How the government can help increase housing supply

The Biden-Harris administration has increased access to capital, but Federal Home Loan Banks should be doing more.

Today’s column is a guest post from Deputy Secretary of the Treasury Wally Adeyemo.

We need more housing supply in America. It is the most important thing we can do to lower the cost of housing. It is true that accomplishing this goal is going to take more than federal money; it is also going to require state and local governments to put in place reforms that make it easier to build housing. But we should not underestimate the important role federal dollars can play buying down the cost of capital as well as creating incentives for local and state governments to support housing construction. Over the last three years, the President and Vice President have focused on doing everything possible to promote housing construction, and they’ve also called for additional resources from Congress to help lower the cost of housing by increasing supply.

Administration actions and proposals

Few recognize the ways American Rescue Plan (ARP) money is being used to increase housing supply. In order to promote more construction, the Treasury Department offers states and localities the ability to use ARP resources to invest in housing, and communities have now dedicated over $7.5 billion of this funding to build and support tens of thousands of units of affordable housing across the country.

Beyond this additional funding, we’re trying to solve financing puzzles for developers. During a project, developers often first take out a construction loan before the property owner takes out a mortgage. During the time it takes to construct a home, interest rates can fluctuate, creating risks for developers. That’s why Treasury and HUD revamped the Federal Financing Bank Multifamily Risk Sharing Program so that eligible borrowers have access to a “rate collar,” meaning we can provide them with greater certainty about the interest they will have to pay. A housing agency in Montgomery County, Maryland, has already taken advantage of these risk-share loans and will use the new rate collar to finance and build new mixed-income housing.

We also, of course, continue to administer one of the federal government’s largest housing program, the Low-Income Housing Tax Credit (LIHTC), which provided $13.5 billion last year to support affordable housing. In order to meet the need for additional supply, the President and Vice President have asked Congress to invest $37 billion in expanding LIHTC to build or preserve 1.2 million affordable rental units.

They also have requested a new $20 billion Innovation Fund to create competitive grants that incentivize state governments, local governments, and Tribes to expand housing supply by reforming local regulations, building projects near transit, converting properties from commercial to residential, and more. And they have proposed a new $19 billion Neighborhood Homes Tax Credit that would be the first tax provision to directly support building or renovating affordable homes for homeownership, supporting hundreds of thousands of starter homes.

President Biden and Vice President Harris have made clear that the Administration will do everything we can, but we also need others to help. One group that has a responsibility and the capacity to contribute more to housing supply is the Federal Home Loan Banks (FHLBs).

Federal Home Loan Banks

Nearly 100 years ago, Congress created the FHLBs to help meet our nation’s housing needs. Unfortunately, over the years, these banks have focused less on supporting housing and liquidity as more of their resources have gone to paying executives and building up their reserves.

The FHLBs are government-chartered corporations that benefit from both an exemption from paying taxes and the perception of implicit government support that allows them to borrow more cheaply than private actors. Outside experts estimate that the FHLBs receive an annual federal subsidy of more than $7 billion.

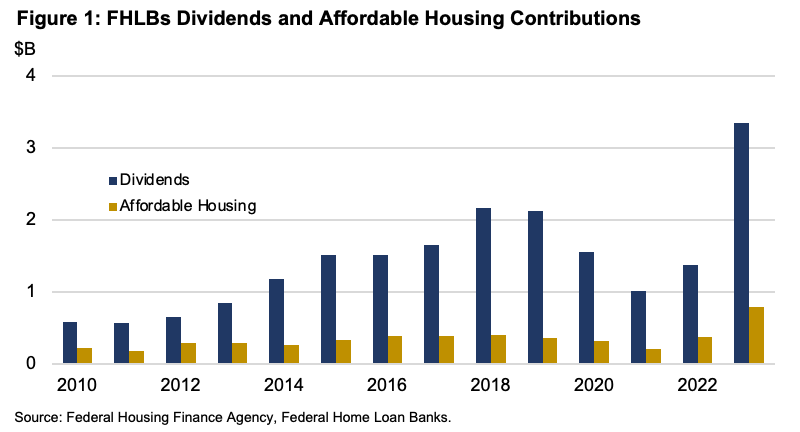

Congress gave these benefits to the FHLBs so that they could more effectively support housing in America. Instead, they have been giving increasingly large dividends to their shareholders, while keeping affordable housing contributions modest (Figure 1). Last year, the FHLBs provided $792 million to affordable housing programs while giving $3.4 billion in dividends to their shareholders.

