Democrats need to think bigger on utilities

We need more power, not just short-term rate cuts.

Regulation of electrical utilities is quite possibly the single most tedious, technical, boring area of American public policy.

And yet, the price that households pay for electricity is a salient issue, especially when it’s rising, and electricity prices for commercial and industrial uses are substantively quite important for the economy’s long-term prospects. So with electricity bills spiking recently, everyone’s got a take on the issue.

And I’m concerned that many of these takes are much too narrow in focus and sort of mis-state the problem — which is that we need to treat electricity generation as a platform for broader growth and not just an item in the household consumption budget.

First, let’s zoom out. Utilities in the United States come in three basic formats. One is publicly owned utilities (the Tennessee Valley Authority is by far the most important, but there are lots of smaller ones). The other two are investor-owned: vertically integrated utilities (now mostly in the Southeast, but used to be more common) in which the same regulated monopoly that runs distribution also owns power plants; and restructured utilities (nowadays most of the large markets like California, Texas, and the whole Northeast) in which a regulated monopoly runs distribution but there is a competitive deregulated market for generating electricity.

“Regulated” in this context means not only that there are rules about how the company can operate (all industries are regulated in this sense), but that prices are regulated.

The actual price-setting is somewhat discretionary and rule-based, but the basic idea is that the investors are entitled to cover their operating costs and earn some rate of return on their capital investments.

And this is what most of the (too narrow, in my opinion) discussion is about right now: how to push that rate of return down.

The good news is that unlike the proposals I’ve derided as slopulism, reducing the rate of return really will reduce consumer electricity prices. It does what it says on the tin. But lowering the rate of return also reduces capital investment in the electricity sector, and we should be asking whether that’s an outcome we actually want. Are we satisfied with this trajectory?

I don’t think we should be, which means we need to think differently — and bigger — about the whole structure of this industry.

We want more electricity

This whole obsession with reducing utility R.O.I. is really downstream of the degrowth strain of environmentalism associated with Amory Lovins.

Most Democrats would tell you that they’ve left this way of thinking behind, that they have a vision of the world in which we electrify home heat, get people using electric cars (and eventually trucks), and welcome a renaissance of American manufacturing. Setting data centers and A.I. entirely to the side for a moment, that’s a vision that inherently involves producing and consuming a lot more electricity.

With that in mind, I think it’s instructive to look back at this April 2008 discussion paper from the Justice Department’s antitrust division that considered what had worked well and what had not in breaking up the vertically integrated utilities.

The overall judgement of the paper is that restructuring was a success, mainly because it led to operational efficiencies at power plants.

Utility regulation is driven by the belief that the industry is inherently monopolistic. But it’s really the distribution and transmission layer that’s monopolistic; different generators of electricity can compete for the utility’s business. And by forcing them to compete, you create normal market incentives to generate power as cheaply as possible — incentives that don’t exist or are much weaker when the utility is vertically integrated.

The D.O.J. paper then considers two shortfalls of the restructuring model: First, that it’s not clear how to finance inter-regional transmission. Second, that there’s no clear answer to the question of “who determines the when, what, where, and how much of generation investments.”

His ultimate conclusion is that the operational efficiency benefits are the most important thing, so restructuring was on balance a good idea.

This makes sense in the context of 2008, when the country had seen very little overall growth in electricity use (“load” in the industry jargon) and very little further load growth was predicted. And I think we should understand the current discourse about R.O.I. tweaks as being in the same spirit: If you have a basically fixed set of electricity needs, the most important thing is to meet those needs as efficiently as possible.

But if you want to electrify tons of stuff while you also increase manufacturing output, then you’re going to need a lot more electricity. If you need a lot more electricity, then planning for new generation investments and new transmission is really important. And across most of the country the regulatory paradigm isn’t set up to do that.

Planning to plan

The exception that proves the rule here is Texas, which has handled a lot of load growth. Texas is in many ways blessed for this. The state has abundant wind resources and abundant solar resources and also lots of cheap privately owned land that can be purchased for renewables development. It also has a political culture that doesn’t care about climate change and is generally happy to allow the balance of gas and renewables in new generation to be determined exclusively by market forces.

But then on top of all that, compared to other restructured states, Texas has an unusually strong central-planning role in transmission.

