It's time to commit to refilling the Strategic Petroleum Reserve

To guard against future price spikes, guarantee that oil prices won't get too low

Back on June 2, Joe Biden tweeted that companies should lower the price of gasoline — a move that attracted widespread derision (including from me) on the theory that presidential tweeting doesn’t really set the price of globally traded commodities.

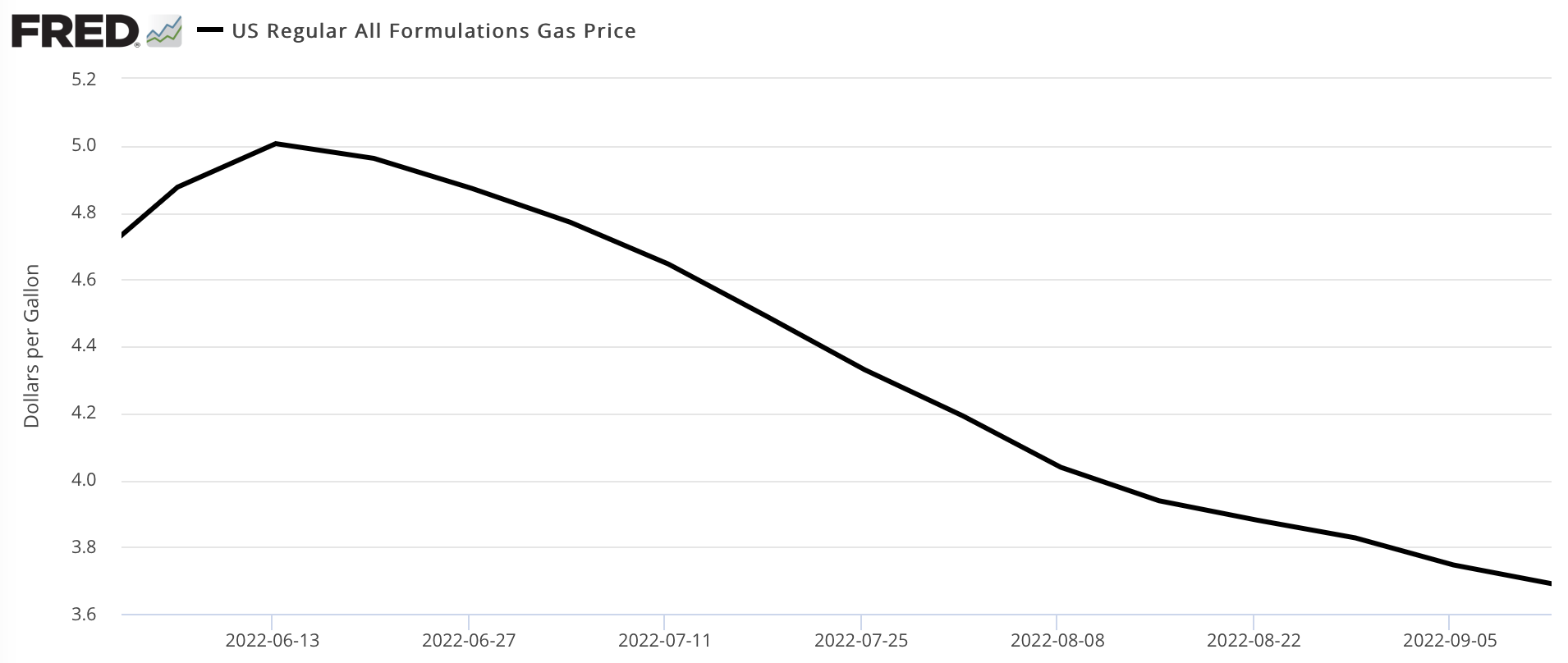

And yet, the facts don’t lie — after Biden’s tweet, the price of gasoline started to fall!

The question of exactly how much Democrats’ political recovery owes to the decline in gas prices (vs. the backlash to repealing Roe or enthusiasm for Biden’s policy actions or whatever else) has become a hotly contested factional issue. And it’s the kind of thing that’s inevitably difficult to prove. But my read is that it’s pretty important, and most of all it’s a topic where all factions should at least be able to agree on the direction of the impact — gas getting cheaper is clearly better than gas getting more expensive.