Just last year, the FHLBs generated record net income. They are also sitting on $20.3 billion in unrestricted retained earnings—up $14.4 billion since 2010—part of which they could use to support affordable housing. The FHLBs’ claim that they need these reserves, which are well above their regulatory capital requirements, is not supported by logic. Their own regulator, the Federal Housing Finance Agency—the actor most concerned with the FHLBs’ financial risk—has no concerns with the FHLBs allocating more of their retained earnings towards housing programs.

With the government benefits FHLBs enjoy, they should be doing more to address the housing affordability crisis. As a starting point, Treasury has spent the past few months trying to constructively work with the FHLBs to voluntarily increase their commitment to housing programs to 20 percent of their earnings. If this level of commitment had been in place, the FHLBs would have contributed nearly $2 billion more to housing programs over the past five years than was required by law. But the FHLBs refused to make this commitment, preferring to retain these assets for their own benefit.

In the meantime, American families continue to face a housing affordability crisis. We know what we need to do to solve this crisis: We need to build more homes in America. It requires all of us to step up and do our part. The Biden-Harris Administration will continue to do our part, and we need the FHLBs to do theirs.

We know a number of the FHLBs would like to do more to support housing, but there are a few members that have prevented these Banks from acting in the public interest. Building more housing is a bipartisan issue, and we need the FHLBs to do their part. If the FHLBs are unwilling to do more to address the nation’s housing needs, we should consider whether federal resources used to support the FHLBs could be put to better use helping reduce the cost of housing for Americans.

"Affordable [housing/homes/rental units]" appears seven times in this piece and sixty times in the linked "Federal Home Loan Banks Combined Financial Report" (which is, it must be said, much longer).

Neither defines "affordable", and it's hard to tell whether the authors are using it colloquially, or in the technical sense of "costs no more than 30 percent of income" - the common definition for government programs.

At any rate, I think everyone who pays serious attention to housing in the US knows two things:

- 'Filtering — the process by which properties age and depreciate in quality and price, becoming more affordable to lower-income households — not new construction, is “the primary mechanism by which the housing market provides affordable supply.”' (https://www.huduser.gov/portal/pdredge/pdr-edge-featd-article-061520.html)

- Affordability provisions often frustrate development, both because they make the projects less attractive for investors and developers, but also because they activate NIMBY resistance. Sometimes, NIMBYs even _add_ those provisions to make projects less palatable and harder to finance.

All of which to say is: the exclusive focus on constructing new "affordable" homes seems well-intentioned, but counter-productive.

Most of the obstacles to housing supply and lower housing prices are at the state level, but there are some tax policies that artificially boost the market price of housing while having almost no effect on supply. The federal government could stop doing these things. It wouldn't have a MASSIVE effect, but it would have an effect:

1. Eliminate the special tax status of REITs. For those unfamiliar, a REIT is a type of company that consists of at least 75% housing and cash and distributes at least 90% of its earnings to shareholders. As long as it does this, it's exempt from corporate taxation. I'm not a fan of the corporate tax, but as long as we have it, it should be applied equally across the board.

2. Eliminate the primary residence deduction. If you sell your primary residence, you can deduct $250k from your capital gains taxes or $500k if filing jointly. Again, if I had my way, we'd be taxing consumption anyways, but while we have capital gains, they should be taxed the same across the board. For political reasons, current owners would probably have to be grandfathered in. That's fine.

3. Eliminate SALT and MID. Again, you'd probably have to phase them out over time, which is fine.

4. Eliminate steel and lumber tariffs. Self-explanatory.