Seniors aren’t living on “fixed incomes”

It’s not 1967 anymore — the world has changed.

Talk about senior citizens living on “fixed incomes” is such a cliché at this point that when Mark Kelly’s team put this tweet together, I’m sure they didn’t think twice.

But while this association between being elderly and being on a “fixed income” describes an extremely real aspect of American life between 1946 and 1975, it has little applicability to the present day.

Today’s senior citizens have, on average, some of the least “fixed” incomes of anyone out there.

I don’t particularly need Senator Kelly to pass a special bailout for Substack writers, but my business genuinely struggles with overall price inflation.

Slow Boring’s annual price hasn’t risen since I launched in 2020. But that initial $80/year subscription would be $102 in today’s prices. Yet because we all know that people care about nominal prices and not just real ones, if I suddenly hiked prices, that would almost certainly hurt me with subscription renewals.

The good news is that our subscriber base has steadily grown over time, so real revenue has always gone up, even during the really bad inflation years.

But especially because people selling digital subscriptions — whether that’s me, the New York Times, Netflix, or anyone else — can’t exactly say that we were forced by rising costs to raise prices, it’s just objectively the case that it’s easier to run our businesses when the inflation rate is low and harder when it’s high.

My personal economic situation is unusual, but this is a general fact about the world.

It’s probably easier to talk your boss into giving you a raise if inflation is at 8 percent than if it’s at 1 percent. But the fact is, you still have to exert effort to bargain for that raise.

There’s good research on this from Joao Guerreiro, Jonathon Hazell, Chen Lian, and Christina Patterson. Naive economists say that 0 percent inflation and 0 percent nominal wage growth is the same as 5 percent inflation and 5 percent nominal wage growth. But that wage growth doesn’t happen automatically — you need to fight for it, and the fighting is itself costly. A lot of the wage growth in 2022 and 2023 came from people switching jobs to get a raise, which is better than not getting a raise. But again, having to switch jobs requires effort and makes people inflation-averse.

You know who doesn’t have these problems? Senior citizens!

Fixed income in ye olde days

Go back in time to the post-war generation, though, and three things were different:

Social Security benefits were adjusted for inflation on an ad hoc basis by Congress on a very unpredictable schedule.

A much larger share of private-sector workers were in labor unions that had negotiated automatic cost-of-living adjustments into their contracts.

It was unusual for middle-class people to own stock.

Under these conditions, worrying specifically about senior citizens on fixed incomes made a lot of sense. Their Social Security benefits were specified in nominal terms. A very large fraction of their private savings would have been old war bonds specified in nominal terms. And in contrast to those senior citizens on their fixed incomes, not only did lots of union workers have cost-of-living-adjustment clauses in their contracts, but plenty of large non-union employers copied this to help keep their workers happy and their workplaces union-free.

In this specific context, senior citizens were, in fact, particularly vulnerable to inflation due to a high likelihood of living on a fixed income.

You could imagine George Meany meeting with some government officials in the late 1960s or early 1970s and pushing them to keep a laser focus on full employment despite rising inflation. And you could imagine someone from the government pushing back and asking, “That’s fine for your members, but what about retirees living on fixed incomes?”

I’ve been working my way through Agatha Christie’s Hercule Poirot mysteries and now that I’ve gotten to the postwar years this seems like a big issue in English society, too. There are retirees and war widows living off nominally fixed pensions or bonds, and dismantling the whole apparatus of rationing and price controls would be bad for them even if it would ultimately be economically beneficial to the country.

Crucially, though, today’s private-sector workers are dramatically less likely to have automatic inflation adjustments and only an idiosyncratic senior citizen would have their income entirely tied up in bonds.

The way we live now

Right now, about a quarter of seniors say they rely on Social Security for basically all their income. These are relatively low-income seniors and it makes sense to worry about their financial well-being. But since 1975, Social Security benefits have an annual automatic inflation adjustment. So while it’s reasonable to worry about retirees at the bottom of the income distribution, they are not living on “fixed incomes” at all and are not specifically burdened by inflation.

In fact, it’s just the opposite: Unlike working-age people, who even in a climate of rising wages need to exert effort to get their pay boosted to compensate for inflation, low-income retirees are automatically protected from inflation.

What about rich retirees? Well, rich retirees own shares of stock. The stock market has done extremely well in recent years, easily compensating anyone with significant investments for rising prices.

What’s more, while stock prices are not automatically inflation-adjusted, they are in practice pretty protected. That’s because the overall trajectory of the stock market is dominated by the actions of professional investors and algorithmic traders, and these investors are not particularly prone to money illusion. Inflation gets priced in rapidly, and a person with a healthy 401(k) account doesn’t need to do anything to secure inflation compensation.

Of course, people also invest in bonds, and it’s true that if you buy a long-term bond for the interest income and then inflation rises, you take it on the chin.

This is a thing that happens. But to be living on a fixed income, you need to imagine a senior who is affluent enough that Social Security does not dominate their income, but whose affluence consists overwhelmingly of bonds rather than stocks. Are there people like this? I’m sure that there are. But it’s not a large share of senior citizens, and it’s not a particularly economically vulnerable set of senior citizens.

This is much, much, much less common and socially significant than the banal case of a young worker with a nominally determined salary for whom inflation means either declining real income or a series of annoying conflicts with his boss to get a raise.

