It's time to raise taxes on the rich

Get it together, Democrats!

The number one issue in the country is inflation, so Democrats ought to try to enact policies that reduce inflation. On a political level, it would help them a little bit to be seen as trying to reduce inflation (rather than seen as primarily arguing about library books), and it would help them even more if inflation actually went down. But it’s also the case that, substantively, inflation is a big problem in people’s lives and one ought to try to do something about it.

What should Democrats do exactly?

Well, you can imagine a lot of things being helpful. At a time when the Federal Reserve is trying to constrain demand, it’s very good to have positive supply-side reforms that can power growth forward. But it’s also good to have fiscal policy rowing in the same direction as monetary policy, meaning — in this instance — deficit reduction rather than stimulus.

And here’s where the current state of things is driving me insane. Bill Clinton’s administration reduced the deficit by taxing the rich and reducing spending. Barack Obama’s administration tried to do a deal like that (“grand bargain”) but was mostly stymied by Republicans, so they ended up settling for the “fiscal cliff” where they basically just taxed the rich to reduce the deficit.

By the time Joe Biden won in 2020, Democrats were tired of being the green eyeshades party; they wanted to tax the rich and then spend all of the revenue on new programs. That’s where I was in November 2020 as well. But since that time:

Congress passed a lame-duck stimulus bill.

Jon Ossoff and Raphael Warnock were elected to the Senate, and Congress passed another stimulus bill: the American Rescue Plan.

On a bipartisan basis, Congress passed the Infrastructure Investment and Jobs Act that is largely “paid for” with smoke and mirrors.

Inflation became a huge national problem.

When the facts changed, I changed my mind. That’s what Democrats did when they largely stopped caring about deficit reduction during the 2012-2020 period (read Jason Furman, the then-top economic advisor to the Obama administration, explaining in 2016 how their thinking on fiscal policy had evolved). But the facts have changed again, so Democrats’ position ought to change, too. They ought to do exactly what Democrats have done in the past: raise taxes on the rich to reduce the budget deficit.

Some of the White House’s messaging on economics has made this pivot, which is great. But Democrats will have concurrent majorities in Congress for the next few months and also standing reconciliation instructions. And I don’t see them currently making any efforts to seal the deal between Joe Manchin, Kyrsten Sinema, and congressional leadership on a reconciliation bill.

And that’s insane! They should do something — something that would address inflation and restore the core class dynamic to American politics, something that would open up the possibility of building up the policy legacy of the 117th Congress at least a little bit.

They should raise taxes on the rich.

Austerity is needed

The global economy is a very complicated machine and a lot of unusual things are happening right now. Dislocations related to the Covid-19 pandemic are still clearly impacting the economy in many ways, and Russia’s invasion of Ukraine and the counter-sanctioning of Russia by the western coalition struck another set of blows to the supply-side of the economy. With Xi Jinping caught between his country’s low rate of vaccination with inferior vaccines and the extreme transmissibility of current variants of the virus, China appears to be flailing in ways that may make the economic situation considerably worse in the near future.

Based on the way the Fed has traditionally done monetary policy, it is very important to ascertain exactly why inflation is happening.

If the cause is excess demand, the right response is to raise interest rates and slow down demand. But if it’s a supply-side shock — like a Ukrainian wheat crop can’t be shipped to Egypt via the Black Sea because of a Russian blockade — then monetary policy is supposed to “look through” that shock and ignore it. Ben Bernanke made a fair number of policy mistakes during his turn as Federal Reserve chair, but he’s always done excellent work on this looking-through issue, and this piece he wrote for Brookings in 2017 is a great introduction to it.