Most other places have a tighter set of tradeoffs — between decarbonization, consumption of open land, cost, etc. — to negotiate but no mechanism to plan them.

Northeastern states with progressive elected officials, expensive land, limited sunshine, and poor onshore-wind potential face hard choices. When you ask officials what is the plan, exactly, to generate enough electricity to switch to a winter-peaking grid that can keep homes warm with heat pumps, they don’t have an answer.

Worse than that, they don’t have any institutional mechanism by which an answer could be developed.

People worry, reasonably, that data centers could push up their electricity costs. But anything that uses electricity — a factory, an electric car, a heat pump — poses that exact same risk. Places don’t normally achieve economic growth by preventing people from doing economically useful things with electricity and thereby making electricity cheap. You want a virtuous cycle where investments in generation and transmission fuel economic growth and the growth recoups the costs of the investments.

I’m not getting too deep into the regulatory specifics in this column (though may in a future piece), but I wanted to at least gesture in the direction of thinking more clearly about this.

It is reasonable to not want ratepayers to bear the costs of additional utility infrastructure — higher household electricity costs are one of the most regressive financing mechanisms on Earth.

To address that by trying to stymie investment in additional infrastructure loses sight of the goals, though. What we need are regulatory tools, perhaps including a return to vertical integration in more locations, that allow for coherent planning and both force and enable regulators to address the real tradeoffs.

And we need new financing mechanisms — like taxes, potentially on new commercial users such as data centers — to ensure that the infrastructure buildout doesn’t burden household users in a way that defeats the goal of promoting electrification. That might call for a revival of direct public ownership of utilities along the lines of the Tennessee Valley Authority model.