And while Biden, of course, did not actually tweet his way to a lower global oil price, the Biden administration has contributed to it. After an early unwise flirtation with “supply-side” climate policy, Biden has largely embraced America’s role as a major oil producer. He’s also directly contributed to global oil supply with historically large releases from the United States Strategic Petroleum Reserve (coordinated, to an extent, with similar releases from allies). This is not the only reason prices have moderated, but the releases did contribute.

The SPR has acquired a reputation over the years as a pointless political gimmick, but it is a genuinely useful policy tool now that the world’s relationship with oil has become more complicated. And since the administration seems undecided on what to do with the now nearly empty SPR, I want to say here that the best way to synthesize Biden’s Russia policy objectives with his legacy on full employment and climate change is to commit to refilling the SPR at a relatively high price, like $80/barrel, ideally by using put options to guarantee prices in advance rather than waiting for prices to actually fall.

It would also, in my view, be wise to try to work with Congress and allies to invest money in making the SPR larger. Trying to buy oil low and sell high is of course a strategy available to all kinds of financial actors. But generating enough physical oil storage capacity (as opposed to electronic futures) to actually absorb excess production or provide excess supply is the kind of thing that requires government-scale financing. And we ought to do it because as the global oil industry enters what should be a period of managed decline, this commodity is too important to be left up to the market.

The logic of an early refill

Modern Democrats have an ambivalent relationship with the U.S. oil industry.

On the one hand, they acknowledge that high gasoline prices not only drive inflation but — very critically — drive perceptions of inflation.

But on the other hand, they see the oil industry fundamentally as their political enemy. That's not just because Democrats are committed to climate policy changes that are at odds with oil industry interests. It’s because the climate left’s master narrative about politics requires them to be doing battle with nefarious special interests rather than with the public’s own unwillingness to make short-term economic sacrifices for the sake of the climate. This turns Big Oil into a bogeyman to be slayed.

From a bogeyman viewpoint, refilling the SPR now looks like a bad idea.

Committing to refilling at $80/barrel would be good for the American oil industry because it offers some protection against losses that could be induced by further drops in the price of oil. It would also likely deny Biden the potential political benefit of oil getting even cheaper.

So why do it?

Well, the main reason is that we can’t have much confidence in the global situation. The Russian government is obviously not our friend, and the larger logic of western economic warfare on Russia is that Russia might decide to start curtailing oil exports at any time. The Saudi government continues to be an official friend of the United States of America, but the Saudis have some kind of corrupt relationship with Donald Trump and Jared Kushner and would clearly prefer them back in power. More broadly, the Saudis have proven over this past year that they cannot be relied upon to deliver oil price stability in the face of a geopolitical crisis with Russia — which is literally the entire point of the U.S.-Saudi relationship.

That means we need to do what we can to hedge against the possibility of a future Russia-induced global price spike. And that means refilling the SPR sooner rather than later and at prudent prices. But more broadly, it means supporting the ongoing recovery in U.S. oil production and creating a situation where investors continue to drill here — and accelerating the price of drilling if global prices rise. And to that end, it’s useful to try to prevent oil prices from tumbling too much.

The oil situation, briefly reviewed

The SPR originated in the 1970s when the United States was an importer of oil. The idea was basically to prevent the country from running out of oil in a crisis.

Of course, once it was created, the idea of using SPR releases to curb basic fluctuations in global oil prices was irresistible but gained a reputation as a pointless political gimmick. Oil price surges are bad for the incumbent, so the opposition party always makes political hay and argues that the incumbent should be doing SPR releases. But for 40 years, the global price of oil was fundamentally determined by OPEC’s production decisions (or more recently OPEC + Russia), so the SPR couldn’t really make a difference.

The U.S. shale oil boom changed that.

Shale fields are more expensive to produce on a per barrel basis than the Saudi fields. But they are also a less gargantuan undertaking than offshore drilling, with the individual projects relatively quick to spin up and spin down. That meant that with world oil prices at moderate or high levels, the world’s marginal oil fields were actually in the United States of America.

One way you see this manifesting is that the price of oil in the United States (the West Texas Intermediate price as measured at the big pipeline junction in Oklahoma) is generally a bit lower than the global ocean-borne price. That’s because the U.S. has started exporting enough oil that logistical bottlenecks are a relevant economic factor.

