The problem with flexible average inflation targeting

Nobody — including the Fed — is clear on what it means when inflation is high

This piece is written by Milan the Intern, not the usual Matt-post.

You may not have noticed at the time, given everything else going on in the world, but back in August of 2020, something very important happened: Jay Powell gave a speech in which he announced that the Federal Reserve had updated its strategic framework, the central bank’s guidelines for conducting monetary policy. Instead of targeting 2 percent inflation annually, the Fed would target 2 percent inflation on average:

…the Committee seeks to achieve inflation that averages 2 percent over time, and therefore judges that, following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.

This was a BFD and has played a significant role in both the successes and failures of economic policy over the past few years.

Still, the announcement raises some questions. How much inflation does “moderately above 2 percent” entail? How long does “for some time” mean? That’s not because monetary policy is some sort of dark wizardry — it’s genuinely unclear what the new framework means in practice. This in turn is a problem for the economy since the Fed tries to make monetary policy predictable, which can’t really happen given the incredible levels of confusion and disagreement (even inside the Fed itself) over what the current framework actually means.

A brief history of monetary policy

Under the Federal Reserve Act, the central bank’s mandate is to “promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.”

The idea of a balance between price stability and maximum employment is called the Fed’s “dual mandate,” and it’s related to the idea in economics that there is (in the short-run at least) a tradeoff between lower unemployment and higher inflation. This is known as the Phillips curve,1 and the basic idea is that if unemployment is really low, workers will have a lot of bargaining power to demand raises, and firms will raise prices in order to pay for them. The rising cost of living causes workers to demand further raises and firms to further raise prices, which can cause an inflationary spiral if left unchecked. Conversely, low inflation can be caused by high unemployment as bargaining power is diminished. So central banks aim to strike a balance between promoting employment and controlling inflation.

In the 1970s, the United States and many other countries experienced very high inflation. That was checked across the developed world over the course of the 1980s largely via a very severe recession. In order to prevent a recurrence of that cycle, the Reserve Bank of New Zealand began officially targeting 2 percent annual inflation in 1989, with most other countries’ central banks following suit. Under Alan Greenspan, the Fed unofficially targeted 2 percent inflation but did not make the target explicit because Greenspan believed it beneficial for the Fed to reserve the right to “look through” certain things — essentially to have the option to blow off weird stuff.

When Ben Bernanke was Chair, the Fed made the 2 percent annual inflation target explicit, believing that it would enhance trust in their decision-making. The idea was that markets can more easily understand how the Fed would respond to a given situation if a framework is in writing, as opposed to hoping investors can read the chair’s mind.

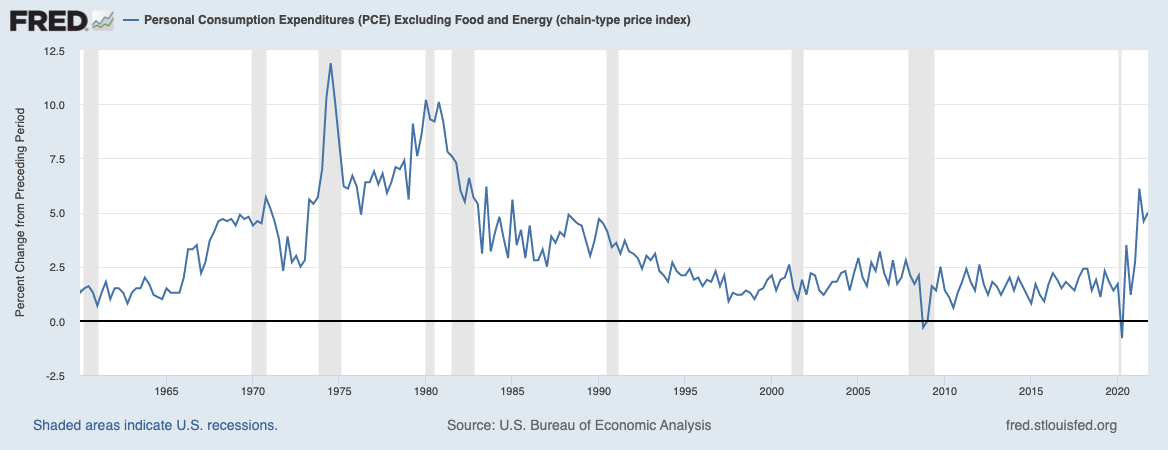

But Timothy Lee of Full Stack Economics told me that under Bernanke (and later Janet Yellen), the Fed treated 2 percent as a ceiling rather than a target, “tapping the brakes” by raising rates when they believed inflation was getting close to 2 percent rather than when it went above 2 percent. So in practice, the Fed was targeting somewhere between 1.5 and 1.8 percent inflation. Indeed, after “the Great Inflation” of the 1970s, inflation rates steadily declined during “the Great Moderation,” and by the 2010s the Fed was consistently undershooting the 2 percent target.