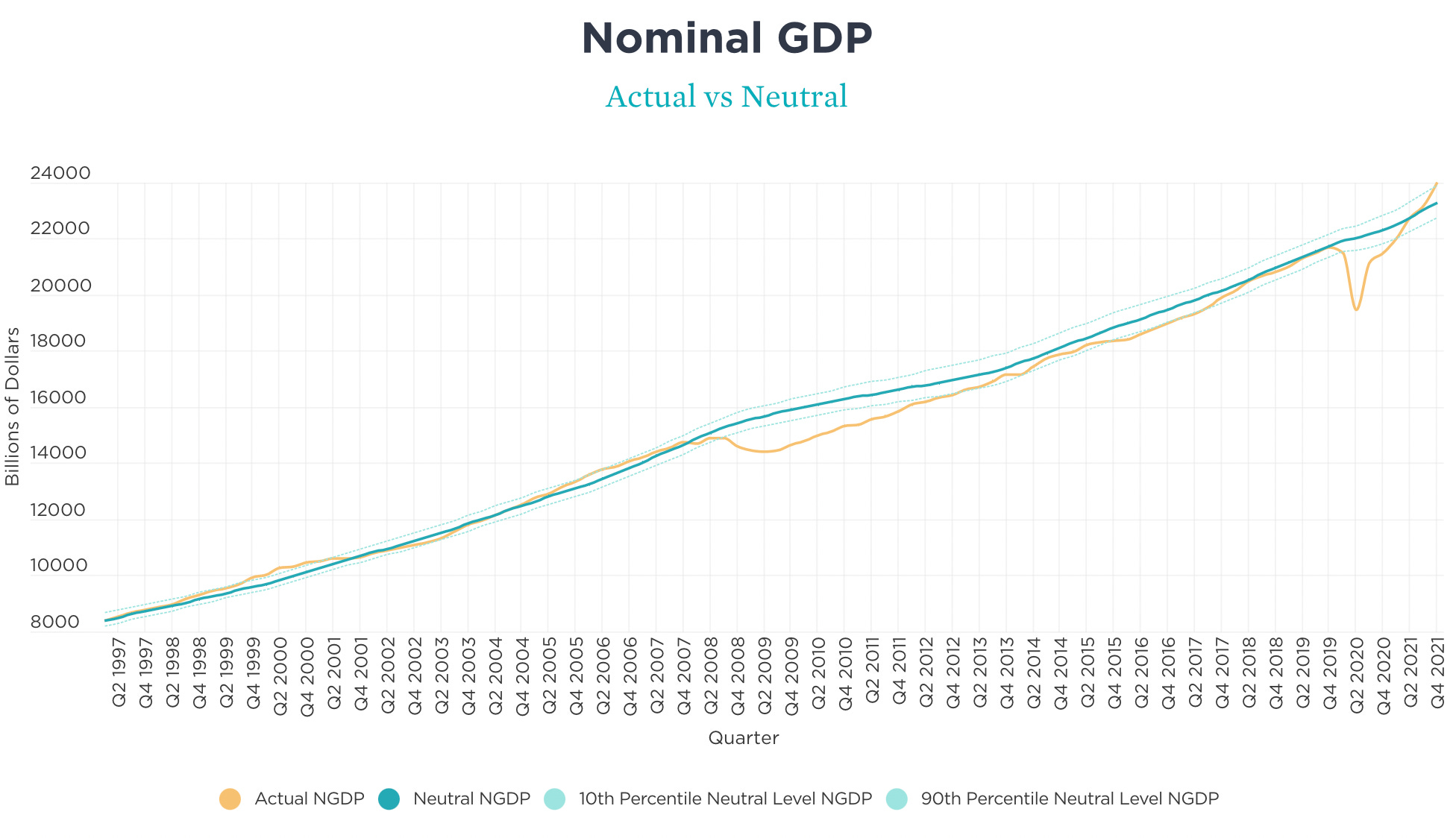

The perceived importance of the looking-through question is why economic commentators keep arguing about the relative impact of different supply shocks vs. the American Rescue Plan and other factors. But the persistent focus on this question has spun some people into the view that the presence of supply shocks means categorically that there’s no need to slow demand. And that’s wrong. If you ignore all the details and just look at economy-wide aggregate spending, you’ll see that after crashing during the shutdown, we’ve had a very rapid spending recovery. By the second quarter of 2021, we had caught up with the pre-pandemic trend. Then in the second half of 2021, economy-wide spending zipped up way above where you would have forecasted based on pre-pandemic trends.

With that much spending, you’re sure to get inflation.

This is not the only problem in the economy by any means. I think it’s probably the case that food and energy prices are a much bigger deal than this economy-wide inflation, and that’s why many people are feeling angry right now. And the high food and fuel prices are exacerbated by a lot of factors not explained in this chart.

But the excess of demand is real, it’s worth addressing, and it’s better to address it partially through fiscal policy rather than exclusively with higher rates.