The world of shale oil has also been pretty aggressively competitive, with lots of different companies drilling and producing. That’s meant that, like in any healthy competitive market, the profit margins were historically not that great. Then in 2014, OPEC decided they were worried about the permanent loss of global market share and pricing power and wanted to try to drive American frackers out of business. Gulf oil is still cheaper to produce than shale oil, so OPEC waged a price war and created a situation where American producers were losing money and going bust. The idea, from the Saudi perspective, was to deter future investment in shale oil and keep the Gulf on top. But it’s hard to keep a good wildcatter down, and by 2018 and 2019 the United States was pumping more oil than ever. Then came Covid-19, a huge collapse in global oil demand, and another wave of losses for American frackers.

U.S. environmentalists spent a while taking victory laps on this because a loss for fossil fuel investors was seen as a win for renewables.

It’s bad when nobody drills

But as the global economy recovered, it was clear that the win was illusory. This isn’t to deny that renewables aren’t winning — wind and solar installations are rising quickly thanks to falling costs. Batteries are getting cheaper, which is driving the adoption of electric cars and electric bikes. But change takes time. New England still needs fuel oil for heat. Most people have ICE cars. There are no commercially viable electric airplanes. All of the trends toward renewables and electrification are very real, but also not meaningfully impacted by short-term oil prices.

The actual winner of the fracking bust was non-U.S. oil exporters, most of all Saudi Arabia and Russia. As prices started to rise, American investors did not want to pour money into expanded fracking; they’d been burned twice and didn’t want to lose their shirts again. So everyone who was already pumping oil — Russia, Saudi Arabia, Norway, Gulf of Mexico fields, the frackers whose wells were up and running — enjoyed windfall profits. A lot of people on the left complained about these windfalls without fully acknowledging that windfall profits for incumbents are the necessary corollary of an investment drought. Either the private sector puts money into new production and competes profits away, or else financiers are induced to “keep it in the ground” and margins soar.

And for a while earlier this year, we had major shale barons saying that they wouldn’t pump any more even if oil went to $200/barrel because they were so burned by the past few busts.

