America needs more giant banks

The moral of Silicon Valley Bank's collapse is that the real danger comes from the medium-sized ones

The latest Bad Takes episode, also about Silicon Valley Bank.

In 2010, Congress responded to the global financial crisis by passing the Dodd-Frank overhaul of America’s financial regulatory system.

The primary goals of Dodd-Frank were to make bank failures less likely and to create a process for dealing with the failures of large financial institutions rather than having government officials make it up on the fly. Because bank regulation is a sprawling topic, things like the creation of the Consumer Financial Protection Bureau and various securities regulations also found their way into the legislation. But the bill passed because of a desire to avoid situations in which government officials were improvising their response to bank failures, ideally by avoiding failure in the first place.

And yet here we are in 2023, reading press releases about the FDIC invoking special authority to insure uninsured deposits and the Fed creating new special lending facilities for banks.

I don’t think there’s any big problem with these decisions, but they raise the question of how we came to this point after a major legislative debate about how to avoid exactly this scenario. And the answer turns out to be pretty straightforward: in 2018, the GOP-controlled House of Representatives wrote and passed a bill substantially curtailing the regulation of banks that are roughly the size of Silicon Valley Bank on the theory that banks of this size are not systemically important and could be resolved through the ordinary FDIC process. Moderate Senate Democrats who felt the need to burnish bipartisan cred chose this bill as their big bipartisan gesture, calculating that of all the possible issues they could defect on, this was the one that progressive groups were least invested in.1

Trump administration appointees at the Federal Reserve, the FDIC, and elsewhere implemented this legislation very much in the spirit in which it was written, assuming that SVB-sized banks could be resolved through the ordinary process without causing broader economic harm and therefore didn’t need to be tightly regulated. Objections were raised by Democrats on these boards, including Lael Brainard, who now runs the National Economic Council, and Martin Gruenberg, who now runs the FDIC, but they were overruled. Michael Barr, who is now the Fed’s top bank regulator, also objected from outside of government.

Five years later, it turns out that Brainard, Gruenberg, and Barr were right all along — putting SVB through the normal regulatory process would risk the stability of a number of perfectly solvent banks, and therefore the government needs to step in and improvise.

These improvisational bailouts make a lot of people angry, and I share that anger. I’m particularly angry not because SVB or its depositors got “bailed out,” but because the executives and shareholders of other SVB-sized banks also got bailed out as a result of this, even though those executives were the ones who lobbied against Dodd-Frank on the theory that the regulation was unnecessary. And I’m secondarily angry that a lot of other angry people are going to take out their anger on government officials (like Barr, Gruenberg, and Brainard) who warned against this course of action, while the people who set it on us escape blame entirely.

Sadly, “being mad” is not a policy option. But as long as I’m mad, it seems like a good time to uncork a take I’ve been brewing for the last decade: banks operating on the scale of Silicon Valley Bank — the so-called large regional banks — are bad, and the policy of the United States government should be to encourage regional banks to merge and become megabanks comparable in scale to the Big Four. Megabanks are better-regulated and less risky than large regional banks, and creating more of them would lead to a more competitive megabank marketplace and eliminate some of the problems of concentration.

Bank failure without bailout

Something I see over and over again in the discourse is that Americans’ somewhat romantic notions about small businesses allow certain myths about small banks to persist.

A lot of people have it in their heads that small bank failures are inherently safer than large bank failures, and that’s why small banks are entitled to lighter regulatory supervision. Alternatively, people believe that small banks get rougher treatment from the government when they get into trouble — no bailouts! — while larger banks receive special privileges. This is because most people don’t really understand what happens when a small bank fails.

But here’s how it works. When Almena State Bank of Almena, Kansas failed in October 2020, the FDIC closed it and sold it to a bank named Equity Bank based in the Kansas City area. In this situation, the purchasing bank typically pays $0 for the failed bank and in exchange receives the failed bank’s branches, whatever investment assets are left on its book, and the failed bank’s clients and client relationships. The purchasing bank is also now obliged to give depositors their money if they ask for it. This means insured deposits are taken care of without the FDIC spending its money and uninsured deposits are also taken care of without the FDIC spending its money —a good deal for everyone involved. But it relies on the idea that when a small bank fails, another bank will want to take over its branch network.

This is basically a numbers game. There are a lot of banks in the United States, and since “buying” a failed bank is essentially free, the bet is just that some bank or other will have an executive team that’s ambitious enough to want to expand.

The main issue the FDIC deals with in practice is that it tries to avoid excessive geographic concentration. So if a bank with seven branches fails, the preference is to sell it to a bank that doesn’t currently have branches in those communities to preserve local competition. But sometimes that isn’t possible, and the bank that’s most interested in buying has an anti-competitive motive.

In practice, though, this process basically always works out. The FDIC shuts down a bank, it calls up some larger banks that operate nearby (but not in exactly the same locations), and the bank reopens. As I’ve mentioned before, when I first lived in D.C., my bank account was with a longtime local bank called Riggs Bank. Then Riggs was caught doing serious financial crimes, causing it to become insolvent. On Friday the bank was closed, and then on Monday its branches reopened as PNC Bank branches. No depositors lost any money, and the government didn’t need to spend a dime. In effect, rich people who had uninsured deposits got a “bailout” from PNC, as did the FDIC, which would otherwise have been on the hook for the insured deposits. But PNC got to expand into the D.C. metro area. Everyone wins.