Taxing the rich is a good option

Using monetary policy to raise interest rates is a classic approach and a necessary part of America’s strategy for slowing demand growth.

Unfortunately, there is a slightly paradoxical aspect to it because higher interest rates raise the cost of investments — such as in building new homes or converting suburban office parks to new uses for the Zoom era. And in principle, we’d like to see investment-led economic growth to raise our overall production capacity and make supply challenges less challenging.

Another option is to constrain consumption to get people to buy less stuff.

The problem there is that you are addressing the material hardship of inflation by inflicting more material hardship on people. What you want to do is target the hardship on people able to bear it. The pause on student loan repayments, for example, mostly benefits people in the top third of the income distribution. If you resume student loan repayments, that would suck demand out of the economy, and it would mostly do so by restraining the consumption of the affluent. But of course even though most student loan debt is held by affluent people, some of it is not. So the smart strategy in this case might be to end the pause while also doing means-tested cancellation so people in the bottom half of the distribution get permanent relief while those in the top half pay their fair share to combat inflation.

But the student loan situation is a weird quirk of our current circumstances. The main way that politicians allocate financial burdens to those who are most able to pay is through progressive taxation. Thanks to the Republicans’ Tax Cuts and Jobs Act, the overall tax burden in the United States got lower and less progressive. An extremely obvious thing for Democrats to do in today’s inflation circumstances would be to respond by making the tax burden higher and more progressive — to tax the rich.

Get this party restarted

I don’t particularly want to waste too much time revisiting the question of what went wrong with the Build Back Better proposal. But I do want to suggest that a lot of folks have been too eager to conclude from its collapse that Joe Manchin was acting in “bad faith” and/or “never wanted to do anything.”

I’ve always found that implausible simply because there’s no real reason for Manchin to misrepresent himself.

You could imagine a world where, I dunno, Sheldon Whitehouse secretly wants to sabotage the Biden agenda but also doesn’t want to be seen publicly as doing that because he’s worried about a primary. If that were the case, Whitehouse might engage in some elaborate deception where he’s misrepresenting his true views. But as best I can tell, this is the sequence of events with BBB:

Back in June of 2021, Manchin tells Schumer that he’s willing to embrace up to $1.5 trillion in new spending if it is fully paid for and if any revenue over and above $1.5 trillion is dedicated to deficit reduction.

Schumer kept that quiet, and leadership moved forward instead with reconciliation instructions calling for $3.5 trillion in new spending.

The wrangling with Kyrsten Sinema reached an agreement on something like $1.7 trillion in potential revenue.

Rather than try to edit the spending proposals down to the $1.7 trillion she had revenue for or the $1.5 trillion that Schumer had (secretly!) agreed with Manchin on, Nancy Pelosi moved a bill that used phase-out gimmicks to try to generate a $1.7 trillion score for what was really intended to be $3.5 trillion worth of new programs.

Manchin called foul on this, which seemed to set the stage for detailed negotiations to craft a proposal that would actually fit the criteria Manchin outlined to Schumer back in June.

Instead, Democratic leaders pressed pause on the process and pivoted to an unrelated effort to pressure Manchin and Sinema to eliminate the filibuster in order to pass a political reform bill that left most of the threats to American democracy unaddressed. This never had any chance of succeeding, but it did lead to lots of liberals who didn’t understand the details of the issue yelling at Manchin on Twitter and calling him racist.

All this time, Manchin had been mumbling about inflation and how he thought it was likely to be worse than Biden or the Fed was saying — and then inflation did turn out to be worse than Biden or the Fed was saying.

My guess is that Joe Manchin thinks he has been acting in perfectly good faith this whole time, while Schumer has been acting in bad faith and the White House has been showing bad judgment about the economic situation. This is not to say that Schumer really has been acting in bad faith. My main view is that bad faith is usually overstated and everyone is the hero of their own story.

Where I fault Manchin — and moderate politicians from both parties more broadly — is that he’s been very passive despite being the pivotal player in American politics. He okays some progressive stuff and gives the thumbs down to others, but he doesn’t really exert his power to try to force the tempo of policymakers and say “here’s what I think a good bill would look like.” But he’s a very influential figure in American politics, we are in a perilous moment, and he ought to work out what he’d like to do and try to steer policy in that direction.