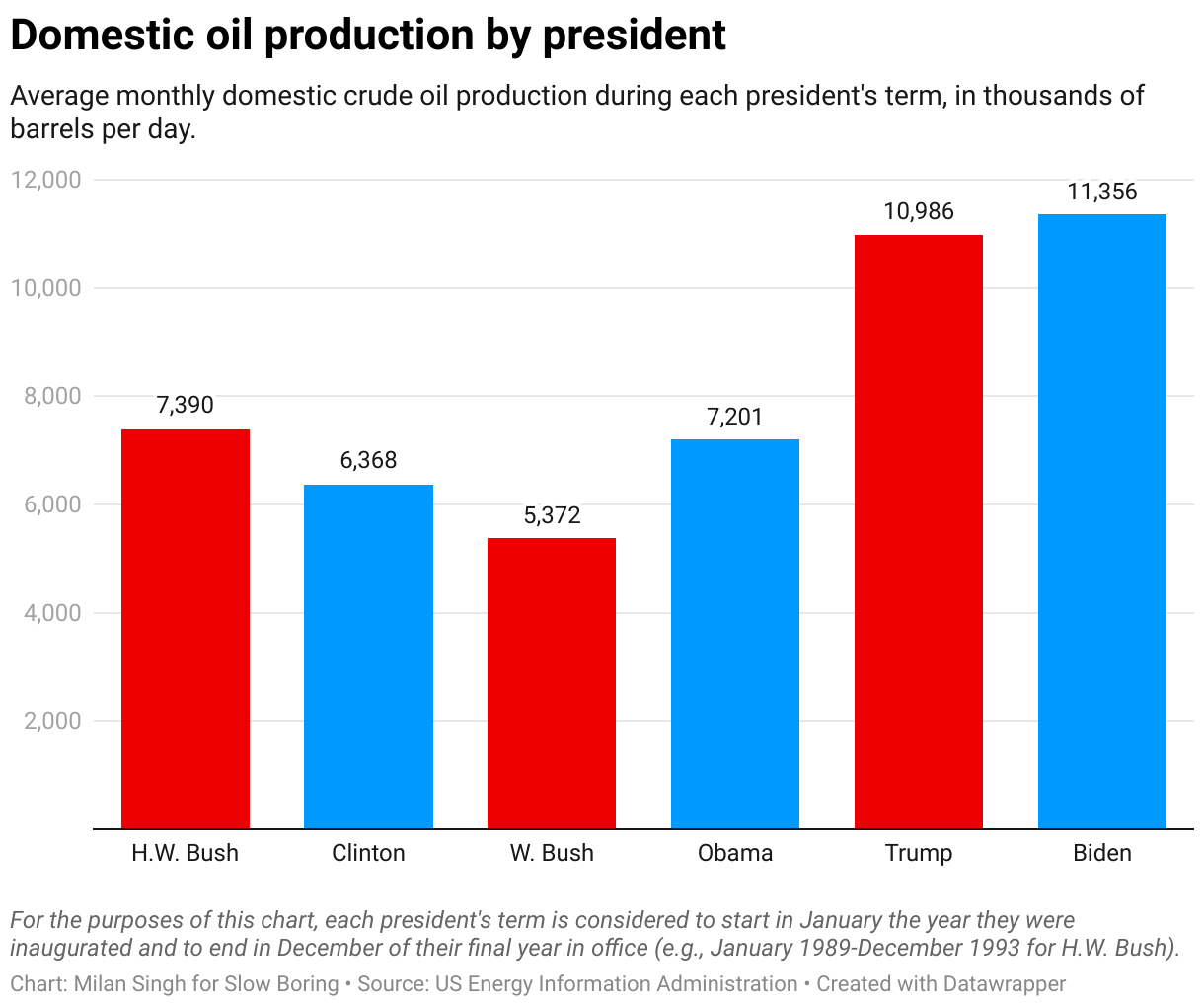

Fortunately, this turned out to be somewhat of a bluff, and production did end up rising quite a bit. Indeed, despite Republican complaints, we are actually pumping more oil under Biden than under any previous administration.

What’s still true is that production hasn’t recovered all the way to 2020 levels, which means the world is still operating in a state of energy scarcity relative to where we were before the pandemic, which makes full economic recovery difficult. But it also means the global economy is significantly at risk of further disruptions in the availability of Russian supply.

The Biden administration has limited tools to deal with this, but refilling the SPR at $80 a barrel helps on two fronts.

Price floor now, price ceiling later

In basic mechanical terms, if we refill the SPR sooner rather than later, that helps hedge against future Russian wrecking by giving us more oil to release. That’s important. If we wait around to get the federal government a better deal at $60/barrel or if we decide SPR refilling is a bailout for big oil that shouldn’t be done at all, we’re left exposed.

But the even bigger deal is we want a situation where if prices rise, the volume of investment accelerates.

If that happens, it limits the impact of Russian actions on global oil prices, which is good for the economy. But it also ensures that a Russian oil cutoff creates an economic windfall for the United States specifically. Russia would lose revenue and oil-importing countries would see a reduction in their terms of trade, but the United States would get a big boost in investment and growth. That’s a decent outcome for us. And because it’s a decent outcome for us, Putin is relatively unlikely to want to do it — deterrence is valuable.

Yet in terms of encouraging that outcome, investors still don’t want to pour money into addressing a price spike if they’re likely to lose their shirts in the next price crash. By refilling the SPR aggressively to minimize the odds of a price crash, you reduce the downside risk of investment and help avert price spikes.

Oil is too important to leave to the market

Over the past couple of years, a number of leftwing publications have hit upon the idea that they should run an article calling for nationalization of the oil industry in order to responsibly manage the transition to electric vehicles:

“Nationalize the U.S. Fossil Fuel Industry to Save the Planet” [American Prospect]

“It's time to nationalize the fossil fuel industries: That'll trigger the right!” [Salon]

“A Moderate Proposal: Nationalize the Fossil Fuel Industry” [The New Republic]

“Nationalizing Fossil Fuel Industry Is a Practical Solution to Rising Inflation” [Truthout]

These are fun takes, but I don’t think any of them really consider practical politics, partisan rotation in office, or the dozens of obvious thorny management issues that would come with creating state-owned oil companies. But I think the impulse behind these takes reflects something important, namely that fossil fuel production is both dangerous (in a climate change sense) and also far too significant to be left to the whims of financial capitalism.