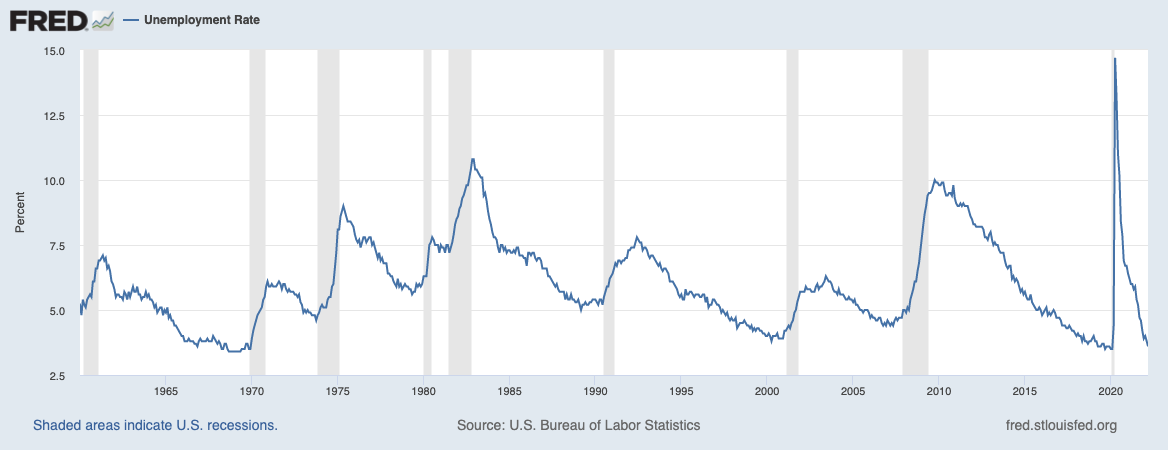

That might seem great — after all, who doesn’t want lower prices? — but the flip side is the Fed was neglecting the maximum employment half of the dual mandate (recall that there is a tradeoff between the two). If you look at the data you’ll see that there was a prolonged period of elevated unemployment in the low-inflation aftermath of the Great Recession.

And that’s what the Fed’s new average inflation targeting framework was designed to correct.

Flexible average inflation targeting, explained

The new strategic framework announced in 2020 was in many ways a response to the shortcomings of past Fed policy and the sense that they had underrated the benefits of full employment. The key change is that the Fed will now target 2 percent inflation on average rather than 2 percent every year with the aim of making up for past undershooting.

To be clear, the idea is not to seek higher inflation for its own sake, but to make up for past shortfalls in employment by increasing demand, with the side effect of mildly higher inflation. Claudia Sahm, a former Fed economist who now works at the Jain Family Institute, told me over the phone that under flexible average inflation targeting (FAIT for short), the Fed is giving maximum employment and price stability equal weight for the first time. But you don’t need to take her word for it, here’s Jay Powell announcing the new framework:

With regard to the employment side of our mandate, our revised statement emphasizes that maximum employment is a broad-based and inclusive goal. This change reflects our appreciation for the benefits of a strong labor market, particularly for many in low- and moderate-income communities.

In researching this piece I spoke to several economists and economics journalists, and all of them said that FAIT was an improvement over the previous Bernanke-era policy because of its increased focus on employment. But the key weakness of FAIT is that it was designed with a low-inflation world in mind, and that’s not how things panned out.

The Fed underrated high inflation

Prior to the pandemic, many well-informed people believed that high inflation was a thing of the past — many of us have spent our entire lives in a low-inflation economy. The “secular stagnation” hypothesis holds that advanced economies will face problems of weak demand and consequently low interest rates and weak growth as a result of demographics and other factors. Here’s Powell in 2018:

While inflation has recently moved up near 2 percent, we have seen no clear sign of an acceleration above 2 percent, and there does not seem to be an elevated risk of overheating.