Focus on real problems

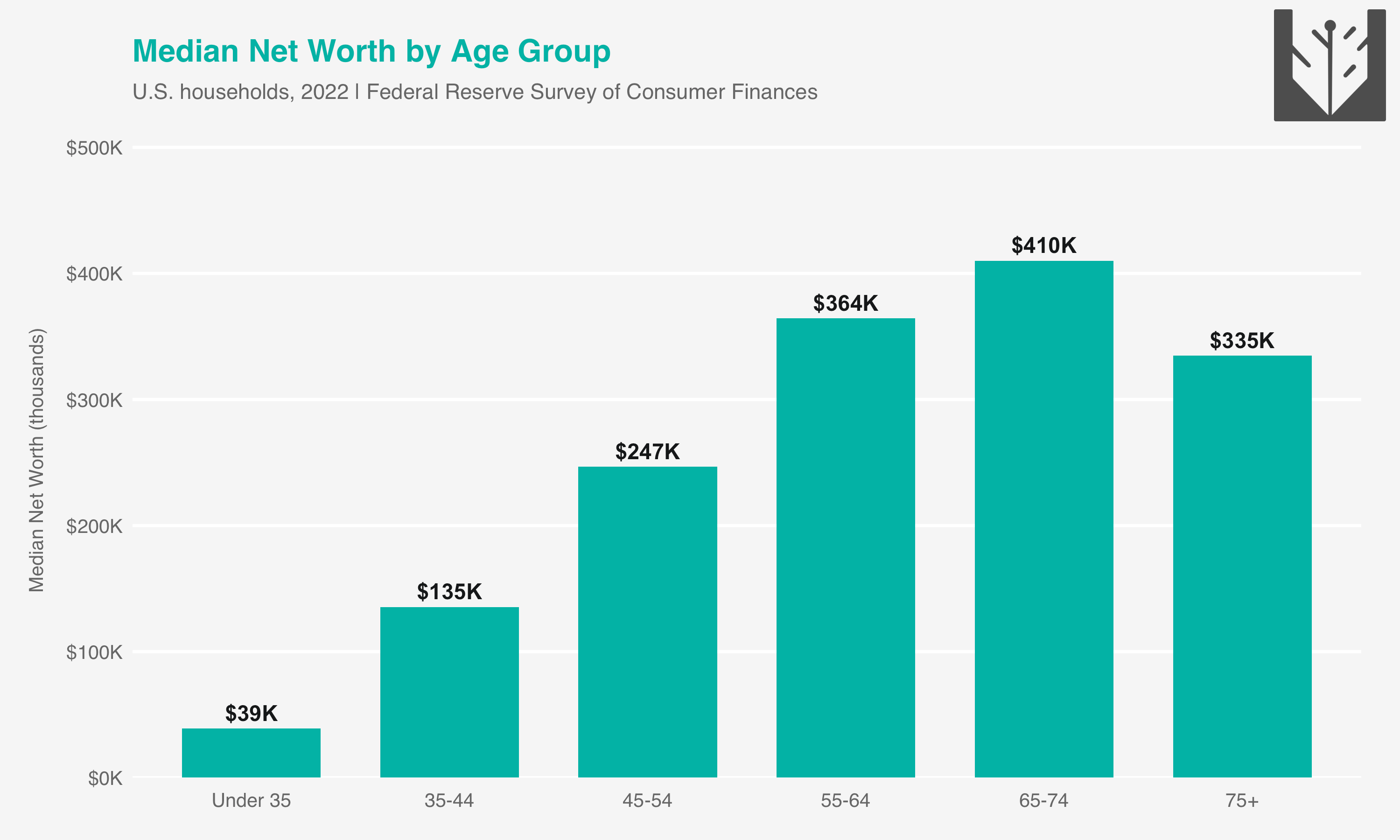

I’m not just trying to nitpick here. It’s important to understand that the elderly are quite a bit wealthier than younger people as measured by median net worth. Elderly Americans are less likely to say that they’re having trouble paying utility bills, skipping meals or missing health appointments to save money, or dealing with pest infestations in their home or crime in their neighborhood.

That’s not bad; it reflects a lifetime of savings plus a generally rising stock market. And it’s a reminder that we don’t need to go out of our way to worry about the economic problems of the old rather than the young.

And to that end, I think it’s helpful to stop repeating outdated clichés about who is and is not on a fixed income. Low-income seniors are protected from inflation by Social Security, which is much better than the pre-1975 design of the program. Affluent seniors are affluent.

Right now, 28 percent of America’s large homes with 3+ bedrooms are owned by empty-nesters. I’m not a communist who thinks we should seize those homes and redistribute them to young zoomer couples who want to get married and have kids.

But if affluent boomers were to sell their homes, realize large capital gains on the transaction, and move into smaller dwellings and live off their financial windfall, that would be a fine outcome for the country. When Senator Kelly says that Washington doesn’t talk about the problems of retired people enough, he has the actual situation completely backwards.

I think the confusion stems from people believing (me until this morning) that fixed income meant you relied on income from a source which paid a defined amount (social security, pension), rather than on income you controlled, like wages (work more to earn more) or drawing down investments/individual retirement accounts (you choose how much to withdraw). I legit did not know old school fixed income was income fixed in nominal terms, and I suspect most people (including those on social security and other retirement programs with automatic CoL adjustments) don't either!

Seniors living on a fixed income is the same as millennials "living paycheck to paycheck": The number of people actually in that economic condition is dwarfed by the number of people who have placed themselves into that category based on vibes,