A pure neoliberal take would say that we should price the externality (carbon tax), which will help lock in the trajectory toward lower long-term oil consumption, which in turn will depress investment in oil production, which in turn will further increase prices and price instability, and that will serve to further speed up the energy transition. That would be fine if all major elected officials agreed that it was a good course of action and if the public agreed that sporadic surges in gasoline prices are a small price to pay for long-term climate progress. But we know in the real world that neither of those things are true, and if we create a situation where the inevitable price of the clean energy transition is 20 years of gasoline scarcity and sporadic price spikes, then people are simply going to turn against the clean energy transition.

But while nationalizing the fossil fuel industry would require unimaginably large levels of political change, putting a firmer steering hand on the trajectory of oil prices can be achieved with a relatively light touch.

What we need to do is stop thinking of the SPR as being about physically securing a domestic oil supply (that’s an obsolete notion from when we were a net importer rather than a net exporter) and start thinking of it as a routine price management tool. When oil gets too expensive, we sell. But before oil gets so cheap that it’s unprofitable to drill at home, we buy. That way we, rather than OPEC, steer the global oil price, and we steer it with an eye toward our geopolitical goals and in a manner that is consistent with the goals of the energy transition.

At the moment, Americans are buying electric cars as fast as they can be made. The relevant bottleneck is getting the minerals for batteries, not that gasoline is too cheap. We should try to do this price stabilization with the SPR we have. And we should also try to get Congress to put the money up to make the SPR even larger so as to be more effective. And we should acknowledge that the desired upshot of this is that at some point in the near future, the country winds up paying a decent chunk of change for a final batch of oil that never gets used. The point is to socialize the risk of continuing to pump as long as we need the oil so that we can have a nice, smooth ride toward decarbonization rather than a bumpy one.

This is both a little more economically interventionist and a little less orthodoxly green than a lot of Democrats are comfortable with. But the alternative of continuing with a strong anti-Russian foreign policy and then creating a recession to control inflation makes very little sense and is not going to be tolerated by the public. Taking the strongest possible guiding hand to moderate oil prices is the way to reconcile Biden’s foreign policy goals with his domestic legacy on full employment and energy transition. The White House is considering the right moves here, but it hasn’t pulled the trigger yet. The time to act is now, while the news on both gas prices and Russia is pretty good, so we can get out ahead of problems before they arise.

This is maybe the most disappointing post in Slow Boring history because the Biden Admin has a policy around refilling the SPR and... one would never know that from reading the post.

https://www.whitehouse.gov/briefing-room/statements-releases/2022/07/26/fact-sheet-department-of-energy-releases-new-notice-of-sale-as-gasoline-prices-continue-to-fall/

"The Administration is also moving forward with a proposal to allow fixed-price forward purchases of crude oil to replenish the SPR and encourage short-term production. Relative to conventional purchase contracts that expose producers to volatile crude prices, the fixed-price contracts can give producers the assurance to make investments today, knowing that the price they receive when they sell to the SPR will be locked in place, providing them with some protection against downward movements in the market. This proposal, if finalized as proposed, would encourage near-term production, promote market stability, and put the federal government in a better position to respond to future market volatility.

The Department of Energy is proposing rulemaking this week that would allow for these purchases. The new rule, if finalized as proposed, would enable the Department to enter into purchase contracts for future delivery at a fixed price. Under current regulations, the Department can enter into contracts for future delivery, but the price paid reflects prices at the time that product is delivered. By instead allowing for the price to be fixed at the time the transaction is executed between the parties, this regulatory change would provide greater certainty to producers regarding the revenues they could expect to generate if they produce more crude oil in the short-term, knowing that the Department has contracted to purchase these barrels at a previously agreed-upon price to replenish reserves.

Importantly, the actual delivery of these volumes back to the Reserve will not take place until well into the future, likely after FY 2023. This means that the repurchase agreements will encourage greater near-term investment in supply but will not raise demand for barrels now or in the near-future."

I guess Matt is assuming that his readership is aware of the Biden Admin repurchasing plan and this column is intended as a revision. But I think it is beneficial, when advocating a policy change, to say what the current policy is first.

BTW, as someone who wants to see Democrats win in November, I don't think the Biden Admin should be taking steps to drive oil prices UP before election day.

I agree that the SPR should be refilled and assume it will happen after the midterms but I think the government creating a put wall at $80 is a bad idea and would encourage all sorts of frontrunning and games around that price. I think it would be much better to announce we are planning to refill the reserves over the next x number of months by purchasing roughly x number of barrels per month. I think that would create less shenanigans in the market and achieve the goal of refilling the reserve.