That line of thinking informed the development and adoption of FAIT. The Fed was very focused on making up for past shortfalls of employment (and by extension, past undershoots on inflation), but if you parse Powell’s 2020 speech announcing the new framework carefully, you’ll notice that he doesn’t actually say what the Fed will do if inflation comes in consistently above target:

…our new statement indicates that we will seek to achieve inflation that averages 2 percent over time. Therefore, following periods when inflation has been running below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.

I think the Fed had good reason to believe that high inflation was unlikely, but ignoring the possibility entirely was a mistake because it’s not clear what FAIT’s prescription for high inflation actually is.

Nobody knows whether FAIT is symmetrical or not

So what happens if the Fed overshoots on inflation? On its face, FAIT might mean they now need to undershoot on future inflation to compensate for the high inflation this year — a symmetrical target.

But Joseph Gagnon of the Peterson Institute for International Economics told me that this is wrong, pointing to a November 2020 speech by then-Fed Vice Chair Richard Clarida. The argument for asymmetry is that if inflation is too high, the Fed can always raise interest rates, but if inflation is too low they can only cut rates down to zero before they run out of firepower, leaving them with far fewer tools to respond to a recession. So the Fed would rather err to the side of a slight overshoot in order to keep their powder dry.

The problem is that nobody knows for sure which interpretation the Fed is using.

Sahm told me that different members of the 12-member Federal Open Market Committee (FOMC) that sets interest rates have differing opinions on this issue. David Beckworth, a monetary economist at George Mason University’s Mercatus Center, said that everyone at the Fed probably agreed that it was asymmetrical but failed to make that clear to the public. Willem Buiter reported for the Financial Times that the various regional Fed presidents (who serve on the FOMC on a rotating basis) have different views on the subject, while Edward Price wrote (also in the Financial Times) reported that FAIT “gives [the Fed] more headroom to target higher inflation,” implying asymmetry.

Now, most people don’t pay attention to monetary policy, and if you asked a random person off the street what they thought about FAIT they probably wouldn’t know what you were talking about. But there’s a difference between a policy that is obscure and one that is unclear. Setting expectations is very important for conducting effective monetary policy, and if the financial press, think-tankers, economic journalists, and even members of the Open Market Committee can’t agree on what the Fed’s policy guidelines mean, then they’re unclear.

What the Fed needs to do next

Frankly, the Fed kind of dropped the ball on inflation. They were too slow to react last year and should have started moving to tighter money sooner. But what’s past is past, and now the Fed has to thread the needle and bring inflation back down without triggering a recession. Fortunately, Powell has acknowledged his oversight and the Fed raised rates by half a percentage point last week, with six more rate hikes expected in 2022.

To be clear, a soft landing is neither out of the question nor guaranteed. Robert Armstrong and Ethan Wu at the Financial Times report that the consensus on Wall Street is real growth above 2 percent, core inflation continuing to slow, unemployment around 3.5 percent, interest rates rising by 2 percentage points over the next year, and a one-in-four chance of a recession (Goldman Sachs has the odds a bit higher, at 35 percent). But they also caution that investors may be over-optimistic here, writing that “the crucial point about a soft landing is that the path is narrow, not that it is unwalkable.” We’ll have to wait and see how things play out.

The Fed’s next strategic review is not scheduled until 2025. The official Slow Boring position is that the ideal monetary policy framework is NGDP targeting. But they’re highly unlikely to abandon FAIT so soon after having adopted it. Beckworth also thinks that before the Fed would consider it, proponents need to build more of an academic consensus around NGDP targeting.

But what the Fed can and absolutely should do is clarify the meaning of FAIT.

FAIT was not designed for a world dealing with a bout of inflation associated with a global pandemic and a massive fiscal policy response. The presumption was that due to demographic trends, most of the world would be facing a Japan-like future of low inflation and weak growth. Those factors haven’t evaporated, and the kinds of situations for which FAIT’s dovish implications were designed are likely to occur in the near future. One major risk today is that the current bout of inflation will discredit the good parts of FAIT right before they are needed.

Some economists have argued that the Phillips curve has “flattened” (or even died) in recent decades as the relationship between low unemployment rates and higher inflation has gotten weaker — see this Substack post from Joseph Politano or this article from The Economist.

Very well done post, Milan.

Being able to explain complicated things in a clear way indicates a thorough grasp of the subject (and makes the reading pleasurable besides). Thanks!