In theory, a bank could fail with nobody willing to take it over. In that scenario, the FDIC has to cover the insured accounts, and there’s also a question of what happens with the uninsured accounts. Even if the bank were really small, wiping out uninsured deposits could be a problem because it might cause people to pull deposits from other small banks, wiping them out. But generally when a small bank fails, someone buys it and there’s no problem.

The problem of the middleweight bank

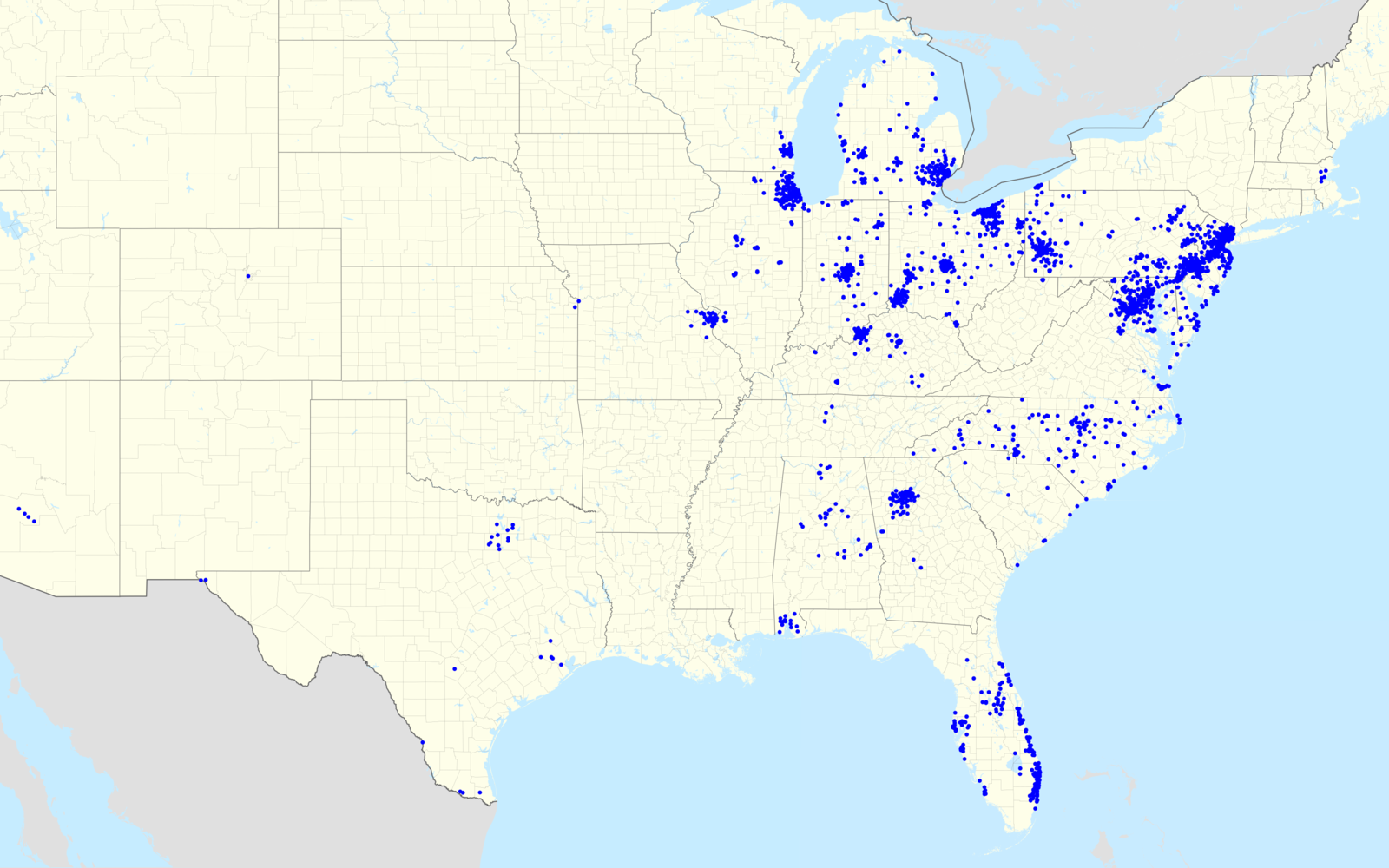

The problem is, what happens if PNC fails? PNC is the sixth largest bank in the country with over $500 billion in assets. That makes it dramatically smaller than the Big Four banks that are informally labeled “too big to fail” and formally classified as Global Systemically Important Banks (GSIBs).

But PNC is still big enough that almost none of the thousands of banks in America could buy it in the event of a failure. And even if Chase or Bank of America could swallow PNC, it’s not clear that they would want to. PNC has an expansive branch network, so expansive that it’s largely duplicative of the network of any possible purchaser.

When you map out the business logic of taking over PNC, splitting up the bank makes the most sense. PNC’s branch network in the South would be complementary to Citibank, its branches in the Midwest would be complementary to Wells Fargo, and U.S. Bank could take over its operations in the Northeast.

But dividing up a bank like that would be a complicated process requiring multi-faceted negotiations among a lot of stakeholders.

Keep reading with a 7-day free trial

Subscribe to Slow Boring to keep reading this post and get 7 days of free access to the full post archives.