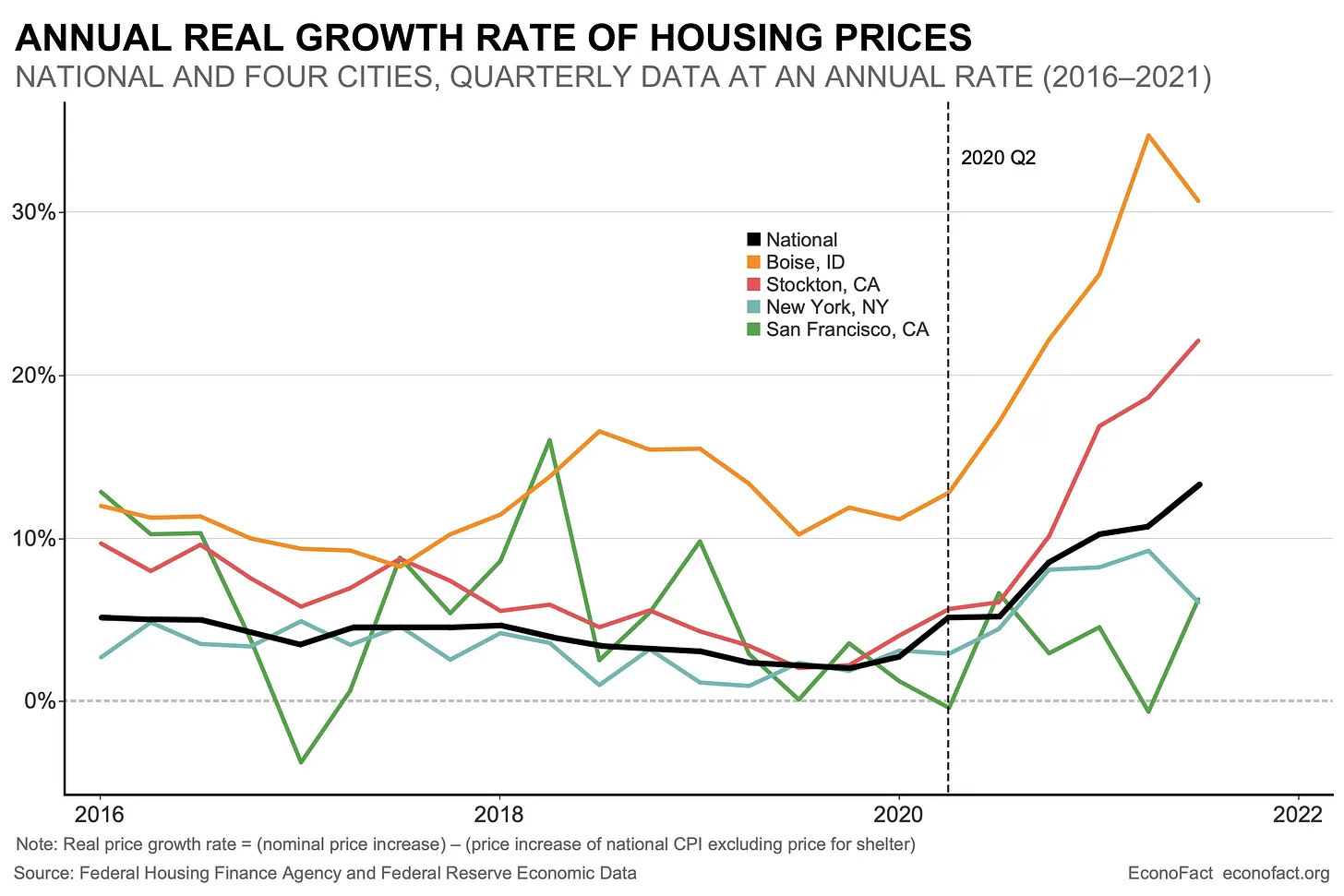

But what explains the short-term trend? How can demand be up even if the quantity of people is down?

I think this actually has a pretty straightforward explanation: population and relative rents are down in places like New York and San Francisco because of remote work. Absolute rents are up everywhere, and that’s also because of remote work. Thanks to remote work, fewer people want to live with roommates, more people want spare rooms to use as home offices, and many people have benefitted from a mix of rising wages and diminished commuting costs, allowing them to afford more square feet per person.

There’s reason to believe that remote work will have significant long-term benefits, but the very sudden shift in commuting patterns has happened much more quickly than the building stock can adjust. And a lot of other phenomena are downstream of that. Homelessness has risen in many places, for example, because your home office has displaced someone poorer than you from a bedroom.

And it’s even impacting the labor market. This increase in housing demand has meant rising costs for renters, but older people with lots of home equity scored a financial windfall as home prices boomed. What do older people do when they reap an unexpected asset price windfall? Well, some of them retire earlier than they otherwise would have. And Jack Favilukis and Gen Li calculate that this accounts for all of the post-pandemic decline in older workers’ labor force participation. It’s not that people have re-evaluated the meaning and purpose of life or that their work ethic has collapsed. It’s not fear of Covid. It’s that remote work boosted white collar workers’ desired level of housing consumption faster than the construction industry could add housing, creating a windfall for incumbent homeowners who then chose to take the windfall in the form of earlier retirement.

The wealth effect

The basic idea is pretty easy to understand. If I found a duffel bag full of money in a forgotten closet, I might splurge on something or save it for a rainy day.

But suppose you’re a 65-year-old regional manager who was planning to retire in 18 months when you become eligible to claim your full Social Security benefits. Well, if you get a cash windfall that’s plenty to live on for those 18 months, you might just say fuck it and retire a bit early. Why not? You’ve worked hard your whole life, your job is not particularly glamorous, and you don’t like dealing with annoying Zoomers at work.

I’m a little annoyed by the Favilukis and Li paper’s title, “The Great Resignation Was Caused by the COVID-19 Housing Boom,” because the Great Resignation was a dumb meme. To the extent that it refers to anything real, I think we should see it as referring to the pandemic-era boom in quitting one job in order to take another. That’s a real thing that happened; it’s the means by which higher labor demand translates into higher wages in an economy when few workers have a labor union that can negotiate raises in a less chaotic way.

What they are looking at instead is the rise in early retirements.

Beyond the title, though, it’s a good paper, and it shows a few different things:

From 2011-2021, higher price growth leads to lower labor force participation for older homeowners.

Higher house price growth has very little impact on the labor supply of younger homeowners.

Higher house price growth has very little impact on the labor supply of older renters.

The conclusion is that, in general, older homeowners use home equity windfalls to enter early retirement or semi-retire.

They then exploit the fact that the house price boom hit different metro areas differently, more muted in New York than in Boise for example, to create a counterfactual scenario of how age-specific labor force participation would have evolved if 2020 and 2021 home price trends had been the same as they were in 2019. The big difference is this thin pink line rather than the thick red one — showing we would have had substantially more old homeowners in the workforce without the home price boom.

Note that the big changes here are among people who are older. But this is important. As Lydia DePillis and others have written, the post-pandemic decline in labor force participation is overwhelmingly a story about older people. I’ve become enough of a cranky old person to be entertained by Adrian Wooldridge’s musings on legal marijuana and work ethic but statistically, the story about seniors retiring thanks to a wealth boost is a much bigger deal.

Sudden change is hard on the economy

The economics of the Covid era keep surprising us.

Keep reading with a 7-day free trial

Subscribe to Slow Boring to keep reading this post and get 7 days of free access to the full post archives.