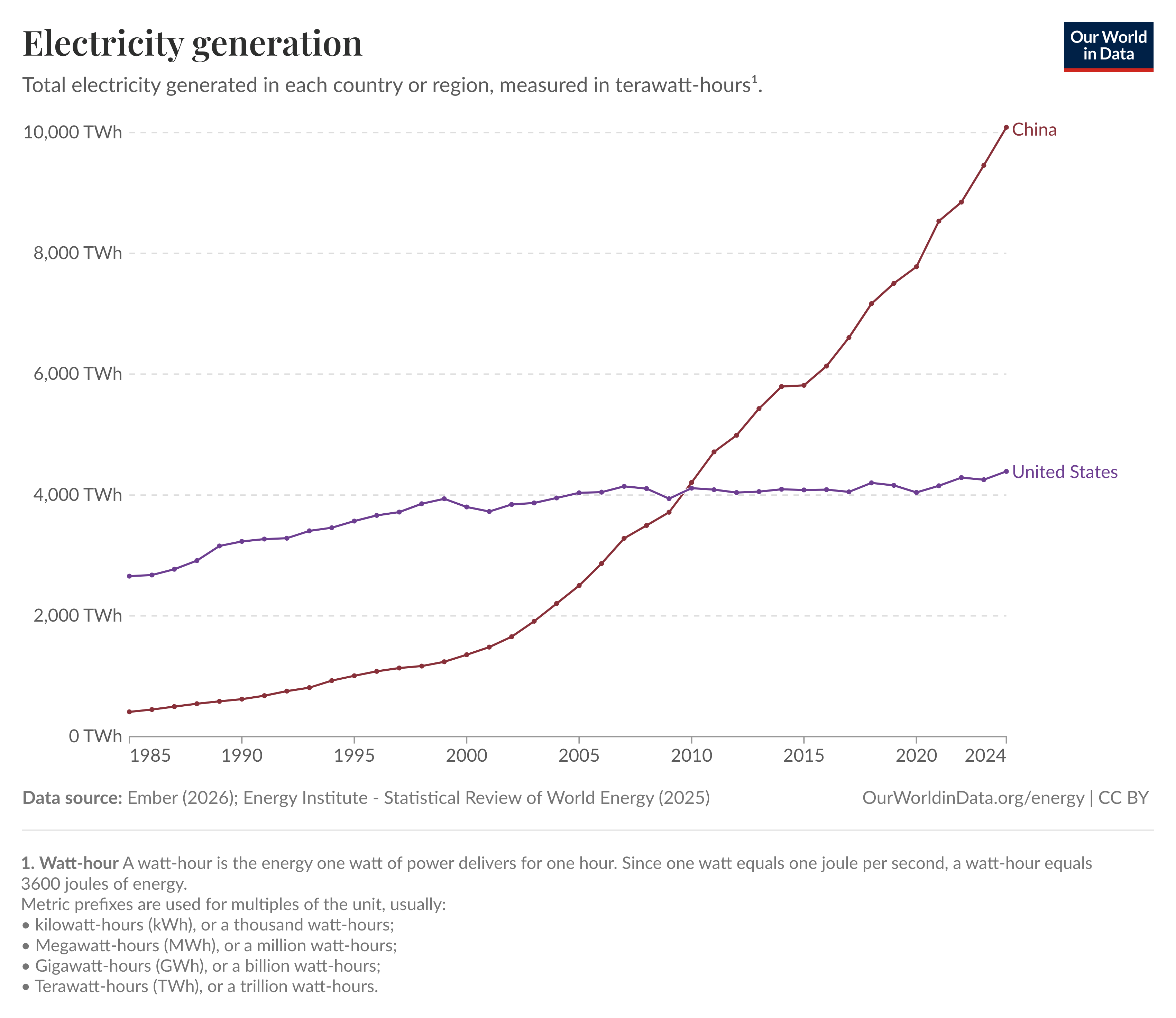

I don’t have a fully fleshed-out theory of what this should look like. But again, just look at that chart of Chinese versus American electricity generation. Shrinking the utility share of the electricity pie isn’t aligning our policy with our goals. We need to start from the premise that we want generation and more transmission, and adopt regulatory structures that support growth rather than maximizing short-term operational efficiency.

As an investor in industrial scale RenEng, Grid. Grid. Grid. My obsession during the Biden Admin where they were not taking this seriously - time to build out this infra is not like playing in IT.

Transmission (long distance), Distribution (local)

Interconnections (regional interconnects) expanded and reinforced to enable at-scale power exchange and RenEng timing arbitrages to reduce issues of wasted production and equally

Capacity on existing lines (lower cost up-front capital upgrade w new tech) increased to reduce congestions.

Expanded lines

Without grid expansion like crazy, RenEnergy is going nowhere, prices are going to skyrocket overall no water generation sourcing.

It would be highly appropriate to have a national funding backing this rather than putting on the backs of local and regional ratepayers

Analagous to the 1950s-1960s highway expansion.

Except it's energy super-highways.

Loved the wonkiness of this and glad Matt is digging into this. Utility regulation doesn't get much attention aside from occasional superficial "the rates are too dam high" takes.

My opinion on the competitive generation vs centrally planned generation debate is that the electricity sector more dynamic and less predictable than it's been in decades. When times are uncertain and rates of innovation and risk are at their highest, market competition generally does much much better than central planning.

IMO, looking at a paper analyzing electricity restructuring in 2008 misses the biggest stress test of restructured markets we've had so far. When fracked gas dramatically lowered the cost of gas generation vs coal, restructured markets proved themselves much better at reacting to the shift and at saving ratepayers money quickly. Uneconomic coal plants were retired much faster in restructured markets because investors knew their plants were sunk costs that couldn't and wouldn't be able to compete. They ate the losses and moved on. In monopoly markets, regulators didn't want to admit to the huge losses that would show up on ratepayer bills as stranded costs. So they kept the uneconomic plants running for much longer at ratepayers' ultimate expense.

The example above shows the real benefit of competitive generation. The main distinction between the two models is who holds onto risk. In the competitive generation model, investors hold risk and if things don't go as expected (eg a plant becomes uneconomic), they take the hit rather than ratepayers. In the monopoly model, ratepayers hold all the risk and have to guarantee payments to utilities even if a plant turns out to not be economic down the road.

The thing is, we're in a period of rapid load growth from data centers and electrification. On top of that, innovation on the generation side is going like gangbusters. Ten years out, we just don't know what load will be or what the most economic generation mix will be. This dynamic environment is where competitive markets outshine central planning by a huge margin.

IMO, anyone that thinks monopoly regulation of power generation is going to serve ratepayers better over the next 10 years is badly mistaken.