At the same time, what I haven’t seen since Build Back Better ran off the rails is a real effort from the White House and congressional leadership to mend fences — apologize, throw someone under the bus, do Manchin-friendly executive orders, whatever it takes. But time is really running out here. Inflation is very high. Demand growth has to come down. Democratic Party elected officials have a window of opportunity to target rich people for a fair share of that demand restriction. But it’s expiring incredibly soon and calls for some real urgency.

What else could we do?

If Democrats can raise a trillion or more in tax revenue, I personally wouldn’t want to see it all go to deficit reduction, even though deficit reduction is warranted by the current economic situation.

Out of everything in the BBB proposal, the $350 billion or so in tax credits for the production of zero-carbon energy is both substantively important and also well-aligned with contemporary anti-inflationary imperatives. I would really like to see leadership do anything it takes — literally making any concessions around domestic fossil fuel regulation or anything else — to get Manchin to agree to that.

Beyond that pot of money, I’d be happy to spend on plenty of other ideas. But the only question that really matters is what Manchin and Sinema want to spend money on. If they want to build a couple of giant golden calves in their home states, we should do that. If they want to make the ARP enhancements of Affordable Care Act subsidies permanent, we should do that. If they just want to reduce the deficit, then we should do that.

The important thing is to write a bill that is overall anti-inflationary, passes Congress, and is signed into law. That’s important substantively. And I also think that it’s important politically. I’m not sure Democrats quite recognize how close we are to totally losing sight of the traditional class basis of American partisan politics. Voters are very myopic, and if we don’t have a good old-fashioned fight every few years about taxing the rich, then people will just forget that fundamentally low taxes on rich people by any means necessary is a core priority for Republicans. The way to dramatize that is for Democrats to get off their butts, apologize to each other for past mistakes, and do some legislating.

I understand the frustration with Manchin’s refusal to provide his specific priorities within a $1.5T bill. Yet I get the impression he doesn’t have strong preferences for one program versus another. Further I don’t think he wants to get the political flack for picking and choosing which programs make the cut.

And I think that is reasonable. Those hard decisions should ultimately reside with party leadership; chiefly, Schumer, Pelosi, and Biden. That is the job of being in a leadership role; making the hard calls that can build a voting block to pass legislation and receiving political flack for their decisions.

I personally blame these three leaders for eschewing their responsibilities. Yet I can understand their concerns about having to anger some political blocks, journalists, and twitterati “thought leaders” by explicitly endorsing certain priorities over others. E.g., stating they want to drop the CTC in favor of addressing climate change and deficit reducation. No matter what they choose they will anger someone and receive a fair amount of loud condemnation.

It’s even possible that these three leaders don’t see the possibility of reconciling these priorities into a package that can garner sufficient votes among congressional Democrats. Any proposed package may be vetoed by Dems that don’t see their hobby horse included. E.g., the SALT assholes. In which case our Democrat leadership finds themselves in the sisyphean task of going through the motions of developing and championing a cornucopia of Dem priorities while knowing no such bill will ever pass.

Yes! Yes! Yes! This should be a no-brainer. That the Democrats are not doing this, that in fact, despite the Trifecta we’re close to the midterms and they *still* haven’t corrected the horrible (an hugely unpopular) GOP tax cuts, show the party has a radical problem. How could they be so incompetent or clueless??

I have two main suspicions: 1. Weak leadership from the WH leaving a vacuum that makes it very difficult to get things done 2. Structural changes in the voter base mean that the Dems are no longer truly incentivized to pursue a classic left-wing economic agenda, not even a very moderate one.

As evidence for no. 2 I’ll point out that until quite recently the left-wing of the party used to be progressive in the original sense: Warren was all about anti-trust, regulation, taxation. Sanders basically the same just in a more populist and less-wonky style. But since Trump took power the Dems lost their North Star. Warren and even Sanders paying homage to woke agenda that they truly ignored (or that simply didn’t exist) until 2016 or later. Heck, Sanders used to be an immigration skeptic - a proud tradition in a labor left - but in the 2020 came out publicly for decriminalizing illegal border crossing !

And Warren nowadays still does some good work, but it seems her no. 1 issue now is student loan debt. What happened to them? I suppose they (naturally enough) fell inlove with their own new found popularity, and then got carried away by a hyper-educated and pretty wealthy base, that is not truly interested in economic-left policies beyond the occasional virtue-signal. Culture wars are far easier on the old pocket.